Several inflation prints and Fed Chair Powell’s comment regarding a “soft landing” around combating inflation in the US cause more downside volatility on risk markets overnight as Wall Street rolled over after what looked like a continuation of more positive results from the start of the week. In currency land, Euro continued to push slightly higher against USD, but the King remains on his throne against commodity currencies, with the Australian dollar pushed well below the 70 handle. Bond markets saw a retracement in yields, with 10 Year Treasuries pulling back from 3.3% to 3.1% while interest rate futures came back slightly to only indicate 190 bps in rate rises by the Fed this year. Commodity prices fell back again, with oil prices the sharpest, with Brent falling nearly 4% while gold again slipped well below the $1850USD per ounce level.

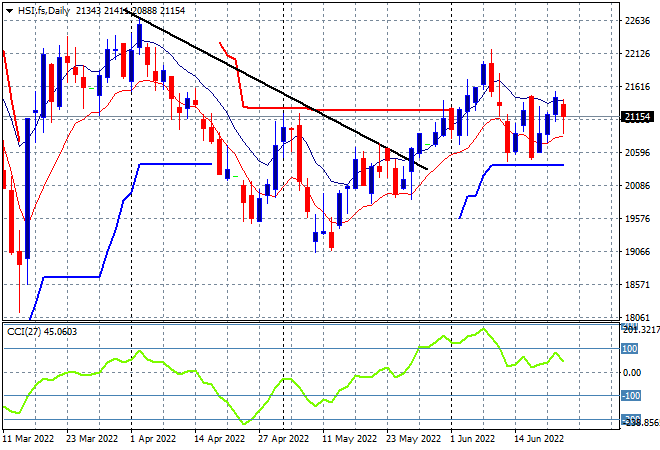

Looking at share markets in Asia from yesterday’s session, where Chinese share markets were quite negative with the Shanghai Composite down some 1.2% to close at 3267 points while the Hang Seng Index took back most of its gains for the week, down 2.5% to close at 21008 points. The daily chart was showing price anchored at trailing daily ATR support at the 20500 point level with daily momentum barely positive before the recent bounce and this lack of overbought momentum is telling. Price action is still a fair way from the May lows at the 19000 point level, but the overall market remains well contained:

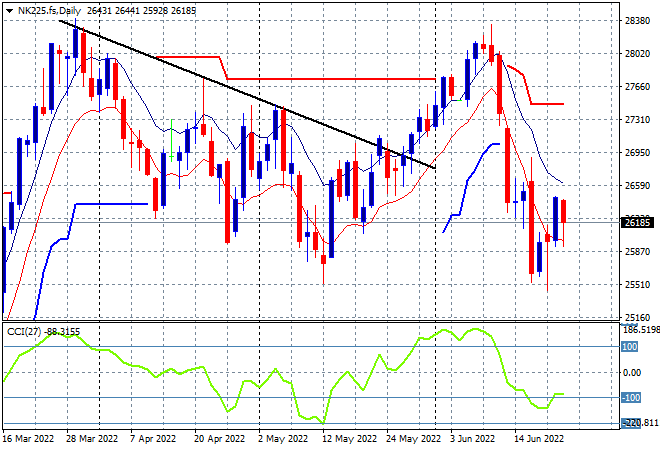

Japanese stock markets slipped slightly with the Nikkei 225 index closing 0.4% lower at 26149 points. The daily futures chart of the Nikkei 225 was showing a very solid start to the trading week, with a much weaker Yen not yet translating into sustainable gains here as price action is not yet back above the key high moving average level. Watch daily momentum readings however which need to get back out of the oversold zone:

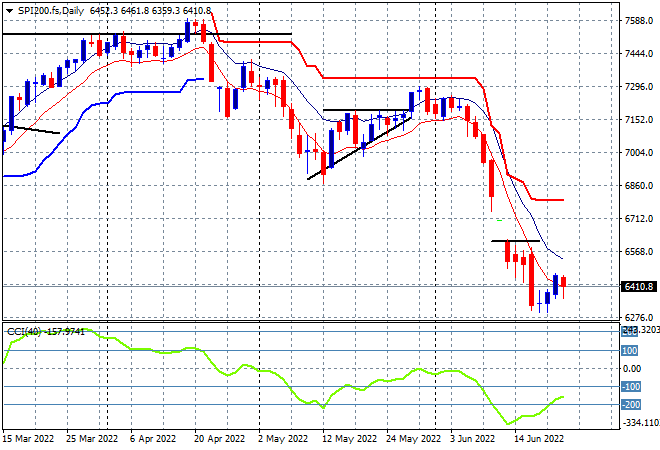

Australian stocks also fell behind with the ASX200 finishing more than 0.2% lower at 6508 points. SPI futures are up around 0.4% or approx. 30 points, so there is a possibility of reclaiming that loss, but the overall volatility on Wall Street may weaken confidence here through the session. The daily charts continue to show price that needs to recover well above the 6600 point level before calling any bottoming action as daily momentum is still in the very oversold zone:

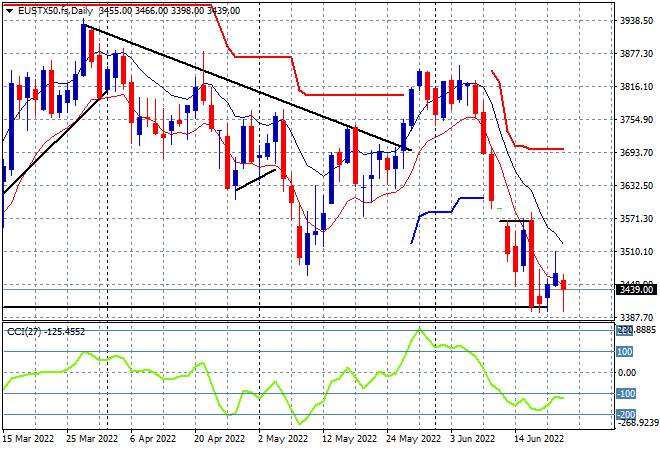

European stocks again were looking positive out the gate, but the slump in the recent consumer confidence figures and the latest UK inflation data saw a broad pullback, with the Eurostoxx 50 index eventually closing some 0.8% lower at 3464 points. The daily chart picture remains bearish at best as price hovers right on the previous daily/weekly lows from the March dip. Daily momentum remains in quite an oversold position with price needing to get back above the 3570 point area very quickly or it will roll over here:

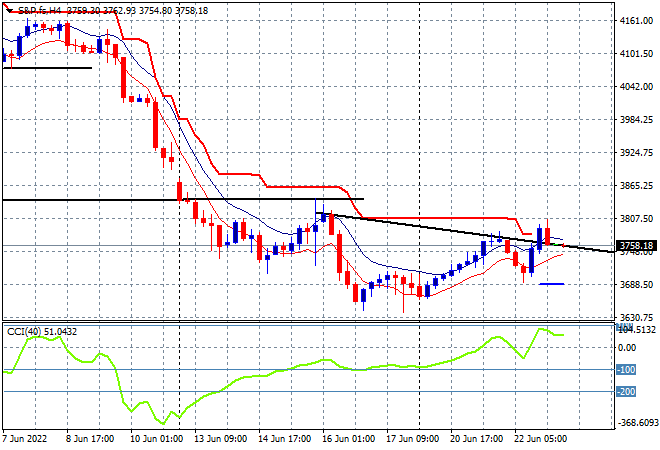

Wall Street had another roller coaster ride overnight, hinging on Powell’s comments with all three bourses eventually putting in minor scratch sessions after being up mid-session. The S&P500 closed 0.1% lower at 3759 points with the four hourly chart still showing a very weak picture, as hesitation remains below the March lows which are not yet filled (lower horizontal black line). To recover out of this correction requires a rally that must go through the 3845 point area, the lows from last week and then back up through the psychologically important 4000 point zone:

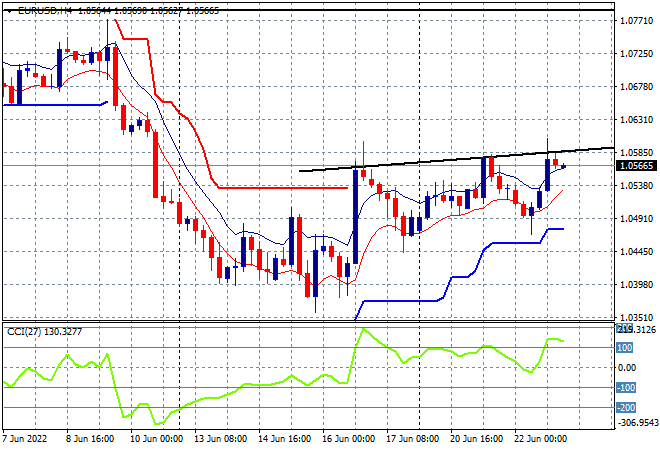

Currency markets were somewhat contained alongside their stock market cousins, with the USD still dominating against the commodity currencies yet Euro is continuing to outperform. The union currency lifted again overnight, almost making a new two week high as it tries to push up through the 1.06 handle but continues to find strong resistance. While traders might be anticipating more ECB rate rises on the back of the BOE/SNB rises, as I said last week this repricing maybe temporary given the 75bps scheduled by the Fed next month, so watch for any retracement below former trailing ATR resistance at the 1.0540 level here:

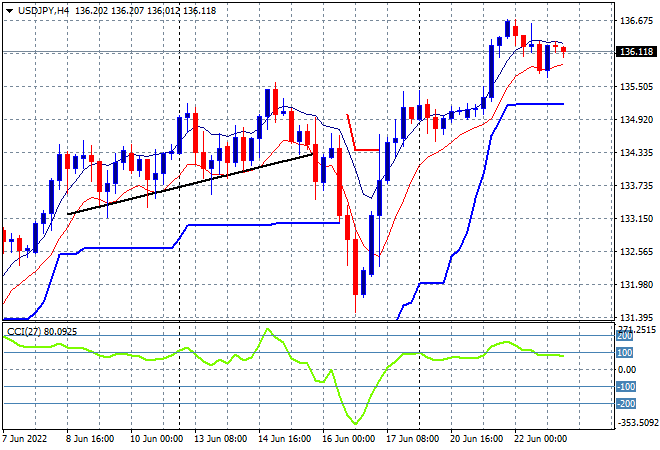

The USDJPY pair stabilised again overnight, consolidating post another big breakout as Yen selling abated slightly above the 136 handle. We’re likely to get another session of stability before another breakout soon, using trailing ATR support at the 135 area as the uncle point. Watch for four hourly momentum as it crosses back above overbought levels as a precursor:

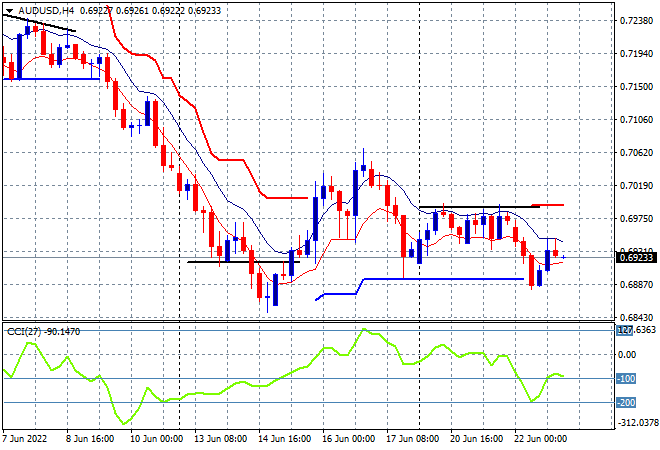

The Australian dollar still can’t get any momentum having rolled over last week as its bounce back above the 70 handle remains stuck, with overnight price action not only keeping it contained below that level but crushed below the 69 cent level, almost matching the previous weekly low. My contention of a retracement below the 69 handle still holds as the Fed well remains ahead of the hapless boffins at Martin Place:

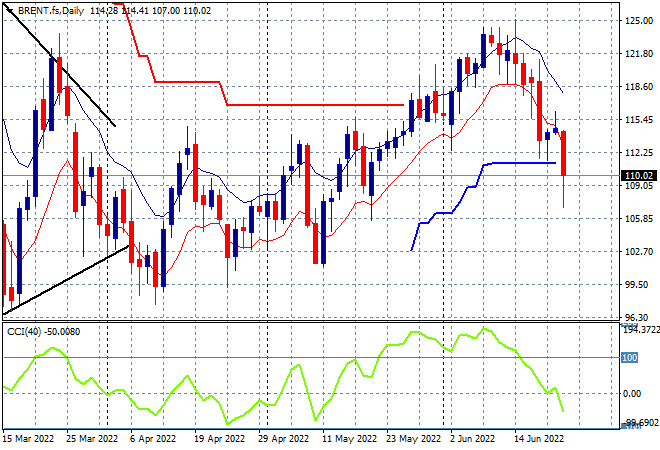

Oil markets are failing to stabilise after a series of lower lows that saw Brent crude overnight cross deeply below the $110USD per barrel level in a sharp inversion. Daily momentum has retraced fully from its overbought status with price no longer supported at the $115 area and has crossed below ATR trailing support level as well. This could turn into a push down to the $100 psychological support level next, and very swiftly:

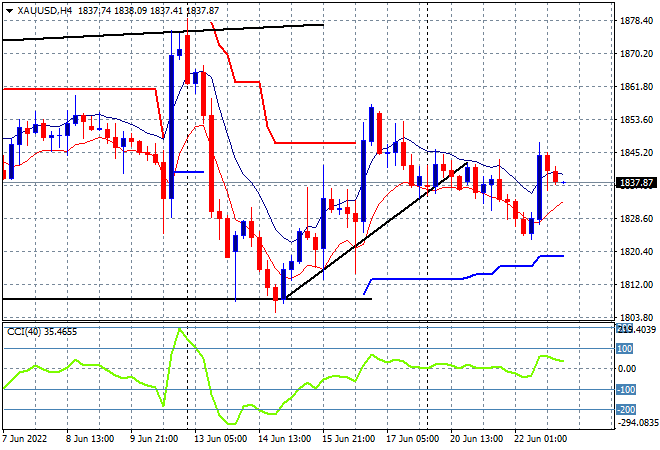

Gold still can’t get out of its sideways bearish oscillation with another false move higher that again turned into a retracement overnight as resistance continues to firm at the $1850USD per ounce level. Daily momentum remains negative as four hourly momentum rolls over, and while the recent bounce off the $1800USD per ounce level is a good sign of a bottom forming, the short term trend is showing a series of lower low sessions, so its not yet enough to convince more buyers to step in:

Which stock should you buy in your very next trade?

AI computing powers are changing the stock market. Investing.com's ProPicks AI includes 6 winning stock portfolios chosen by our advanced AI. In 2024 alone, ProPicks AI identified 2 stocks that surged over 150%, 4 additional stocks that leaped over 30%, and 3 more that climbed over 25%. Which stock will be the next to soar?

Unlock ProPicks AI