Stock markets around the world remain in retreat mode with concern over the Torynutters economic “plan” in the UK sending Pound Sterling to a record low and spiking bond market yields. The USD continues to strengthen against everything with Euro continuing its sharp drop below parity, with the Australian dollar still on the ropes, as commodity prices remain under pressure. Bond markets saw a big lift in yields, with 10 year Treasuries pushing up to the 3.9% level with interest rate expectations still looking at another 150bps in rises by January. Commodities continued to drop below key support levels with WTI and Brent crude falling more than 2%, the latter down to the $82USD per barrel level while gold dropped another $20 or more, failing to support its recent lows and made a new monthly low at the $1620USD per ounce level.

Looking at share markets in Asia from yesterday’s session where mainland Chinese share markets headed lower as we start a new trading week with the Shanghai Composite down 1.2% to 3051 points while the Hang Seng Index is still getting crushed, down 0.7% at 17810 points. The daily futures chart is still showing a very bearish mood and a distinct lack of buying support quite evident. The bear market continues with daily momentum nowhere near out of its negative funk, but at least not getting extremely oversold:

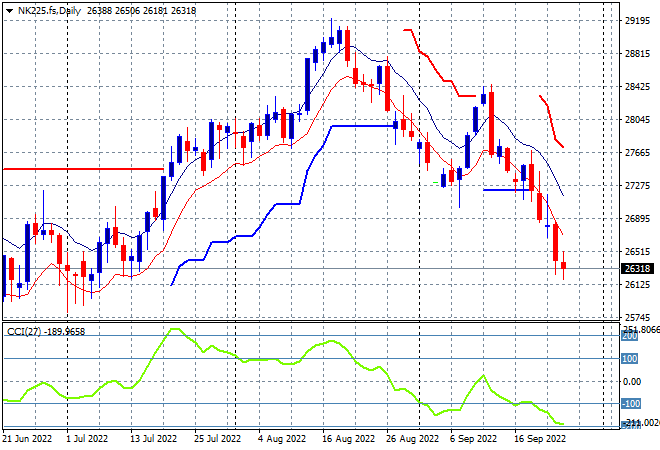

Japanese stock markets were the biggest losers with the Nikkei 225 closing some 2.6% lower at 26431 points. The daily chart shows price action returning to the dominant downtrend after the recent dead cat bounce up to the 28000 point level with support at the 27000 point level taken out recently. Daily momentum remains negative and oversold with successive new daily low sessions pointing to a test of the June lows next as futures are indicating more selling ahead:

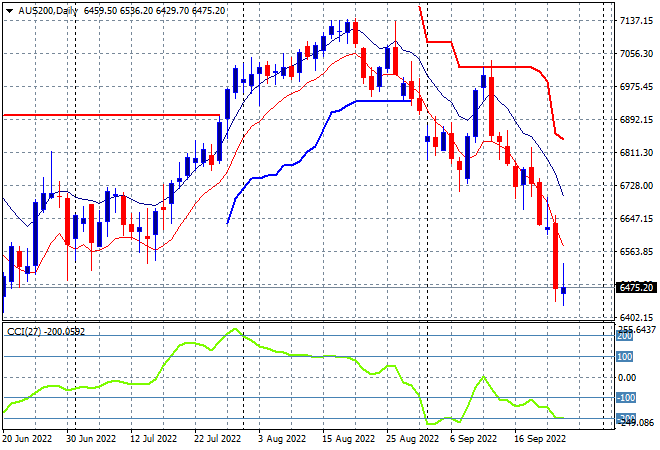

Australian stocks were no longer the worst in the region but its all relative, with the ASX200 losing nearly 1.6% to close at 6469 points, making a new monthly low. SPI futures are up slightly reflecting some stability on European stocks although the late falls on Wall Street could push a further drop on the open. The daily chart shows price action coming up quickly to test the June lows next as daily momentum remains in full oversold mode, with buying support evaporating:

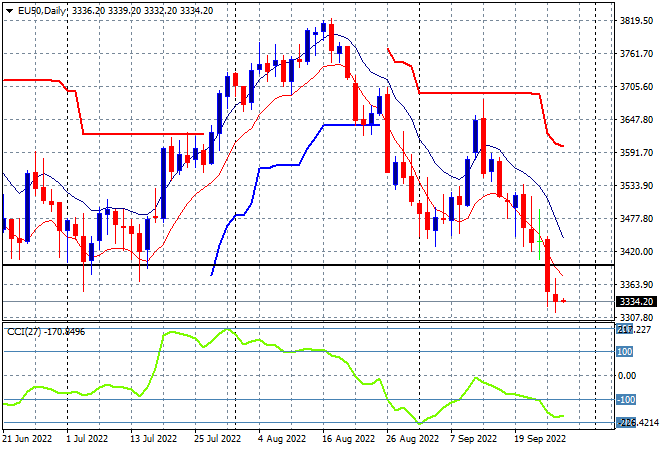

European stocks are still piling on losses but seem to be decelerating, not helped by a much lower Pound Sterling and Euro however. The Eurostoxx 50 Index eventually lost 0.2% to finish at 3342 points. The daily chart shows price action now below the June lows at the 3300 level with another leg down possible as daily momentum remains well oversold:

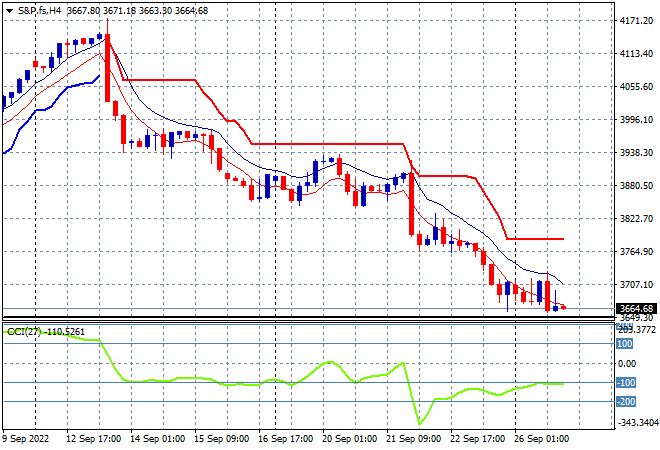

Wall Street however had slightly larger falls, with the NASDAQ down 0.6% while the S&P500 finished another 1% lower at 3655 points. The four hourly chart remains on a steady downtrend similar to all other major stock markets showing how in line market expectations are with the hawkishness of the US Fed. Price has now returned to the June lows (lower black line) which wipes out all of 2021’s returns, but momentum is indicating some deceleration here so watch for support to possibly hold:

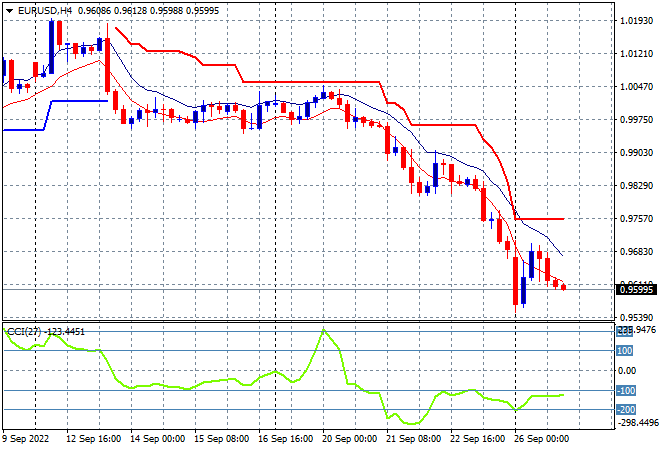

Currency markets remain firmly on the side of the USD, with the big collapse in Pound Sterling – now approaching parity with USD – still not overshadowing Euro’s further drops below parity and breaking through the 96 handle. As expected the union currency continues to be broken by the Fed which is hell bent on containing inflation and is much more hawkish than the ECB, with recession fears mounting. Momentum remains nearly extremely oversold with the four hourly chart indicating more selling pressure as the high moving average is not under threat:

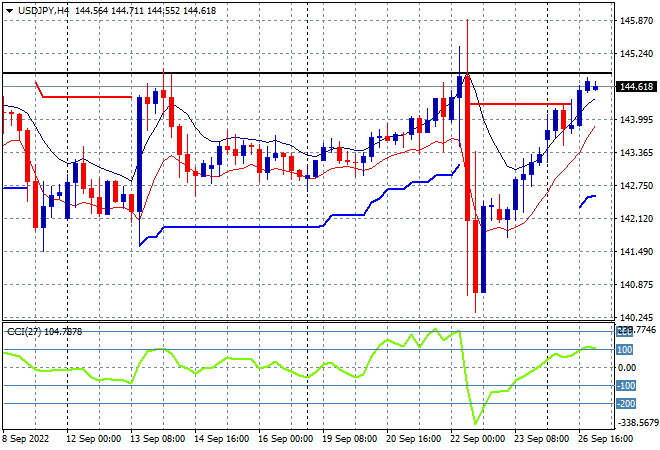

The USDJPY pair continued to melt up after some massive volatility last week around the Fed meeting, now settling at the mid 144 level which equates to the recent weekly highs (upper black horizontal line). Short term momentum has now moved into somewhat overbought following that big volatile move, with price action coming up against obvious resistance at just below the 145 level where its likely to be rebuffed as before:

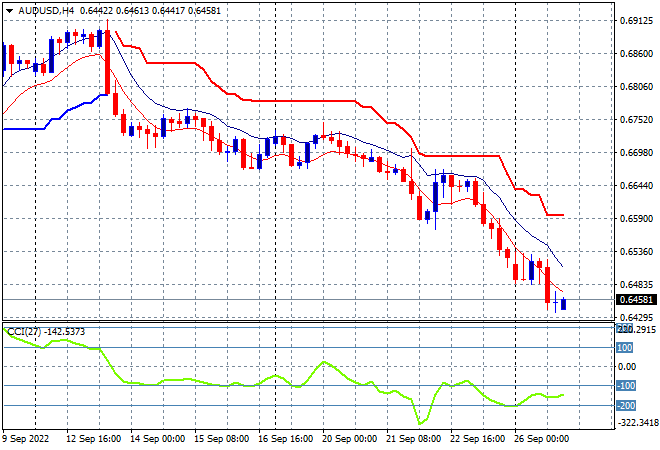

The Australian dollar continued to crack lower, finishing the first day of the new trading week just below the 65 handle, moving in line with risk markets and the falls in commodity prices. My contention that resistance is just too strong at all the previous levels with the 68 handle the area to beat in the short term is holding, with the 67 level firming as well as trailing overheard ATR resistance is just not under any threat:

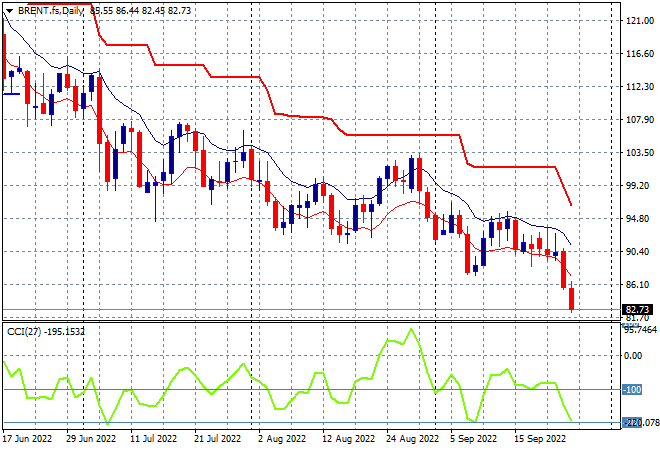

Oil markets continue to pull back following the collapse on Friday night, with Brent crude down another 3% to the $82USD per barrel level overnight. Daily momentum had been persistently negative although not technically oversold but is moving swiftly in that direction as price action is no longer anchored at the recent weekly lows with new monthly lows being made in this rout:

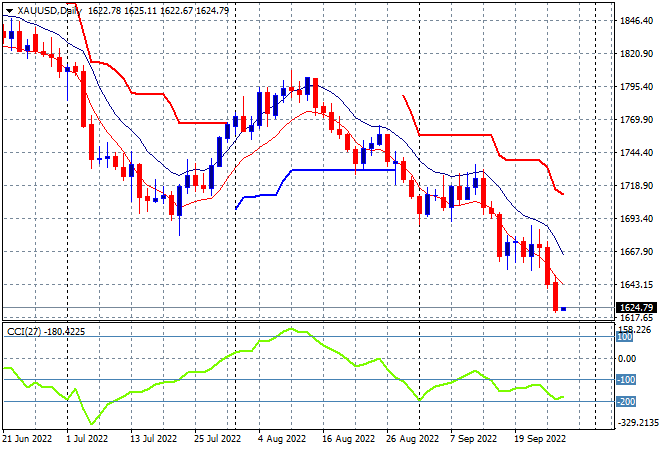

Gold is moving in line with other undollars as the USD remains far too strong against everything, with a further move below the key $1700USD per ounce support level to finish at the $1624USD per ounce level. This takes the shiny metal below the 2020 lows and confirms the multi-monthly bearish setup: