With Wall Street and other US markets closed for a holiday, momentum from Friday night’s exuberance on risk markets was enough to carry over and lead to more upside overnight. The record high German inflation print – now pushing 8% annualised – kept Euro elevated against USD while the bond futures market saw implied yields for 10 Year Treasuries push up towards the 2.8% level again. The Australian dollar continued to soar, having broken out above the 71 cent level alongside stocks, it almost hit the 72 level this morning. Commodity prices were somewhat bullish although with several physical markets closed it was hard to get a decent read, with Oil prices lifting slightly, while gold hovered just above the $1850SD per ounce level .

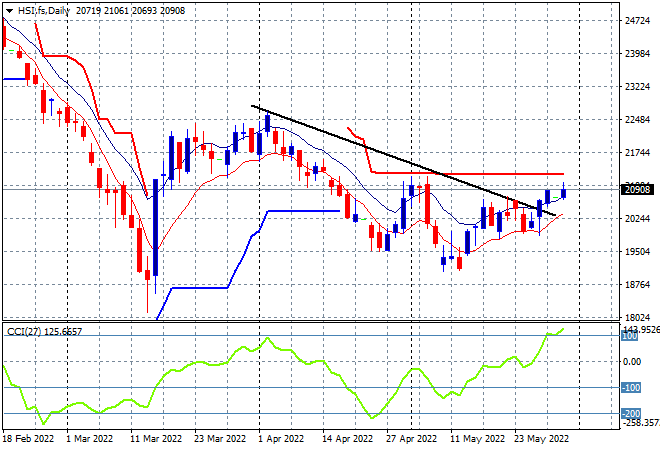

Looking at share markets in Asia from yesterday’s session, where mainland Chinese share markets continued their rebound with the Shanghai Composite closing up 0.6% to 3148 points while the Hang Seng Index built on its Friday gains, closing up nearly 2% to 21109 points. The daily chart is showing price action getting more steam under it again but it remains contained below trailing daily ATR resistance at the 21000 point level that has firmed as strong resistance:

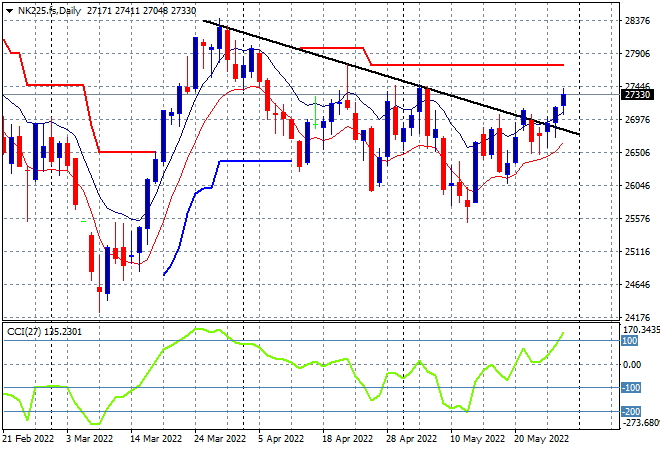

Japanese stock markets were the strongest in the region however, with the Nikkei 225 index gaining more than 2% to close at 27369 points. The daily chart of the Nikkei 225 still has a bearish bent with another attempt to get back above the previous daily/weekly highs near the 27500 point level possibly underway as risk sentiment firms. To properly reverse the downward trend from the March highs requires a substantial move above the 27000 point level with futures indicating more upside on the open as Yen weakened appreciably overnight:

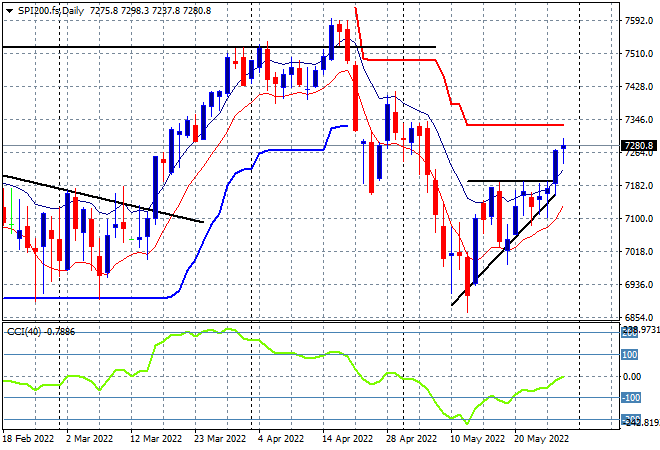

Australian stocks put in a very solid session to start the trading week, with the ASX200 closing more than 1.8% higher at 7286 points. SPI futures are down around 0.2% due to the lack of a lead from Wall Street overnight. The daily chart is showing a super clear breakout here with resistance at the 7200 point level to be cleared very quickly, even though daily momentum readings remain negative, it is normalising:

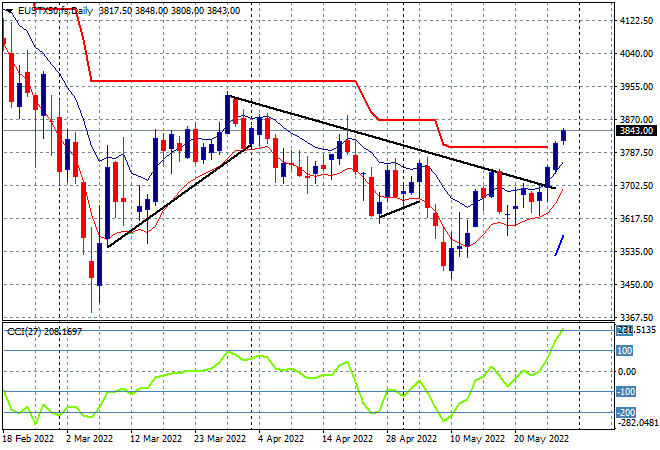

European markets did well overnight but pared some of their gains at the close without a catalyst from a closed Wall Street, with some peripheral markets putting in scratch sessions. Overall, the Eurostoxx 50 index finished 0.9% higher at 3841 points. The daily chart picture is showing a continued breakout that has now moved above trailing ATR resistance that has been keeping this market contained since the Ukrainian invasion. With daily momentum flipping to the positive side, the upside potential is the 4000 point level:

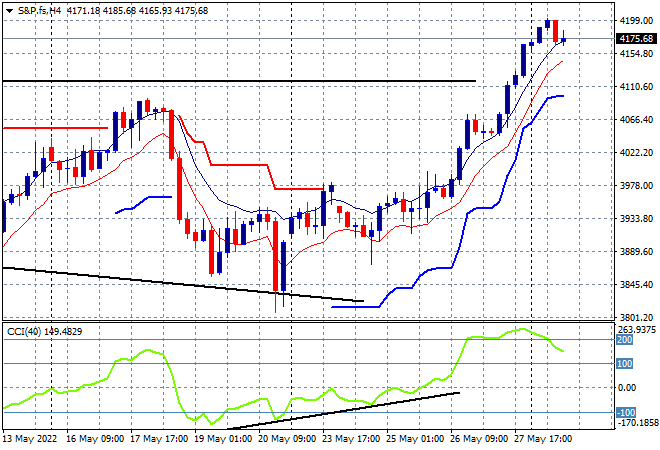

Wall Street was closed for the Memorial Day holiday with equity futures indicating more upside when physical markets reopen later tonight. The four hourly chart of the S&P500 shows a continued surge above the 4100 point previous resistance level, but there is the possibility of some buying exhaustion settling in as daily momentum is only barely positive so far:

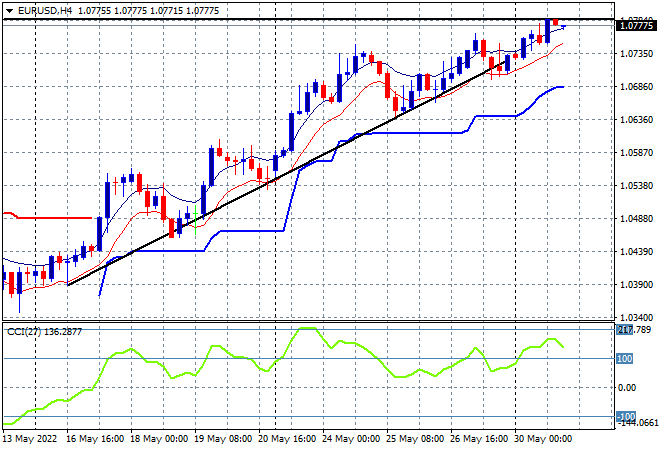

Currency markets saw continued USD weakness without a lead from US traders on a long weekend holiday. The record high German inflation data helped Euro’s cause with the union currency pushing towards the 1.08 handle and almost getting back above the 2020 lows (upper horizontal black line). This continues this medium term uptrend that has been solidified as trailing ATR support at the 1.06 level proper was defended and then raised:

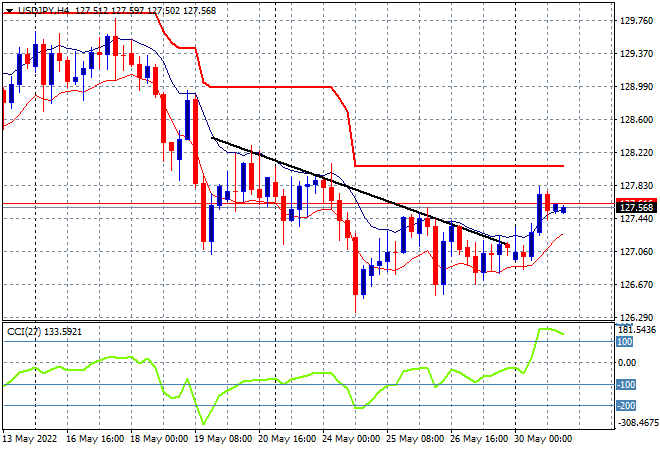

The USDJPY pair finally found some life overnight with Yen buying taking a back seat with a surge through the 127 mid- level that has held on this morning. This catch up play to other risk markets that have been rallying with new breakouts is overdue and breaks the bearish descending triangle pattern on the four hourly chart that had been forming for almost two weeks. Short term momentum has switched to slightly overbought as a result, but trailing ATR resistance at the 128 handle proper has not yet been negated, so I remain cautious here:

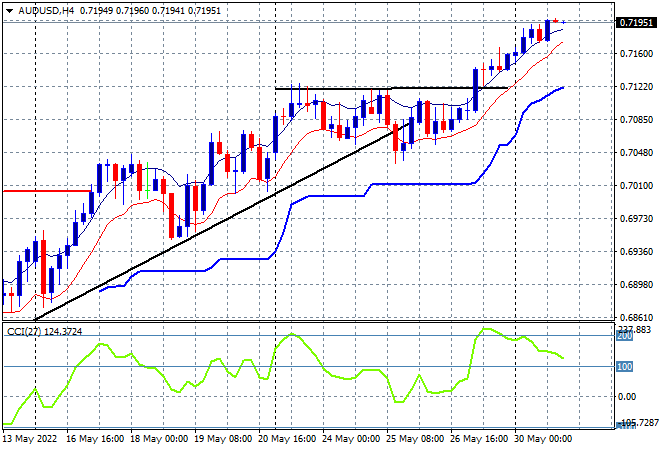

The Australian dollar was almost able to push through the 72 handle overnight, continuing its push from the Friday night moves alongside other risk markets. Four hourly momentum is retracing from its extremely overbought levels so we could still see a small retracement as short term price action seems to be hitting substantial resistance at the 72 cent level, or it could be more positioning before yet another breakout. The previous resistance level at 71 cents (upper black horizontal line) should provide solid support going forward:

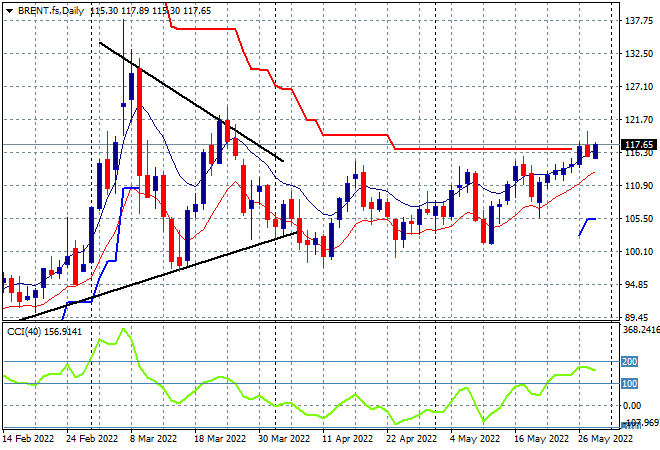

Oil markets were relatively calm overnight with a small lift across WTI and Brent futures despite a closed CBOT due to the US long weekend. Brent eventually finished slightly above the $117USD per barrel level and while this still exceeds its previous weekly high, it keeps price hovering near the trailing ATR daily resistance at the $116 area. Daily momentum is very overextended and properly overbought so that could encourage further upside as US traders return tonight:

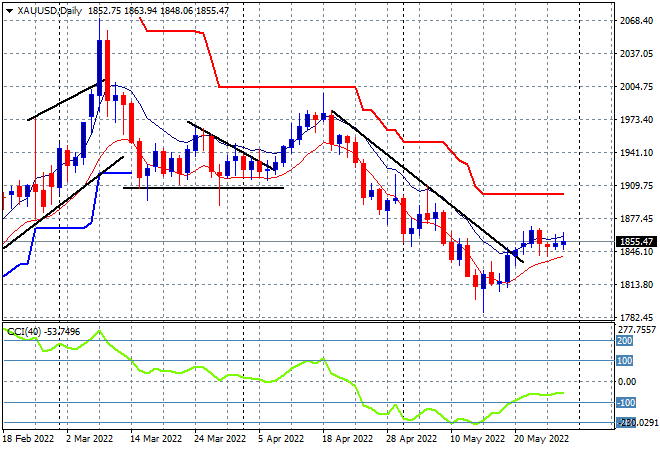

Gold stalled out once again overnight, lacking US traders to provide any upside potential with another close just above the $1850USD per ounce level, despite the USD remaining weak against the majors. While the downtrend from the April highs is likely over, daily momentum remains stuck in negative territory, with an inability to create a new daily high for over a week now weighing on price action. The January lows around the $1800 level remain the downside target that has yet to transform into a new support level: