DXY eased last night:

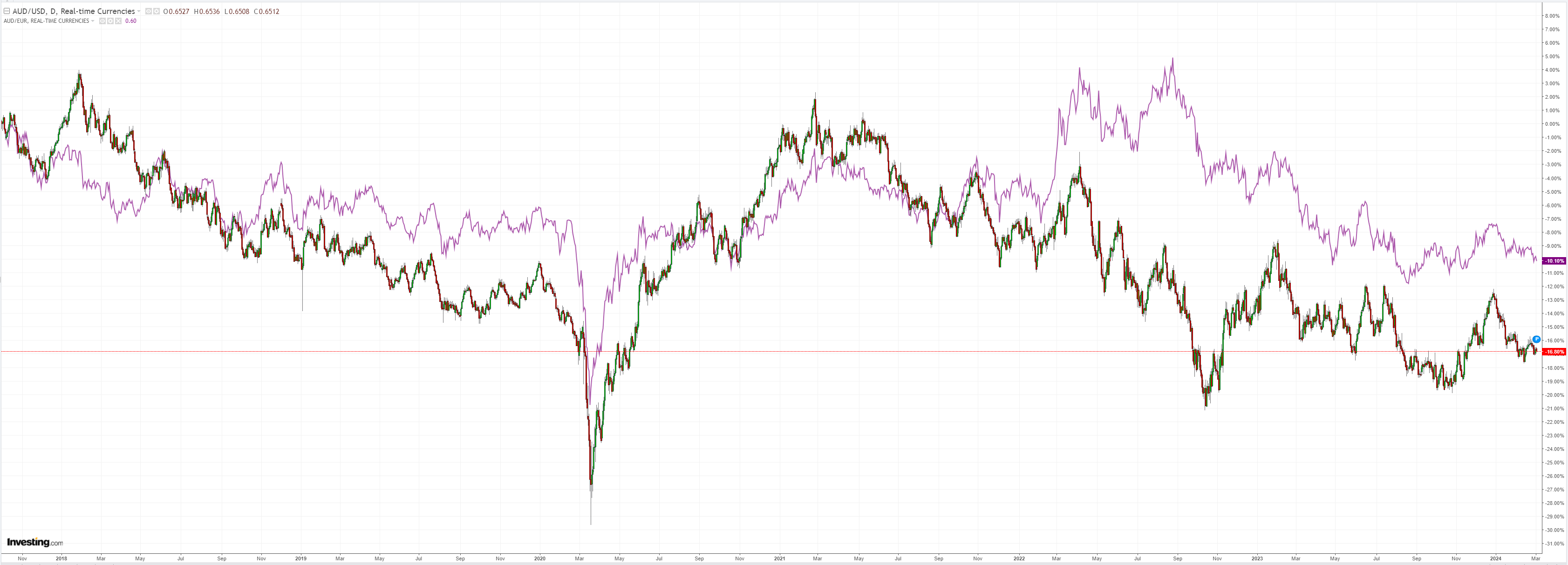

AUD is weak:

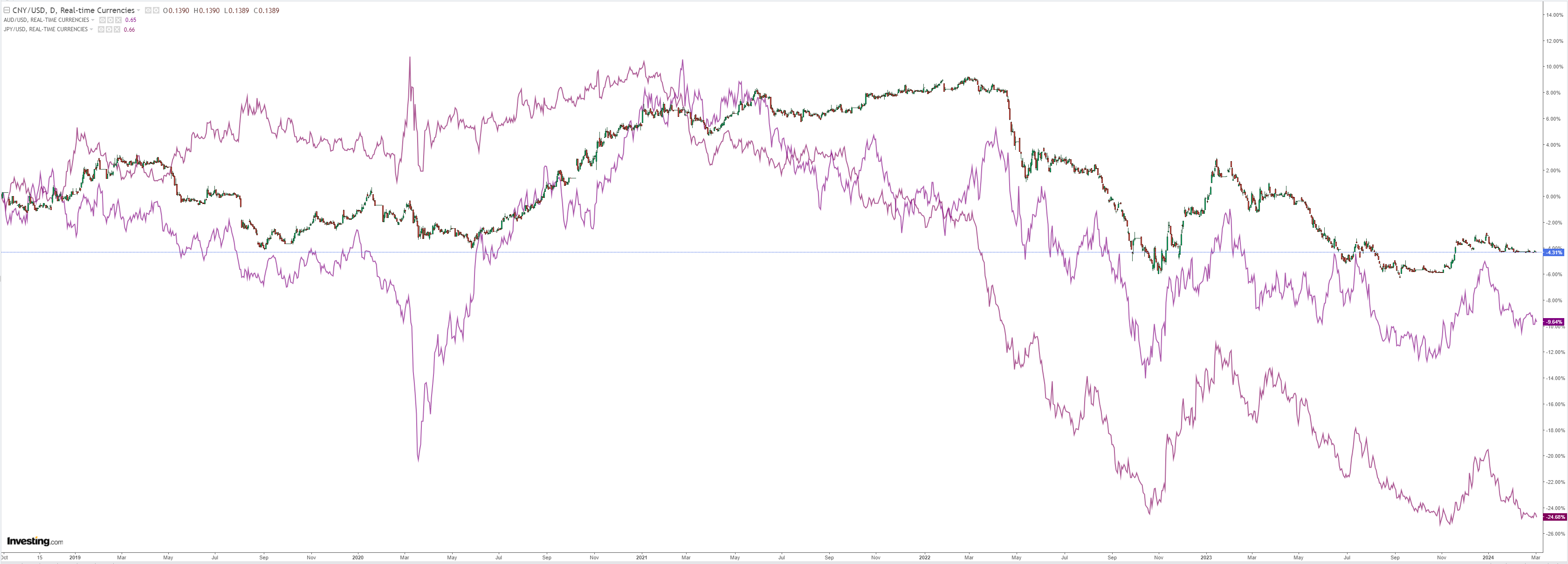

CNY is in stasis forever now. What a global reserve it’s going make!

Oil fell, and gold ramped:

Base metals yawn:

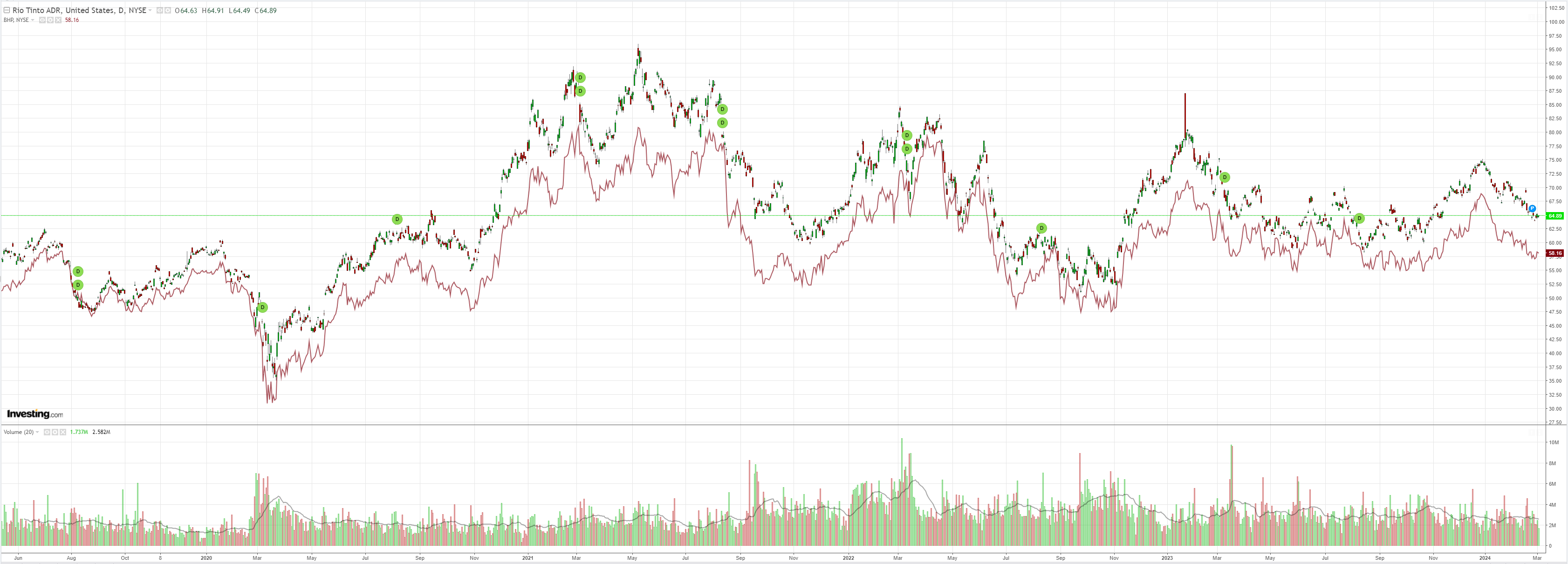

Miners yawn:

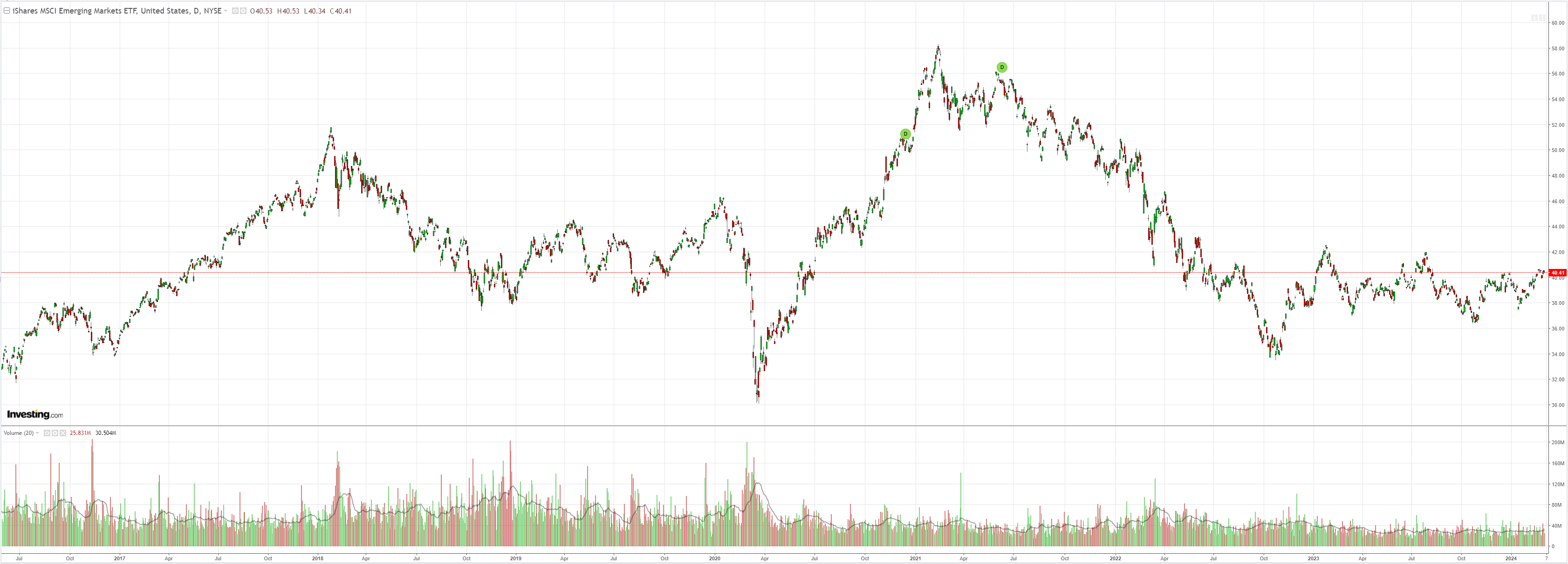

EM yawn:

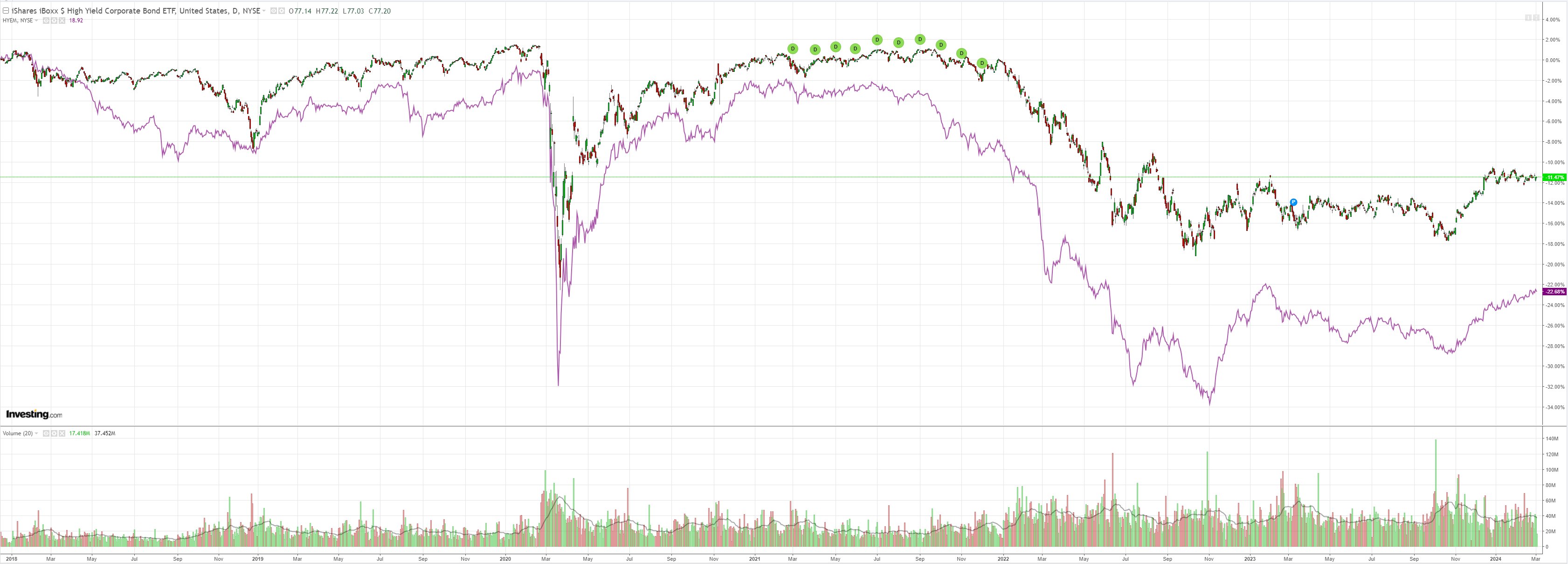

EM junk is still leading risk on:

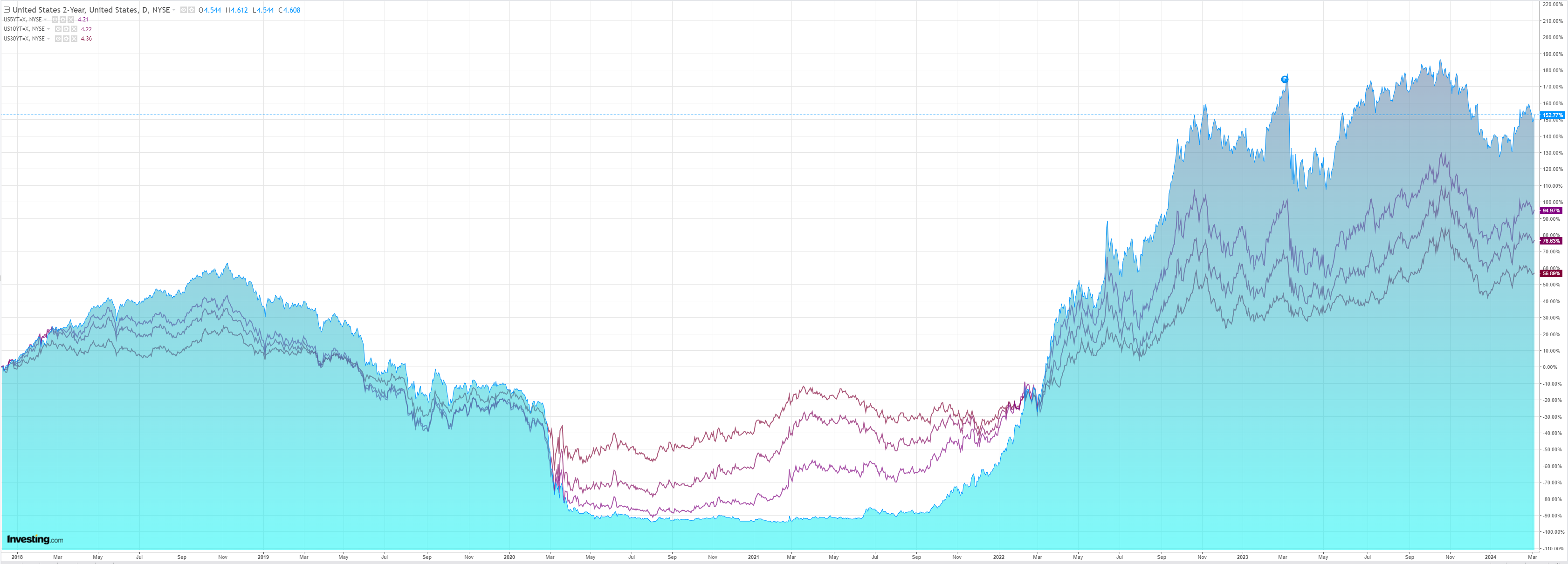

Treasuries sold:

Stocks meh:

As we head deeper into the year, it’s time we consider the implications for the AUD of the US election.

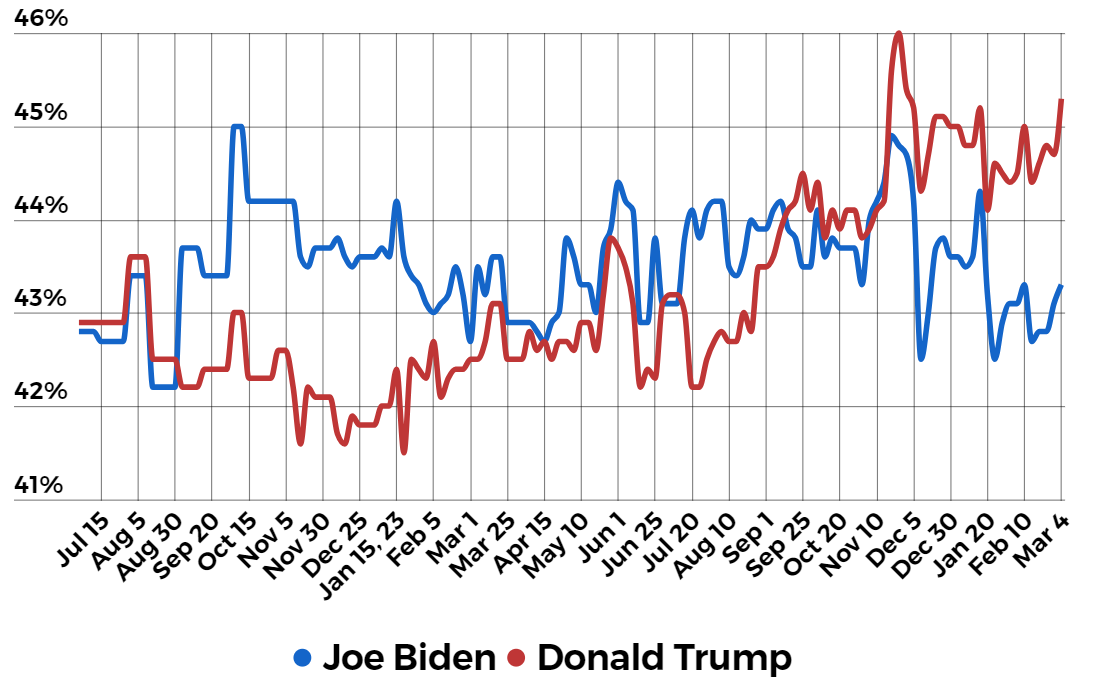

Polling has Donald Trump favourite:

At this stage I would take that with grain of salt. But after last week’s Supreme Court decision to hear the immunity case, the odds are firming that Trump will at least make it to polling day.

While that possibility firms, market will have discount his policies, which are very DXY bullish and AUD bearish.

Most notably, a 60% Chinese tariff and border closure of some type with Mexico.

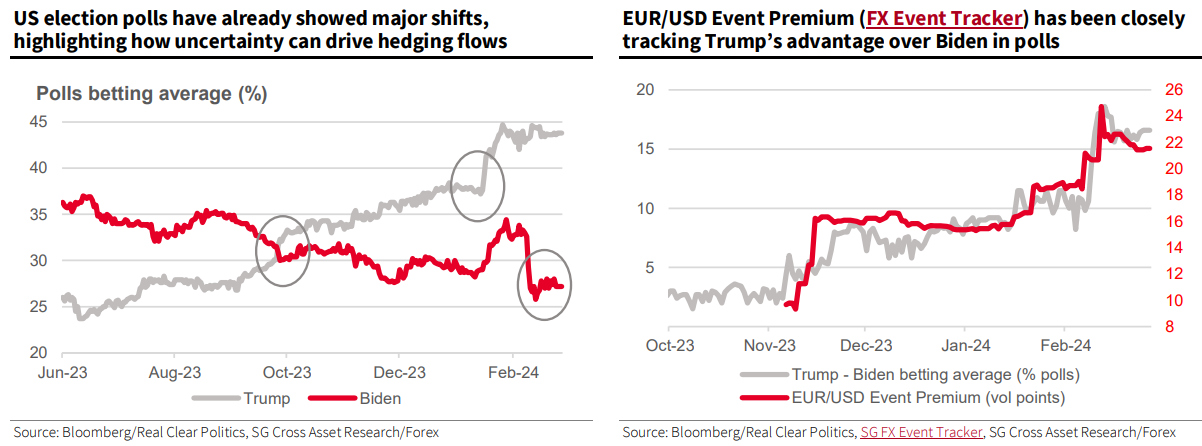

More from Societe Generale (EPA:SOGN):

The EUR/USD option market started to position on the US election one year ahead, and the event premium inferred by our Event Tracker is now closely tracking Trump’s advantage over Biden in polls.

The market is currently expecting EUR/USD vol to be almost four times higher than usual on the day after the election.

The EUR/USD election premium is already higher than in 2020 at the same time ahead of the election day. 2024 has been following a similar rising path to that in 2020, and if the current trend continues in the same way as in 2020, this would suggest a rise in the premium of about 10 vols this spring.

In five of the six previous elections, EUR/USD implied vol declined over the two weeks following election day.

During the quarter following the election, it tended to rise with a Democratic president and to fall with a Republican president.

While the very liquid EUR/USD options provide the most reliable market information, the highest election premiums are found in USD/MXN and GBP/USD in EM and G10 markets.

The markets’ perception of the gap between the two main candidates captures the risk surrounding the election. It turns out that the ‘Trump-Biden’ spread is proving a significant metric, as our EUR/USD election premium has been closely tracking Trump’s advantage over Biden in polls. A rise in this premium is associated with higher volatility just after the election, confirming that the market is seeing a Trump victory as a risk-adverse event.

Trump’s tax cuts set in 2017 will expire in 2025 and even if their extension would be pro-growth, tariffs and geopolitical considerations are potentially major concerns. These issues were already there in 2016, but the economic and geopolitical backdrop looks tricker in 2024, with meanwhile the return of inflation and persisting military conflicts.

There are many uncertainties at this juncture. The court cases against Trump and Biden’s brain are just two. So, I don’t expect DXY to go tearing away.

As well, we still have Fed easing ahead, and a bounce in global industrial production coming, both of which will weigh against DXY.

But the election is already DXY bullish at the margin, and any firming in the odds of a return to Trump will push that further, faster.

Trump’s platform will do material harm to China and is equally inflationary for the US.

He is an outright AUD destroyer.