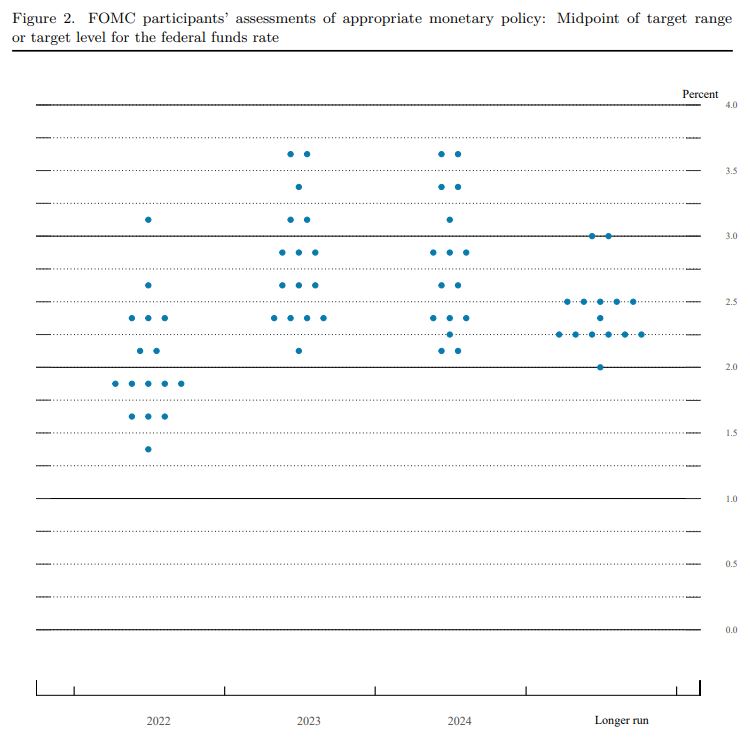

The US Federal Reserve’s FOMC raised its funds rate by 25bp to a mid-range of 0.375%, as was widely expected. Guidance was slightly more hawkish than expected, though, with the dot plot projection medians showing a hike at every meeting in 2022, taking the rate to 1.875% by year-end, and 2.75% by end-2023. In his press conference, Chair Powell said the Fed plans to lift rates “steadily.” He said the probably of a recession this year is “not particularly elevated” and that this is a strong economy that can “flourish” in the face of tighter policy. Every meeting is a live one and if it is appropriate to move more quickly, the Fed will do so. On the balance sheet, he said they are making “excellent progress” and suggested an announcement on particulars could come as soon as the next meeting in May.

US retail sales in February rose 0.3%m/m (est. +0.4%m/m). The core measure (control group) fell 1.2%m/m (est. +0.3%m/m). However, there were large positive revisions to January. NAHB homebuilder sentiment survey fell to 79 (est. 81, prior 81), but remains elevated. The report cited strong sales despite concerns over affordability, higher inflation and prospective interest rises. Business inventories in January rose 1.1%m/m (est. 1.1%, prior +2.4%m/m).

Canadian CPI in February rose 1.0%m/m (est. +0.9%m/m) and 5.7%y/y (est. 5.5%y/y), underlying core measure also firmer.

Ukraine and Russia showed some signs of progress in negotiations, Kremlin spokesperson Peskov saying a proposal for Ukraine to become a neutral country but retaining its own armed forces “could be viewed as a certain kind of compromise.” Ukrainian President Zelenskiy said Russia’s “positions in the negotiations sound more realistic”.

Event Outlook

Aust: Given the recent floods in NSW and QLD have come after the February reference period, Westpac anticipates employment to lift by 60k for the month (market consensus is +37k). A lift in participation to 66.4% should temper the fall in the unemployment rateto around 0.1ppt (Westpac f/c: 4.1%), with risks favouring a smaller rise in participation and a larger fall in unemployment. The Q3 delta hit could see the population estimate dip into contraction on an annual basis. The March RBA Bulletinwill provide insights into the Australia’s economy and financial system.

NZ: Westpac anticipates a 3.8% rise in GDP for Q4, almost fully reversing the Q3 delta-dip; the recovery in production should be a key source of strength, while services spending remained subdued with lingering restrictions over the quarter.

Japan: Weakness in machinery ordersis anticipated for January as the omicron outbreak restrains capital investment (market f/c: -2.0%).

Eur/UK: The final estimate for the Eurozone’s February CPIwill highlight the ongoing concerns with energy inflation (market f/c: 0.9%mth; 5.8%yr). Meanwhile, the Bank of Englandis expected to lift the bank rate by another 25 basis points to 0.75%; Russia-Ukraine uncertainties may cloud the path for tightening beyond March.

US: Robust underlying demand for housing should continue to buoy housing startsand building permits in February, although sourcing labour and high material costs are headwinds (market f/c: 3.8% and -2.4% respectively). Initial jobless claims are set to remain at a low level (market f/c: 220k), and the March Phily Fed indexwill offer a gauge of business activity in the region (market f/c: 15). Volatility in industrial productionwill linger in February as firms navigate supply issues (market f/c: 0.5%).

China’s amusing attempt to talk markets higher may have legs for a bit. Ukraine war newsflow may help as well. But do not be fooled. These are peripheral issues. The main game is now afoot. The Federal Reserve is about to crash the global economy:

Indicators of economic activity and employment have continued to strengthen. Job gains have been strong in recent months, and the unemployment rate has declined substantially. Inflation remains elevated, reflecting supply and demand imbalances related to the pandemic, higher energy prices, and broader price pressures.

The invasion of Ukraine by Russia is causing tremendous human and economic hardship. The implications for the U.S. economy are highly uncertain, but in the near term the invasion and related events are likely to create additional upward pressure on inflation and weigh on economic activity.

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. With appropriate firming in the stance of monetary policy, the Committee expects inflation to return to its 2 percent objective and the labor market to remain strong. In support of these goals, the Committee decided to raise the target range for the federal funds rate to 1/4 to 1/2 percent and anticipates that ongoing increases in the target range will be appropriate. In addition, the Committee expects to begin reducing its holdings of Treasury securities and agency debt and agency mortgage-backed securities at a coming meeting.

In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee’s goals. The Committee’s assessments will take into account a wide range of information, including readings on public health, labor market conditions, inflation pressures and inflation expectations, and financial and international developments.

It is now my base case that the global economy is late-cycle in 2022. Not 2023 nor 2024. Recella that this cycle is on speed:

US yields are already choking off the housing market and the giant post-COVID inventory pile is quivering as oil shocks households.

China is worse. Domestic demand is falling away chasing the property adjustment. OMICRON cannot be beaten without constant lockdowns and material damage to output. An external demand shock looms. It is terrified to cut rates lest CNY crashes. It will have no choice.

Europe is stuffed by an energy shock and war.

EMs are crushed by a tightening Fed and a loosening China.

Yet the Fed is cornered by runaway inflation and will tighten aggressively into all of the above. Jay Powell was unequivocal in the presser. Rates are going to rise every meeting until he aligns demand with supply and given the latter is falling then the former must too.

An end-of-cycle shock is now the base case and, yes, it will also hammer Australia in due course as asset price falls merge with a commodity price crash.

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed. Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website. Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.