Risk markets pivoted overnight on both the latest ISM services print and Fed Chair Powell’s speech, where he posited that rate cuts are on the way, but perhaps not too soon. The ISM was weaker than expected which sent bond markets on a round trip while Wall Street was able to get back into the green, but only just by the end of the session. There was more action in currency markets as the USD weakened appreciably across the board with the Australian dollar managed to get back above the mid 65 cent level for a new two week high.

10 year Treasury yields eventually finished where it started on the macro volatility while Brent crude pushed further above the $89USD per barrel level for another new weekly high. Meanwhile gold is surging irregardless of USD direction, almost pushing through the $2300USD per ounce level.

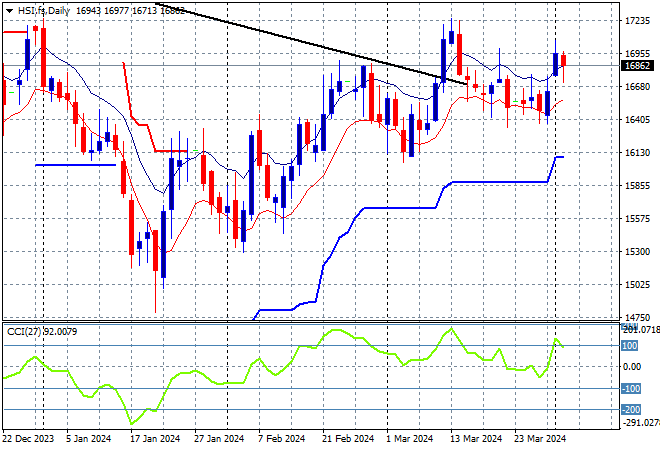

Looking at markets from yesterday’s session in Asia, where mainland and offshore Chinese share markets are going in the same direction – down – with the Shanghai Composite holding above the 3000 point level but falling about 0.3% while the Hang Seng has lost more than 1.2%, closing at 16726 points.

The daily chart was starting to look more optimistic with price action bunching up at the 16000 point level before breaking out in the previous session trying to make a run for the end of 2023 highs at 17000 points with the downtrend line broken. However this has been thwarted as monthly resistance levels are kicking in, although support is firming at the 16400 point area:

Japanese stock markets were also off, with the Nikkei 225 closing nearly 1% lower at 39451 points.

Trailing ATR daily support was never threatened by price action after this bounce went beyond the September highs at the 33000 point level with daily momentum getting back to overbought readings with a significant breakout last month above the 40000 point level. This has now turned into short term resistance so watch for a further retracement below:

Australian stocks had the worst performance with the ASX200 closing over 1.3% lower to 7782 points.

SPI futures are up 0.3% on the rebound on Wall Street overnight but this could fizzle out at the open. The daily chart was looking firmer with the medium term uptrend and short term price action coming together to take out the previous December highs. As I said previously, watching for any continued dip below the low moving average could see a significant pullback but watch ATR support which has been defended so far:

European markets were able to put green on the board but it was mainly the German DAX that did the lifting as peripheral bourses were steady as the Eurostoxx 50 Index finished 0.5% higher at 5069 points.

The daily chart shows price action still on trend after breaching the early December 4600 point highs but daily momentum retracing slightly out of an overbought phase. This is looking to turn into a larger breakout as futures indicate another pullback for tonight’s session:

Wall Street had a relatively volatile session given the ISM print but eventually finished slightly higher although the headline Dow fell back, the NASDAQ gained 0.2% while the S&P500 put on just 0.1% to finish at 5211 points.

The four hourly chart shows a consolidation possibly turning into a reversal here as price action pushes through short term support while momentum swiftly gets into a negative phase. Watch for any break below the 5240 point area:

Currency markets finally put in a proper reversal against USD following Fed Chair Powell’s comments with a surge against King Dollar across the board, fuelled by the minor reversal in the previous session. Euro was able to push through the 1.08 handle overnight but was not alone in its move higher.

The union currency seemed to have support anchored at the 1.08 level but the medium term price action was always suggesting a return to or below that level but this reversal in momentum in the short term is likely to see the 1.09 level come under threat next:

The USDJPY pair was unable to make many gains despite what looked like a very good breakout setup on the four hourly chart with the falling USD reloading this potential for another move later in the week as it consolidates at the mid 151 level.

The medium term picture remains very optimistic as Yen sold off due to BOJ meanderings but momentum is now trying to get back into overbought mode while ATR support remains firm at the 151 handle proper:

The Australian dollar was able to bounce strongly alongside other undollars with a move back to the mid 65 handle making a new two week high.

The Aussie has been under medium and long term pressure for sometime before the RBA and Fed meetings and while the previous temporary surge looked strong, it wasn’t overbought on the four hourly chart and had not surpassed support from last week’s consolidation phase. While this looks good in the short term, longer term resistance is likely to kick in at the 66 cent handle:

Oil markets are continuing their breakouts following the attacks on Russian refineries with Brent crude again pushing higher to settle just below the $90USD per barrel level, exceeding the previous weekly highs.

After retracing down to trailing ATR daily support at the $77 level, price had been bunching up around the February highs at the $84 level with short term momentum definitely overbought and signalling potential upside from here, although slightly overextended:

Gold just keeps climbing to new highs through any volatility with another surge overnight despite the reversal in USD pushing the shiny metal almost through the $2300USD per ounce level, closing at the $2299 level as of this morning.

Last week daily momentum was nearly off the charts – never a good sign – with short term support at the $2100 level turning to what could be rock solid medium term support but still the critical area to watch ahead on a likely pullback due to excessive volatility. So far though – no signs of any stopping: