DXY is up and away again:

AUD fell:

With Oil:

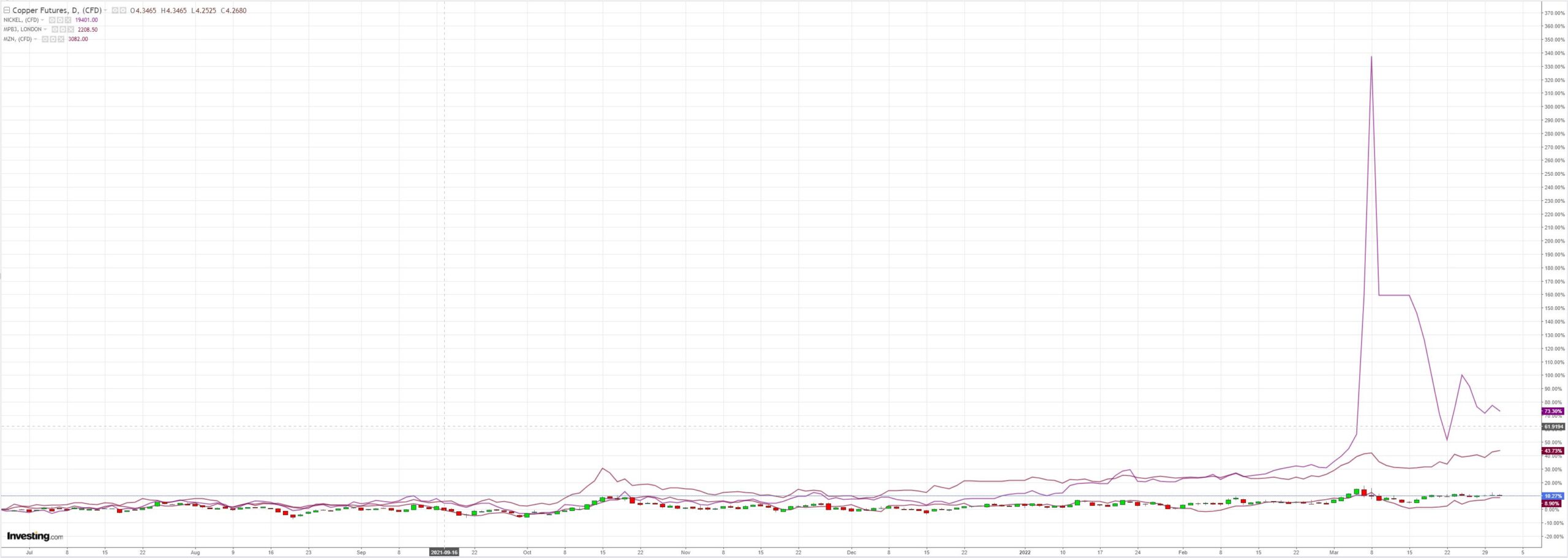

Metals were OK:

Miners (LON:GLEN) too:

EM stocks (NYSE:EEM) gave up:

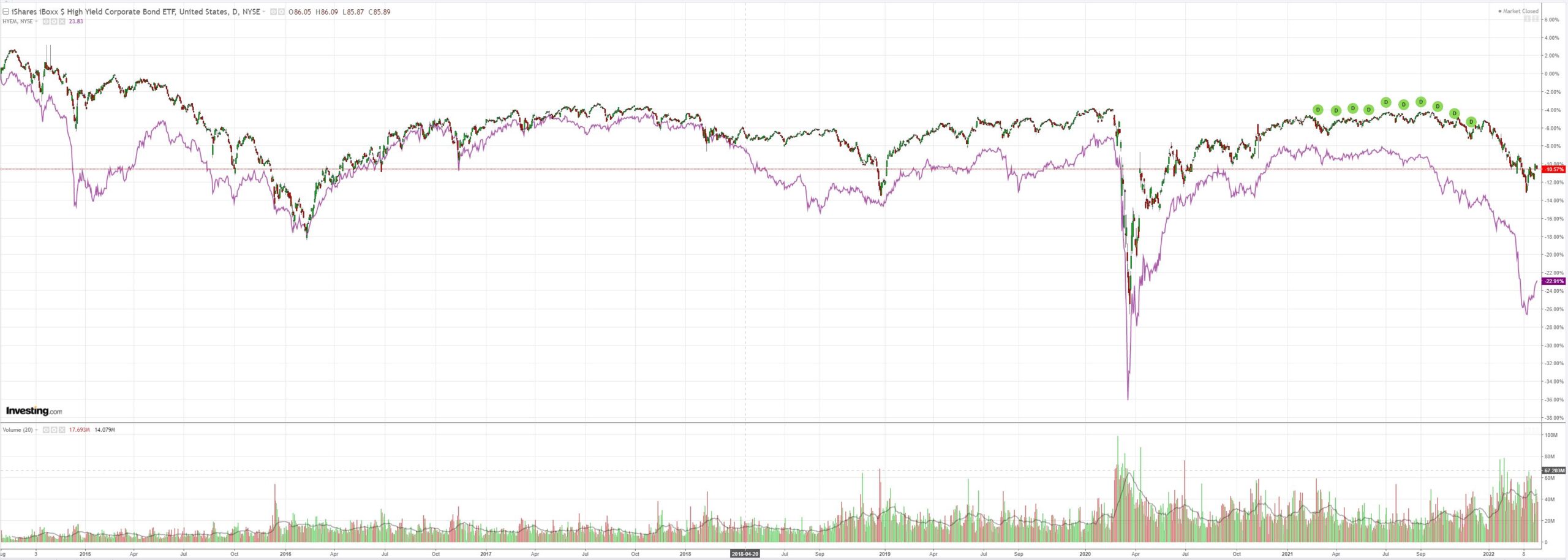

Junk (NYSE:HYG) was mixed:

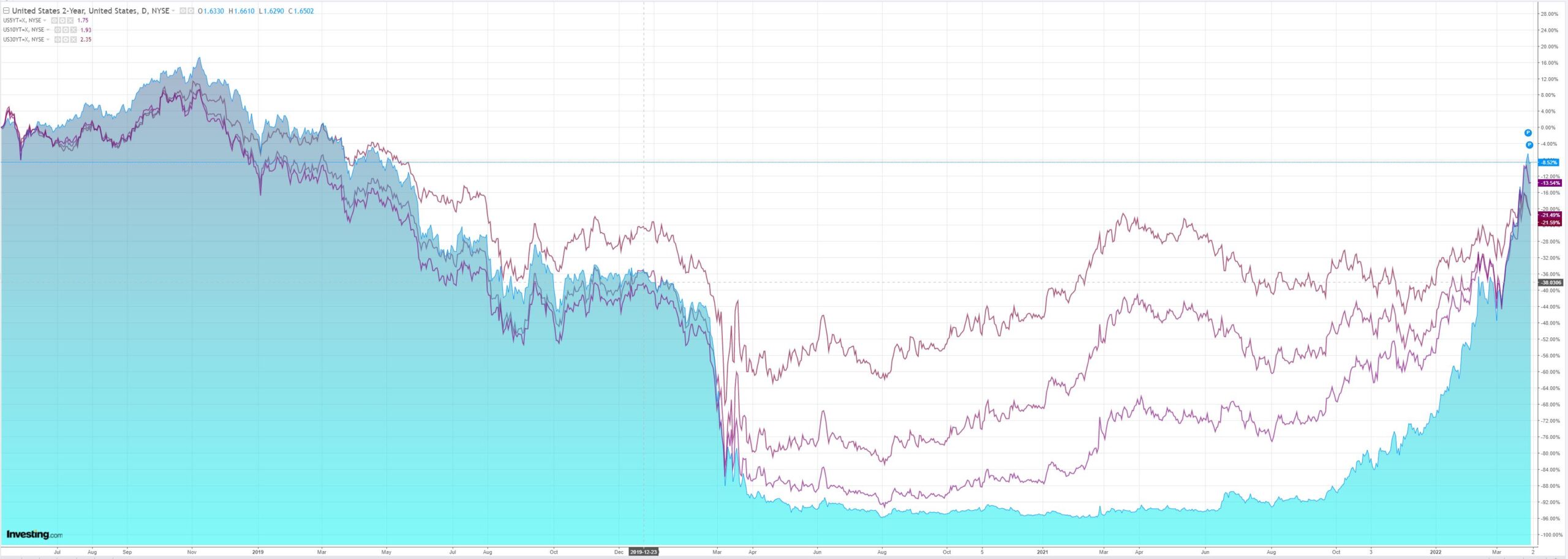

The Treasury curve flattened again:

Stocks rolled:

Westpac has the wrap:

Event Wrap

US personal Income and spending in Feb. rose 0.5%m/m (matching expectations) and 0.2%m/m (est. +0.5%m/m). The PCE deflator rose 6.4%y/y (prior 6.0%y/y), with core slightly below expectations at 5.4%y/y (est. 5.5%y/y, prior 5.2%y/y). Weekly initial jobless claims edged up to 202k (est. 196k, prior 199k), with continuing claims at 1.307m (est. 1.340m, prior 1.342m). Chicago PMI surprised with a rise to 62.9 (est. 57.0, prior 56.3). Production improved to 60.0 – below the 12-month average of 62.8, but up from 55.4. Employment rose to 48.1 from 43.5. New orders rose to 61.9 from 53.0.

Eurozone unemployment rate in Feb. was at 6.8% (est. 6.7%, prior revised to 6.9% from 6.8%). Germany’s unemployment rate was unchanged at 5.0% as expected. French CPI in Mar. showed a smaller rise than yesterday’s releases of Spanish and German CPI. Headline CPI rose +1.4%m/m (est. 1.3%m/m) and 4.5%y/y (est. 4.3%y/y), with harmonised CPI at 5.1%y/y (est. 4.9%y/y).

UK Q4 GDP was finalised higher at 1.3%q/q, from 1.0%q/q, for an annual rise of 6.6%y/y (initially 6.5%). Net exports improved but the consumption components were generally softer than expected. .

Event Outlook

Aust: A soft gain in CoreLogic’s home value index is anticipated for March given the signs of slowing in Sydney and Melbourne (Westpac f/c: 0.3%). The total value of housing finance should post a solid lift in February as approvals continue to catch-up to the strength in turnover levels (Westpac f/c: 2.5%); investor loans are expected to outperform owner-occupier loans (Westpac f/c: 5.5% and 1.1% respectively).

NZ: ANZ consumer confidence is set to remain weak in March given ongoing COVID-19 and inflation concerns.

Japan: Elevated commodity prices and ongoing supply issues are expected to dampen sentiment in the Q1 Tankan large manufacturers index (market f/c: 12). The final estimate for the March Nikkei manufacturing PMI is also due.

China: COVID-19 disruptions will likely weigh on manufacturing growth in the March Caixin PMI but authorities’ support will aid the sector in working through these issues (market f/c: 49.9).

Eur/UK: Energy inflation is expected to make another strong contribution to European consumer inflation in March (market f/c: 6.7%yr). The final estimate for the March Markit manufacturing PMI is due for the Eurozone and UK.

US: Non-farm payrolls are expected to continue reflecting healthy gains in employment growth in March (Westpac f/c: 500k, market f/c: 490k) pushing the unemployment rate lower (Westpac f/c: 3.9%). The historically tight labour market should continue to support average hourly earnings (Westpac f/c: 0.3%). Meanwhile, the March ISM and Markit manufacturing PMIs should highlight the robust growth of the sector (market f/c: 59 and 58.5 respectively). The strength in homebuilding should continue to buoy construction spending in February (market f/c: 1.0%). The FOMC’s Evans will speak on the economy and monetary policy.

Credit Agricole (PA:CAGR) with a snippet:

Following weeks of accentuated gains vs low-yielders like the EUR and JPY in recent weeks, the USD has been largely struggling in recent days. We think that this reflects a combination of fundamental and FX market-specific drivers. Starting with the former, we note that the recent aggressive flattening of the UST yield curve has been seen by some of our clients as heralding the beginning of the end of the recent USD rally that has been in place since early 2021. Indeed, recent history would suggest that periods of very flat and especially inverted UST yield curve (using UST2-10Y) saw the USD trading in a range to somewhat weaker across the board. Turning to the second USD driver, the latest price action reflects the impact of Month-end rebalancing flows – which, according to our analysis, should result in net USD-selling. In addition, we think that profit taking on stretched USD longs – most notably in the case of USD/JPY in the G10 space – are contributing to the latest underperformance. Worth highlighting in that the results from our FX positioning analysis that suggests that, in addition to the JPY, the GBP is also looking quite oversold. On the day, focus will be on the US Core PCE data for February, the Chicago PMI for March and a speech by the Fed’s John Williams. While both the data releases and Fed speak should confirm the already hawkish market expectations, we doubt that this will be enough to give the overbought USD a meaningful boost.

My own view is another leg-up in DXY is coming as markets awake to the looming global recession and stocks then commodities crack lower.

The Fed is unequivocal. It is going to squash demand to fit with constrained supply.

That means one more sharp leg lower for AUD.