Wall Street continued higher for another record high overnight but it wasn’t as convincing as it looked with European markets also continuing their rebound from oversold conditions, with the latest US retail sales print coming in slightly softer than expected. The USD was mixed again with Euro and Pound Sterling coming back a little stronger while the Australian dollar held on to its post RBA meeting gains well above the 66 cent level.

10 year Treasury yields pulled back on the soft retail sales data losing some 6 points to the 4.2% level while oil prices were able to surge higher with Brent crude finishing above the $85USD per barrel level. Gold was able to lift about $10 but is still stuck just above the $2300USD per ounce level.

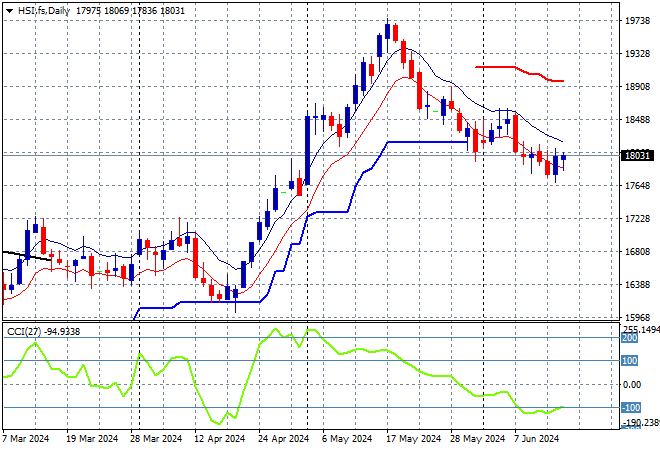

Looking at markets from yesterday’s session in Asia, where mainland Chinese share markets are finally finding some positive momentum with the Shanghai Composite up more than 0.5% while the Hang Seng Index has put in another scratch session closing at 17921 points.

The Hang Seng Index daily chart was starting to look more optimistic with price action bunching up at the 16000 point level before breaking out in the previous session as it tried to make a run for the end of 2023 highs at 17000 points with the downtrend line broken. Price action was looking way overextended but this retracement is now taking some heat out of the market but needs to stop soon before moving into corrective mode:

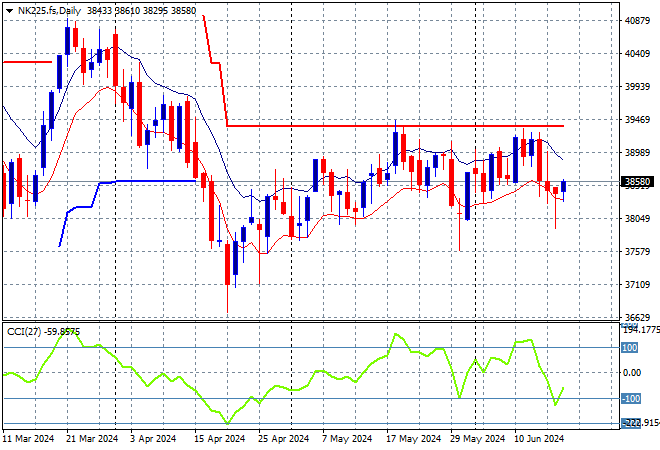

Meanwhile Japanese stock markets are trying a little harder to get out of their holding pattern with the Nikkei 225 up 1% to 38482 points.

Price action had been indicating a rounding top on the daily chart with daily momentum retracing away from overbought readings with the breakout last month above the 40000 point level almost in full remission. Short term resistance had been defended with short term price action now rebounding off former support at the 39000 point level with short term momentum still positive although futures are indicating a small lift on the open:

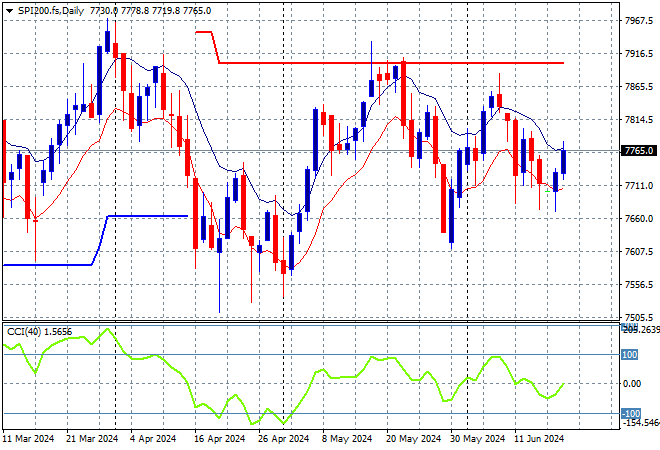

Australian stocks were able to put in a very solid session despite the RBA hold with the ASX200 closing 1% higher to 7778 points.

SPI futures are steady reflecting the very mild moves higher overnight on Wall Street. The daily chart was showing a potential bearish head and shoulders pattern forming with ATR daily support tentatively broken, taking price action back to the February support levels in mid April. Momentum is finally getting out of its oversold condition but has been unable to get back into positive territory with a return to the 7900 point level not yet on the cards:

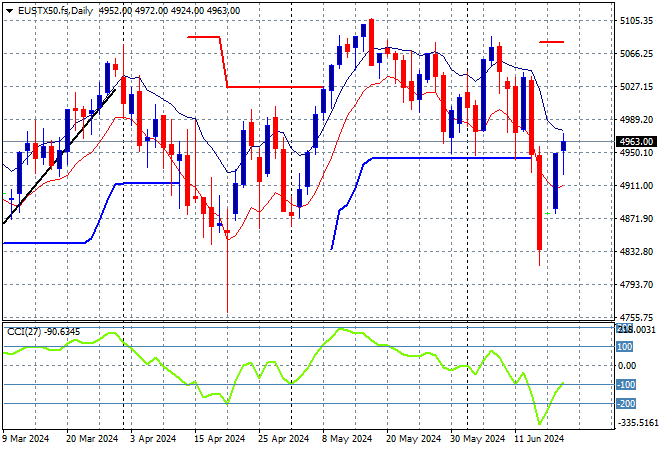

European markets remain somewhat volatile but their were continued rebounds across the continent with the Eurostoxx 50 Index gaining nearly 0.8% to close at 4915 points.

The daily chart shows price action off trend after breaching the early December 4600 point highs with daily momentum retracing well into an oversold phase. This was looking to turn into a larger breakout with support at the 4900 point level quite firm with resistance still looming at the 5000 point barrier. ATR support has been taken out here which is ominous:

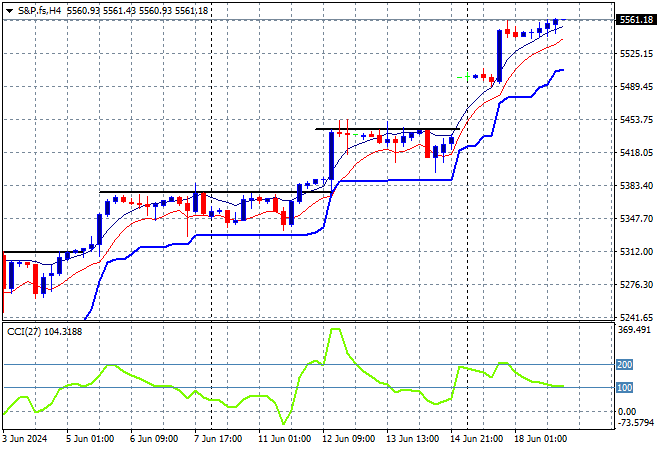

Wall Street is still pushing higher although the NASDAQ ended up with a scratch session, while the S&P500 gained 0.2% to extend its gains above the 5400 point level, closing at 5487 points.

The four hourly chart showed the Friday night rebound coming up against a lot of hesitation at the 5300 point level with short term momentum ready to launch higher. The consolidation phase with a small breakout now has legs as the 5400 point target level is swept away:

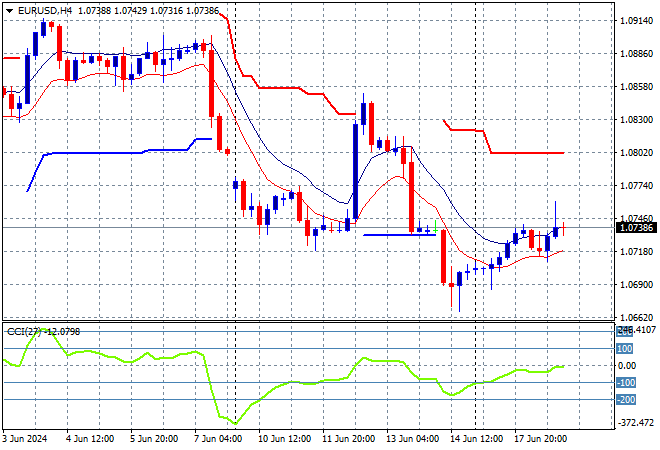

Currency markets are still somewhat feeling the effects of a dominant USD but Euro is coming back slightly after a week of downside volatility, helped by the soft US retail sales print overnight, maintaining above the 1.07 handle as Pound Sterling also recovered slightly.

The union currency had previously bottomed out at the 1.07 level at the start of April as medium term price action with a reprieving reversal in price action back towards the 1.09 level before its own inflation print. Medium term support at the mid 1.07 level is still firm but may come under increasing pressure from here:

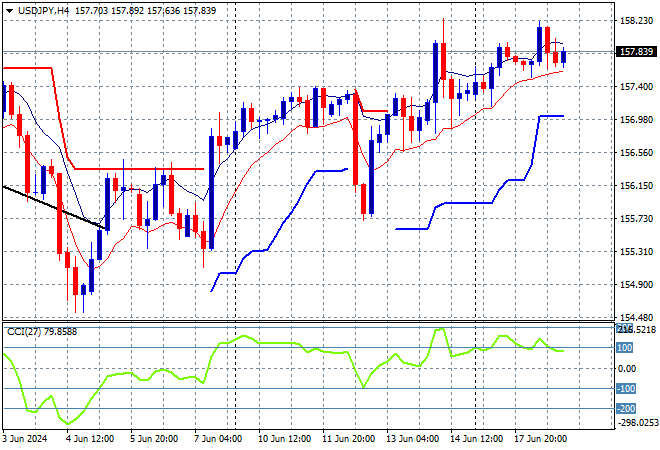

The USDJPY pair was able to hold on but failed to make any new session highs overnight, staying above the mid 157 handle as of this morning and almost matching the previous weekly high.

Short term momentum had gotten out of oversold condition but was not yet positive with price action suggesting a further pause or rollover here before the print with this move taking the pair back to last week’s finishing point. This volatility speaks volumes as it shows the 158 level looming as longer term resistance overall with more range bound price action expected:

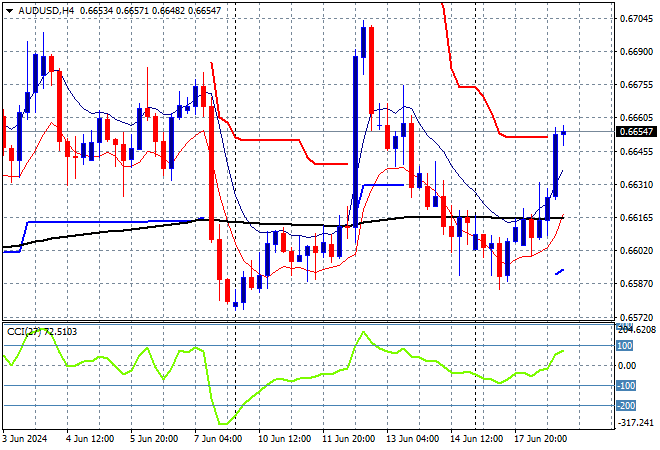

The Australian dollar is trying to get back to its post US CPI one off high at the 67 cent level as North Atlantic traders held on to the Asian gains following yesterday’s interest rate decision by the RBA, with price settling just above the mid 66 cent level.

So far the Pacific Peso hadn’t been able to take advantage of any USD weakness with momentum barely in the positive zone in recent weeks with price action whipsawing around the mid 66 cent level as a point of control. Watch the 66 handle to come under threat again however as this remains unconvincing:

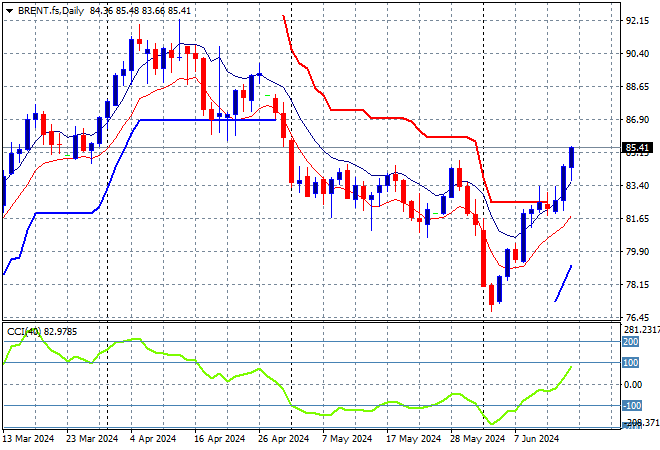

Oil markets are almost out of correction mode with another strong session overnight as Brent crude moved higher to well above the $85USD per barrel level.

After breaking out above the $83 level last month, price action has stalled above the $90 level awaiting new breakouts as daily momentum waned and then retraced back to neutral settings. Watch daily ATR support here at the $86 level which is still broken and will likely be resistance for sometime with short term momentum trying to get out of negative mode:

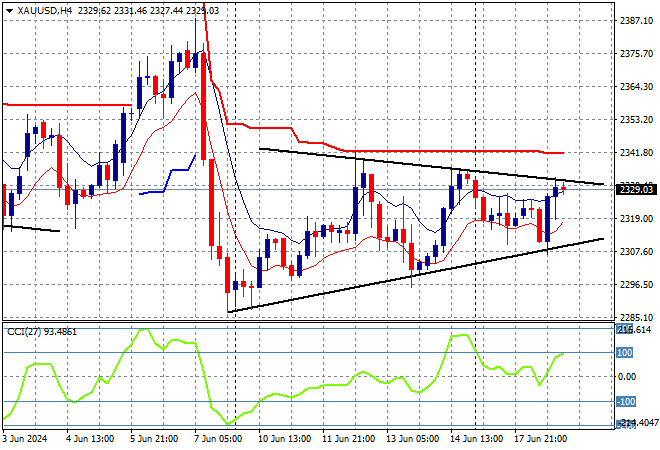

Gold only had a mild rebound on the CPI print last week with a lift up towards the mid $2300USD per ounce level, but was unable to make it stick, and remains in a sideways bearish mood.

Still the biggest casualty of the US jobs report on Friday night, the shiny metal has bounced off its weekly low with short term momentum now neutral but not yet clearing short term ATR resistance overhead: