Overnight saw another weak session for Wall Street despite some solid domestic data as consumer confidence fell back slightly but still higher than expectations with European stocks leading the way instead on the lower Euro. The USD rose slightly against all the currency majors with the Australian dollar still struggling as it failed to make any headway above the 65 cent level again.

10 year Treasury yields rose slightly to the 4.25% level, still a little off of their four month high, while Brent crude fell back following the weekend gap with a move back to the $86USD per barrel level. Meanwhile gold reduced in volatility somewhat to eventually close just above the $2170USD per ounce level.

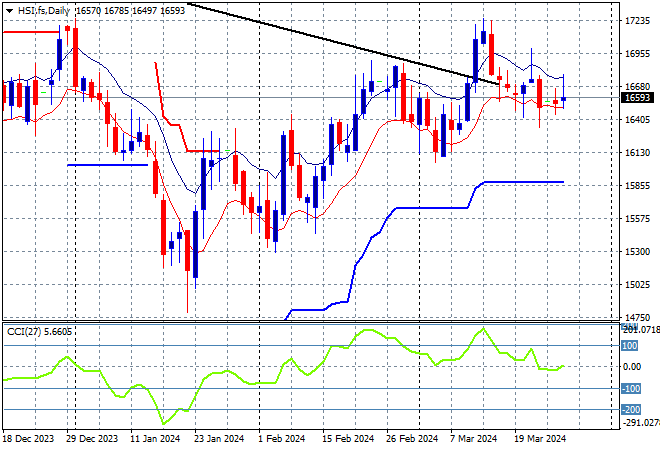

Looking at markets from yesterday’s session in Asia, where mainland and offshore Chinese share markets are trying to make a comeback after failing to get back on track recently with the Shanghai Composite closing slightly higher while the Hang Seng managed a near full 1% bounce to close at 16618 points.

The daily chart was starting to look more optimistic with price action bunching up at the 16000 point level before breaking out in the previous session trying to make a run for the end of 2023 highs at 17000 points with the downtrend line broken. However this has been thwarted as monthly resistance levels are kicking in:

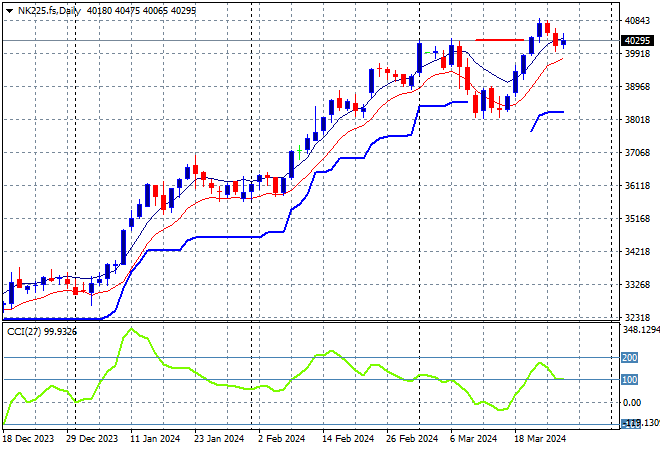

Japanese stock markets were a bit more hesitant, with the Nikkei 225 putting in a scratch session at 40398 points.

Trailing ATR daily support was never threatened by price action after this bounce went beyond the September highs at the 33000 point level with daily momentum getting back to overbought readings with a significant breakout. Last week saw this reversed as momentum goes negative and the selloff back to ATR support at 38000 points taking the wind out of this trend. This reversal has given new life here however:

Australian stocks were the worst performers with the ASX200 closing some 0.4% lower at 7780 points.

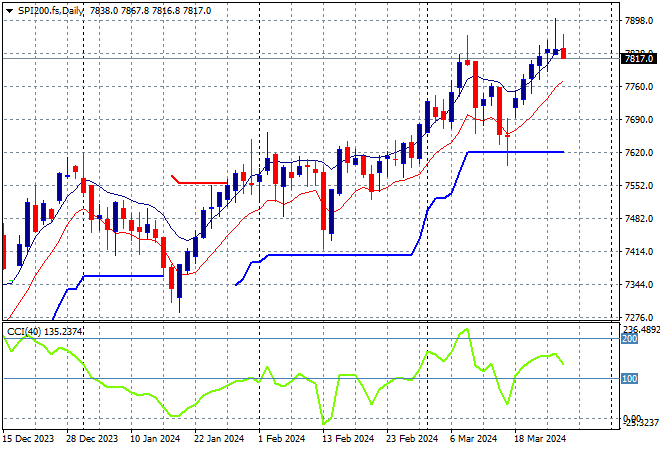

SPI futures are down nearly 0.3% following the poor showing on Wall Street overnight. The daily chart was looking firmer with the medium term uptrend and short term price action coming together to take out the previous December highs. As I said previously, watching for any continued dip below the low moving average could see a significant pullback but watch ATR support which has been defended so far:

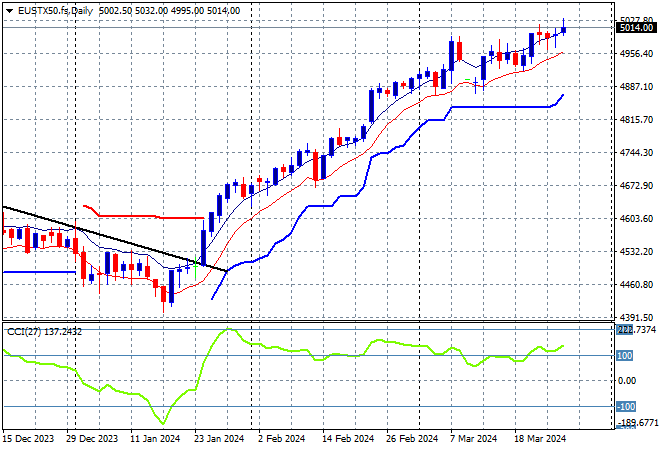

European markets were better across the board with the German DAX dominating again as the Eurostoxx 50 Index eventually finished 0.4% higher at 5064 points.

The daily chart shows price action still on trend after breaching the early December 4600 point highs but daily momentum retracing slightly out of an overbought phase. This is looking to turn into a larger breakout as futures indicate another rise for tonight’s session:

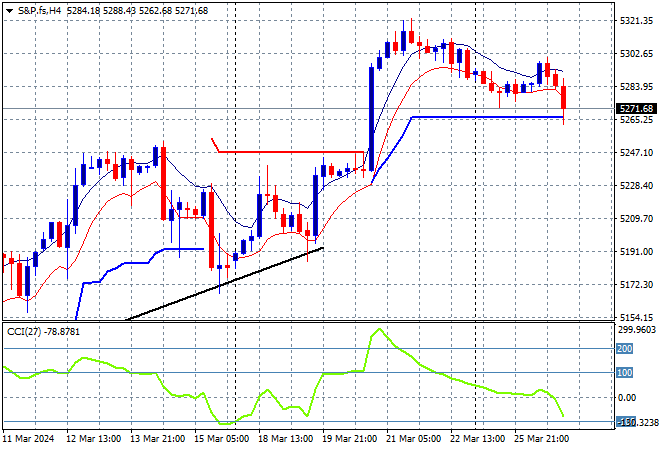

Wall Street couldn’t continue its upbeat mood from last week as the NASDAQ was off by 04% while the S&P500 lost nearly 0.3%, closing at 5203 points.

The four hourly chart shows this slight consolidation back to a more sustainable uptrend with short term support coming up soon while equally short term momentum retraces to a negative setting:

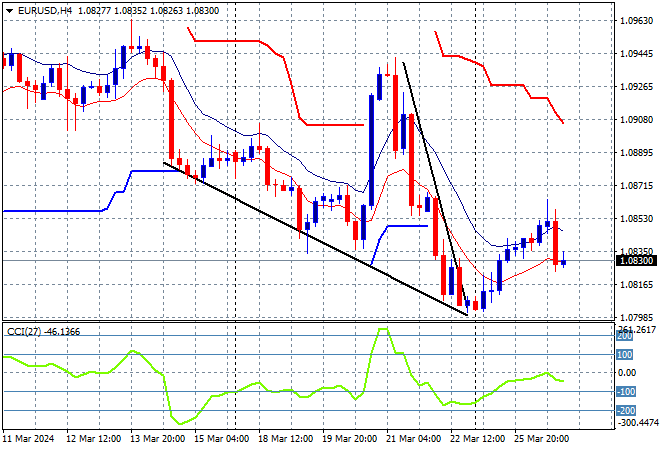

Currency markets saw the most volatility last week in the wake of the BOE and Swiss meetings, with an initial breakout against USD that turned into a big reversal on the Swiss cut with most of the majors retreating against King Dollar. Euro has tried to buck the trend with a small breakout above the 1.08 level on a falling wedge pattern but this was overturned last night as it settled just above that handle.

The union currency seems to have support anchored at the 1.08 level which is where it ended up but the short term price action is now suggesting a return to that level given that short term momentum is nowhere near positive yet:

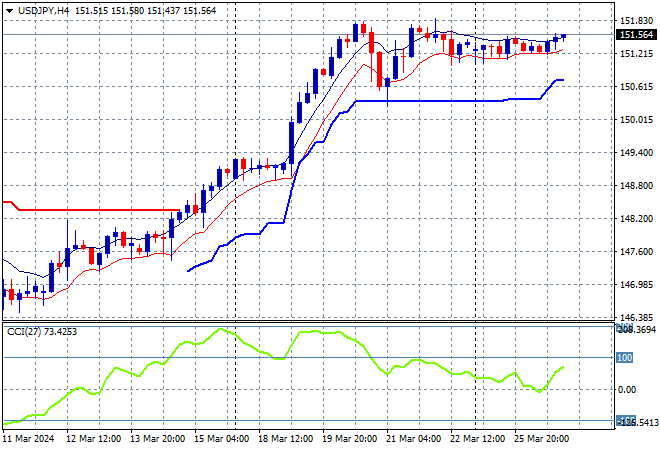

The USDJPY pair was able to nearly get back to its pre-Fed meeting high with a minor bounce above the mid 151 level overnight.

The medium term picture was looking very optimistic as Yen sold off due to BOJ meanderings but momentum is now trying to get back into overbought mode while ATR support remains firm at the 150 handle proper:

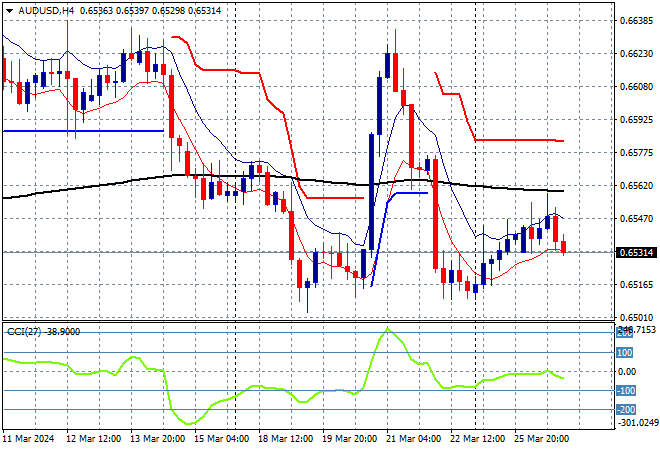

The Australian dollar wanted to return to its weekly highs but failed again with a pullback to short term support and below the 66 cent level as it now dices with longer support at the 65 cent area.

The Aussie has been under medium and long term pressure for sometime before the RBA and Fed meetings and while this surge looked strong, it wasn’t overbought on the four hourly chart and had not surpassed support from last week’s consolidation phase. Watch for the 66 cent handle to firm as resistance here going into today’s monthly CPI print:

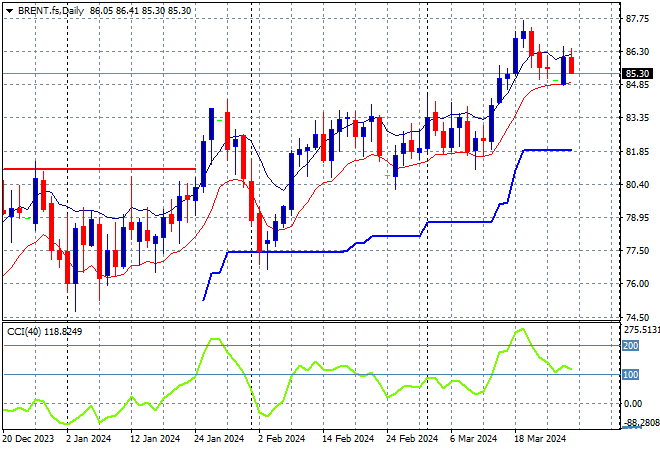

Oil markets are pausing their breakouts following the attacks on Russian refineries with Brent crude pushed slightly lower to settle just below the $86USD per barrel level, still well above the previous weekly highs.

After retracing down to trailing ATR daily support at the $77 level, price had been bunching up around the February highs at the $84 level with short term momentum definitely overbought and signalling potential upside from here:

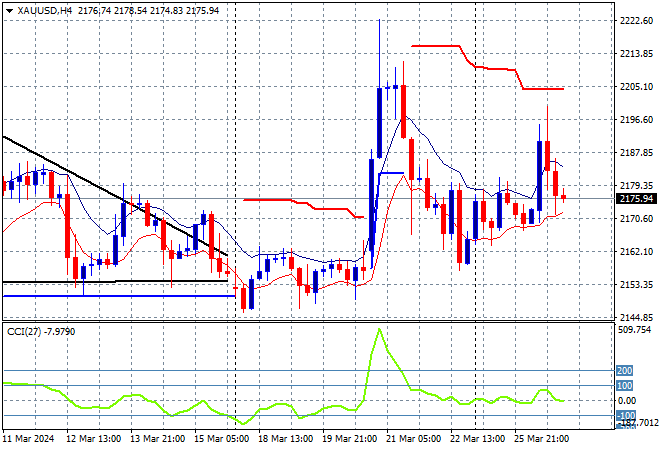

Gold had previously surged above the $2200USD per ounce level in the wake of the soft Fed meeting outcome but this has been thwarted with a series of very volatile sessions that has seen it return back to the $2170 level for a possibly more sustainable trajectory.

Last week daily momentum was nearly off the charts – never a good sign – with short term support at the $2000 level turning to what could be rock solid medium term support but still the critical area to watch ahead on a likely pullback due to excessive volatility: