- PayPal stock came under short-term pressure following its Q2 results.

- However, PayPal revenues are expected to grow by 20% this year.

- Long-term growth drivers in the digital payments and crypto space should provide tailwinds for PYPL stock.

Shares of the leading financial technology heavyweight PayPal (NASDAQ:PYPL) have plunged following the release of second-quarter results on July 28. After hitting a record high of $310.16 on July 26, PYPL stock is currently hovering around $275, down more than 10% off its peak last week.

Despite the recent decline in price, we remain bullish on PYPL stock for the long run. Today, we discuss how investors might consider incorporating the shares into their portfolios.

Long-Term Tailwinds For PYPL Stock

California-based PayPal provides digital payment solutions to merchants and consumers. Its offerings include PayPal, PayPal Credit, Braintree, person-to-person payment platform Venmo, international money transfer business Xoom, iZettle, Hyperwallet, and the recently acquired Chargehound and Happy Returns.

Founded in 1998, PayPal has become a dominant player in the digital payment sector. After having spun off from eBay (NASDAQ:EBAY) in 2015, PYPL pursued an aggressive growth strategy and innovative approach.

Recent metrics highlight:

"The transaction value for the Global Digital Payments Market was $5.44 trillion in 2020, and it is projected to be worth $11.29 trillion by 2026, registering a CAGR of 11.21% during the period of 2021-2026.”

As of May 2021, PayPal had more than 400 million active customer and merchant accounts worldwide. This means the company’s growing network of consumers and merchants is one of the most important catalysts for revenue growth in future quarters.

According to Emergen Research, of all the leading digital payment companies, PayPal is number three by revenue. Its Q2 financial results showed that the top inched up 17% year-over-year (YOY) to $6.24 billion. Non-GAAP net income was $1.36 billion in the second quarter of this year, representing 8% YOY growth as compared with Q2 2020. Management expects top-line and non-GAAP bottom-line growth for the fiscal year to be 20% and 21%, respectively.

Therefore, PayPal’s current market capitalization of $319.5 billion will potentially grow in future quarters as well.

On a side note, readers might be interested to know that among PayPal’s main competitors are JPMorgan Chase (NYSE:JPM), Visa (NYSE:V), Mastercard (NYSE:MA) and Fiserv (NASDAQ:FISV).

On the Q2 results, PayPal CEO Dan Schulman said:

“On the heels of a record year, we continued to drive strong results in the second quarter, reflecting some of the best performance in our history… Clearly PayPal has evolved into an essential service in the emerging digital economy.”

However, he also noted that eBay Marketplaces stopped being served by PayPal, and the metrics reflected this development.

Since October 2020, PayPal has also integrated cryptocurrency into its digital transactions, enabling U.S.-based users to buy, sell and hold Bitcoin, Ethereum, Bitcoin Cash and Litecoin. In Q2, the Venmo platform saw robust crypto trading.

Investor interest in digital currencies is growing worldwide. Earlier in 2021, “The average daily cryptocurrency trade volume has risen dramatically to $109 billion per day.” As one of the first digital platforms to enable crypto transactions, PayPal will continue to benefit from the growth in crypto transactions.

In late July, rumors that Amazon (NASDAQ:AMZN) might be moving into the crypto space brought cheers to investors in Bitcoin as well as many altcoins. The surge in prices came as the market noted a job posting by Amazon that hinted the potential move by the tech giant. Such short-term swings in digital coins are commonplace. But they also show how much the market is interested in these developments.

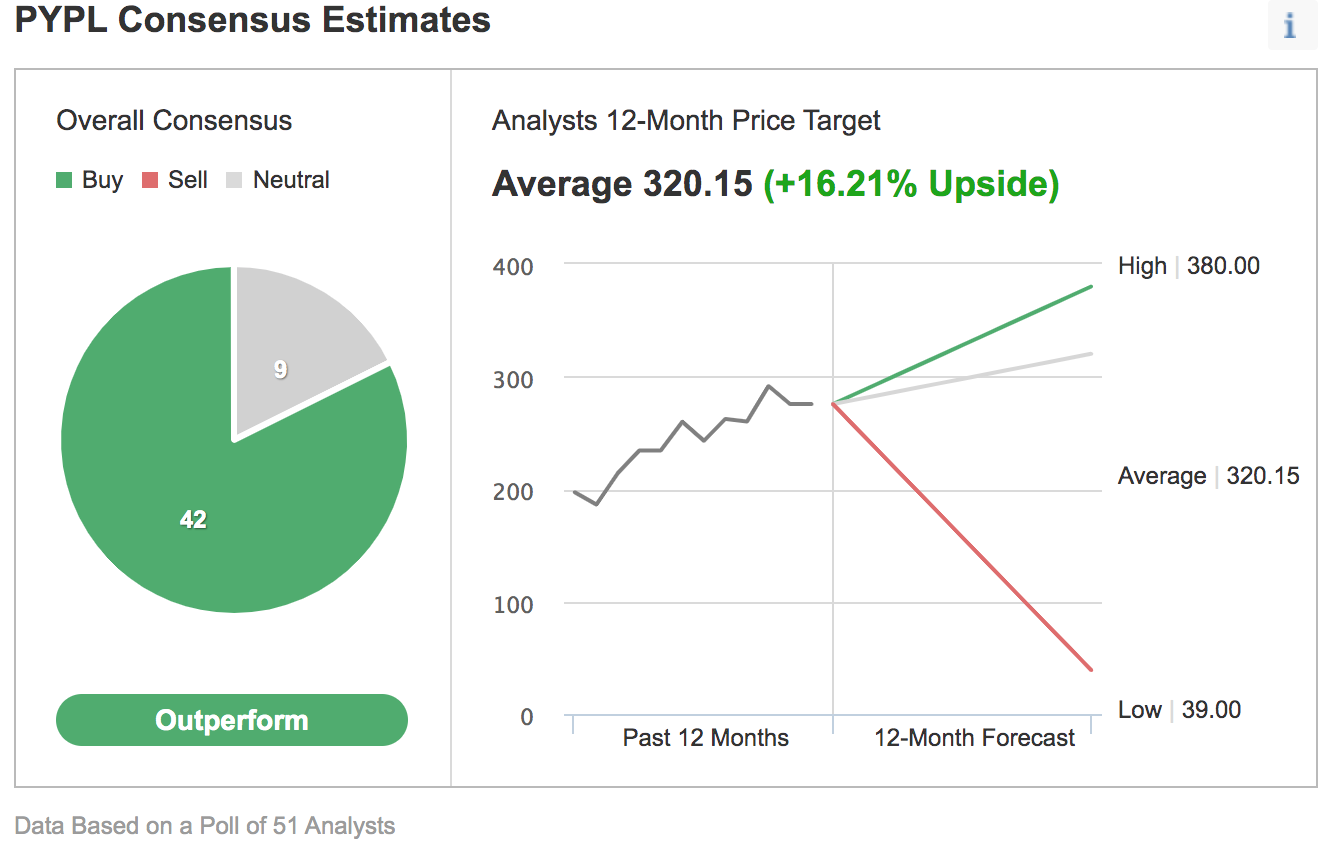

Among 51 analysts polled via Investing.com, PYPL stock is projected to outperform. The 12-month median price target of $320.15 would represent a return of more than 17% from the current level.

Short-Term Price Volatility In PYPL Stock Could Be Ending

Despite the bullish outlook for the coming months, many investors wonder whether now would be an opportune time to enter PYPL stock. We believe the recent decline in price is likely to end soon. Therefore, investors could begin to find value around the current levels.

As we’ve already noted, since the release of Q2 earnings, PayPal shares have lost about 10% of their value, providing a better entry point for buy-and-hold investors. However, there could still be a further pullback toward the $270 level, or even below.

Technical charts show short-term momentum indicators are oversold. Although they could stay oversold for a long time, more than likely PYPL stock will trade sideways in the coming weeks—especially between $260 and $280—until it builds a base around those levels.

At that point, we could possibly expect a new bull leg to start that could take PYPL stock to new highs The long-term technical trend is still up, pointing to a buy.

As part of the short-term sentiment analysis, it would be important to look at the implied volatility levels for PayPal options, which typically shows traders the market's opinion of potential moves in a security. However, it does not forecast the direction of the move.

PYPL’s current implied volatility (IV) is 26.7, which is lower than the 20-day moving average of 31.1. In other words, implied volatility is trending lower. Although the current IV level could change, for now expect the choppiness in PYPL stock to decline.

3 Possible Trades

1. Buy PYPL Stock At Current Levels

Investors who are not concerned with daily moves in price could consider investing in PYPL stock now.

On Aug. 4, as we write, PYPL stock is $272.74.

Such buy-and-hold investors should expect to hold this long position for several months while the stock potentially makes an attempt at the record high of $310.16.

Assuming an investor enters this trade at the current price and exits around $310, the return would be slightly more than 13%.

Investors might also consider placing a stop loss at about 3-5% below their entry point.

2. Protective Put Purchase

Readers who are bullish on PayPal stock, but remain nervous about a further short-term decline, might consider buying a protective put in addition to their stock holdings.

For instance, the trader might buy an out-of-the-money (OTM) put option, like the PYPL Oct.15 250-strike put option.

This option is currently offered at $5.60. Thus, it would cost the trader $560 to own this put option, which expires in slightly over two months (i.e., the maximum risk for the trade). But by buying this option, PayPal investors who also hold the stock would have some protection, especially if the shares or the broader tech sector came under pressure.

This trade would break even at $244.40 on the day of the expiry (excluding brokerage commissions).

3. Buy An ETF That Has PayPal As A Top Holding

Many readers of this column would be familiar with the fact that we regularly cover exchange-traded funds (ETFs) that could be suitable for buy-and-hold investors. Thus, readers who do not want to commit capital to PYPL stock, but would still like to have sizeable exposure to the shares, could consider buying a fund that holds the company as a leading name.

Examples of these ETFs include:

- iShares U.S. Industrials ETF (NYSE:IYJ): the fund is up 15.1% YTD, and PYPL stocks weighting is 6.3% in the ETF;

- ETFMG Prime Mobile Payments ETF (NYSE:IPAY): the fund is up 3.8% YTD, and PYPL stocks weighting is 6.2% in the ETF;

- First Trust Dow Jones Internet Index Fund (NYSE:FDN): the fund is up 14.2% YTD, and PYPL stocks weighting is 5.3% in the ETF.

Bottom Line

PayPal has become one of the most important fintech names, especially in the digital payments space. Its crypto transactions are also growing. Therefore, PYPL shares are likely to offer sizeable gains in the years ahead. Buy-and-hold investors could research the company further with a view to buying the dips.