(Bloomberg) -- Asian stocks pared early gains at the start of the last month of 2017 and S&P 500 Index futures declined as the U.S. tax bill encountered stumbling blocks. The dollar headed for its first weekly gain in four weeks ahead of the tax vote.

Japanese shares gave up an advance that briefly helped the Nikkei 225 Stock Average reclaim a 25-year high reached in November. Shares rose in Australia and fell in Hong Kong. The Dow Jones Industrial Average climbed past 24,000 after John McCain backed the Senate tax bill, and the S&P 500 Index capped its longest monthly winning streak since 2007 as technology stocks rebounded. Treasuries held a slide, with the 10-year yield breaking above 2.4 percent. The dollar came under pressure after the U.S. Senate suspended votes on the bill until Friday as it emerged a key compromise to help its passage collapsed.

McCain’s backing of the tax bill prompted optimism on its prospects as it’s headed for a marathon debate on the Senate floor. Senate Majority Leader Mitch McConnell said votes on the tax bill will resume at 11 a.m. on Friday as the collapse of a key compromise to win a majority for a Senate tax overhaul left Republicans scrambling to salvage the legislation.

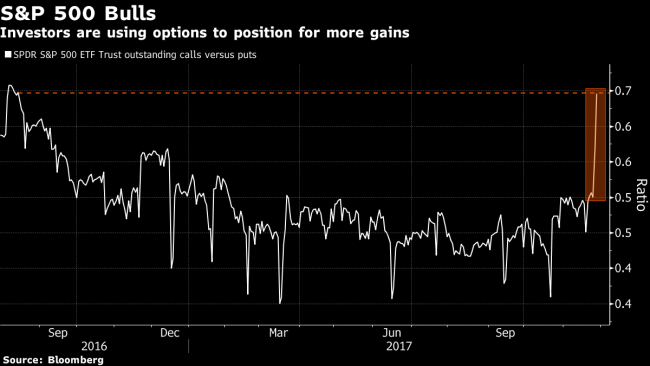

Markets have become sensitive to any progress on U.S. tax reform that would give yet another impetus to an equity bull run into the final weeks of the year that has been fueled by optimism on earnings and economic growth throughout 2017.

Investors will be sifting through key data in Asia on Friday. China’s Caixin manufacturing PMI may slide to 50.9 for November from 51, reflecting credit curbs, the slowing property market, and tighter environmental rules.

Japan’s inflation sped up in October, though price rises are still less than half the central bank’s 2 percent target. In South Korea, inflation unexpectedly slowed to a one-year low and economic growth was slightly stronger than the central bank’s initial estimate.

Meanwhile, Washington politics has again been thrust into the spotlight amid a report that the White House is weighing replacing Secretary of State Rex Tillerson as his relationship with President Donald Trump sours.

Oil posted its longest streak of monthly gains since early 2016 after an OPEC-led coalition of major crude producers followed through on a long-awaited extension of supply cuts.

Terminal subscribers can read our Markets Live blog.

Here are some key events for the remainder of this week:

- Manufacturing in the U.S. probably remained robust in November. The Institute for Supply Management’s index, out Friday, is settling back to a more sustainable pace after climbing to a 13-year high two months earlier in the aftermath of Hurricane Harvey.

- St. Louis Fed President James Bullard and Dallas Fed President Robert Kaplan are scheduled to speak.

- Markets in Indonesia, Malaysia, Pakistan and Sri Lanka are closed for holidays.

These are the main moves in markets:

Stocks

- The Topix index was down 0.2 percent as of 10:50 a.m. in Tokyo and the Nikkei 225 Stock Average fell 0.1 percent after earlier jumping as much as 1.2 percent to touch the highest since 1992.

- Australia’s S&P/ASX 200 Index advanced 0.4 percent. The Kospi index was down 0.1 percent.

- Hong Kong’s Hang Seng Index lost 0.3 percent. The Shanghai Composite Index was down 0.4 percent.

- Futures on the S&P 500 Index fell 0.3 percent. The underlying gauge rose 0.8 percent to a record at the close in New York.

- The MSCI Asia Pacific Index was little changed.

Currencies

- The Bloomberg Dollar Spot Index fell less than 0.1 percent.

- The yen gyrated early in Asia trading and was at 112.52 per dollar.

- The euro traded at $1.1907.

- The British pound was at $1.3534, near the strongest in more than two months, after a 0.9 percent advance.

Bonds

- The yield on 10-year Treasuries was steady at 2.41 percent.

- Australia’s 10-year bond yield advanced three basis points to 2.53 percent.

Commodities

- West Texas Intermediate was little changed at $57.45 a barrel.

- Gold was at $1,275.70 an ounce.