Stocks soared, especially tech. ARK as a safe haven!

The weekend threw up another Ukraine shocker:

In coordination with [U.S, France, Germany, Italy, Canada and U.K] I will now propose new measures to EU leaders to strengthen our response to Russia’s invasion of Ukraine and cripple Putin’s ability to finance his war machine. https://t.co/iU2waDzo9s

— Ursula von der Leyen (@vonderleyen) February 26, 2022

Then there is this:

UPDATED 3: The White House, in call with reporters tonight, made very clear that it’s actively making sure that the SWIFT move against Russia does NOT impact energy payments, using two potential paths | #OOTT #ONGT #Ukraine

The below is from Biden administration senior official pic.twitter.com/W6n2bkGKgH

— Javier Blas (@JavierBlas) February 26, 2022

Well, there you go. Russia has assured Europe of its economic destruction via energy prices and Europe has responded by assuring Russia of its economic destruction by being booted out of the US dollar monetary system.

Russia has now responded by elevating its nuclear threat readiness.

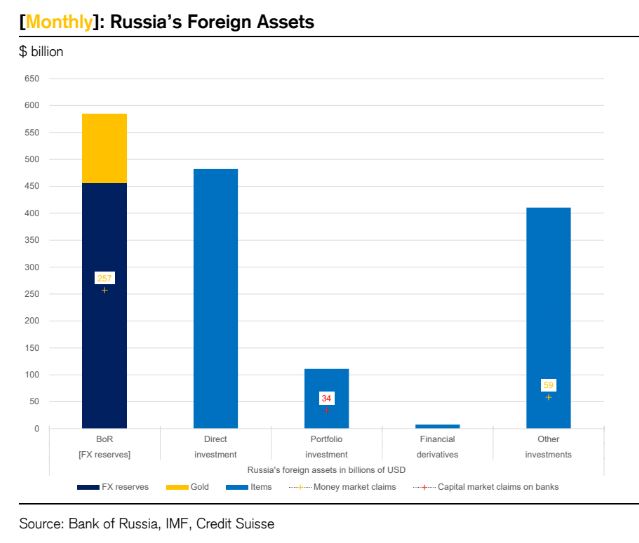

On Monday morning Russia effectively wakes up insolvent. Credit Suisse (SIX:CSGN) has previously had a crack at what it means if Russia is forced to try to liquidate its reserves:

Other than the roughly $200 billion in FX swaps, the Bank of Russia and the private sector have claims on foreign banks in the form of deposits in the amount of about $50 billion each–most likely a mix of euro-and U.S. dollar-denominated deposits, which is how we arrived at the $300 billion total above.

$300 billion deployed in the money markets is a lot.

$300 billion is enough to push spreads around in funding markets.

$300 billion–in the extreme–can either be potentially trapped by sanctions, or moved somehow from West to East to avoid being trapped by sanctions.

Each would be a market event.

Consider for example if funds get frozen through sanctions–an event that would turn a surplus agent into a deficit agent, which in turn would lead to missed payments, much like the onset of Covid-19 led to missed payments and turned surplus agents into deficit agents. Some version of such flows are something the market should discount. Alternatively, consider the notion that…

…if you owe the bank $1 million, that’s your problem, but if you owe the bank$1 billion, that’s the bank’s problem.

Surplus agents can move their surplus funds from Western financial centers and institutions to financial centers, financial institutions, and central banks elsewhere that would then re-cycle surpluses back into the financial system.

However, that would mean the partial “tear-up” of matched FX swap books and outflows of operating deposits (as public and private surpluses are moved, respectively) from Western banks. But that would be their funding problem–as deficit agents, these institutions may then have to tap the dollar swap lines.

When flows change, spreads can gap.

We are no experts on geopolitics, neither do we know which way events will unfold either on the ground or in the domain of sanctions. But if things escalate, it’s hard not to see a direct impact on FX swaps and U.S. dollar Libor fixings given Russia’s vast financial surpluses and where those surpluses are deployed.

Whoever moves first, there is a funding impact either way…

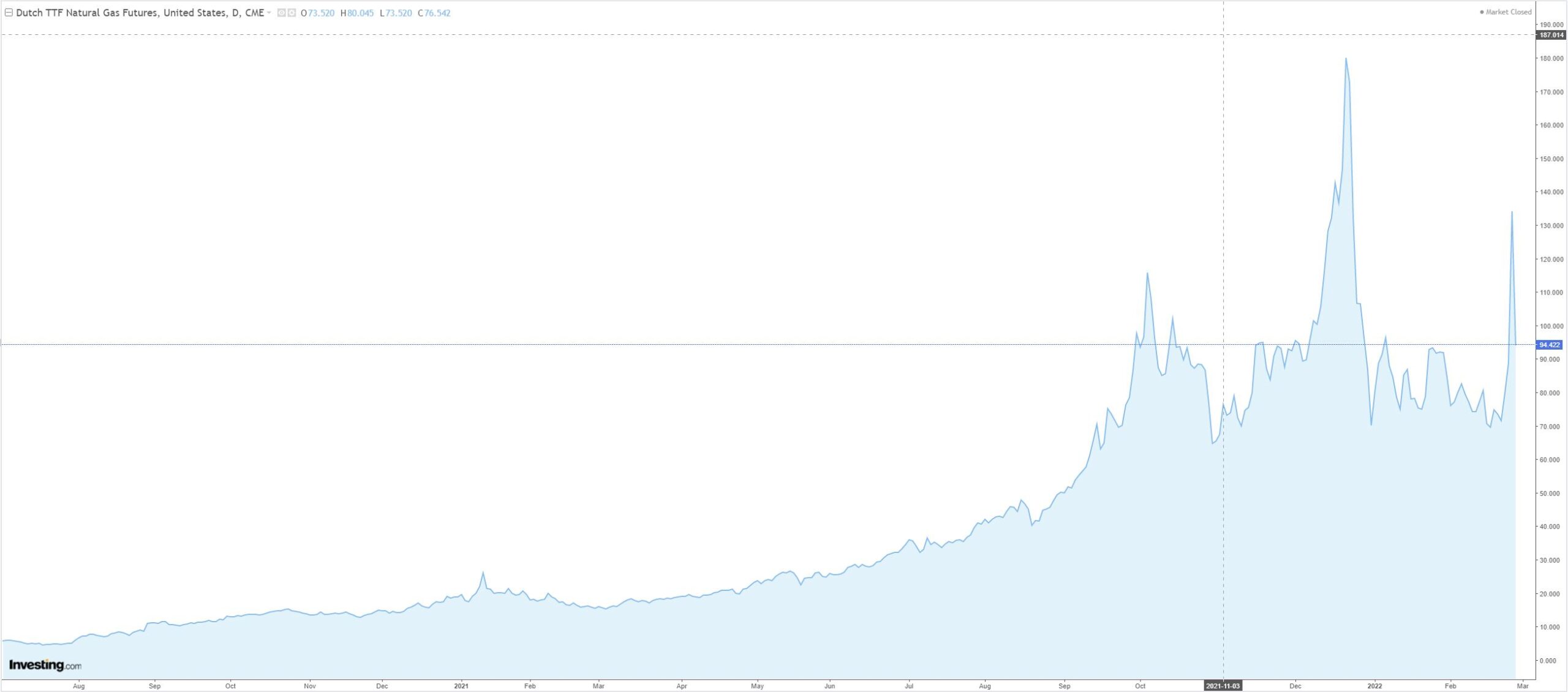

IFthe SWIFT changes are comprehensive enough then expect a global scramble for US dollars typical of an end-of-cycle shock, gold may get liquidated. Whether a genuine energy shock now develops is up in the air.

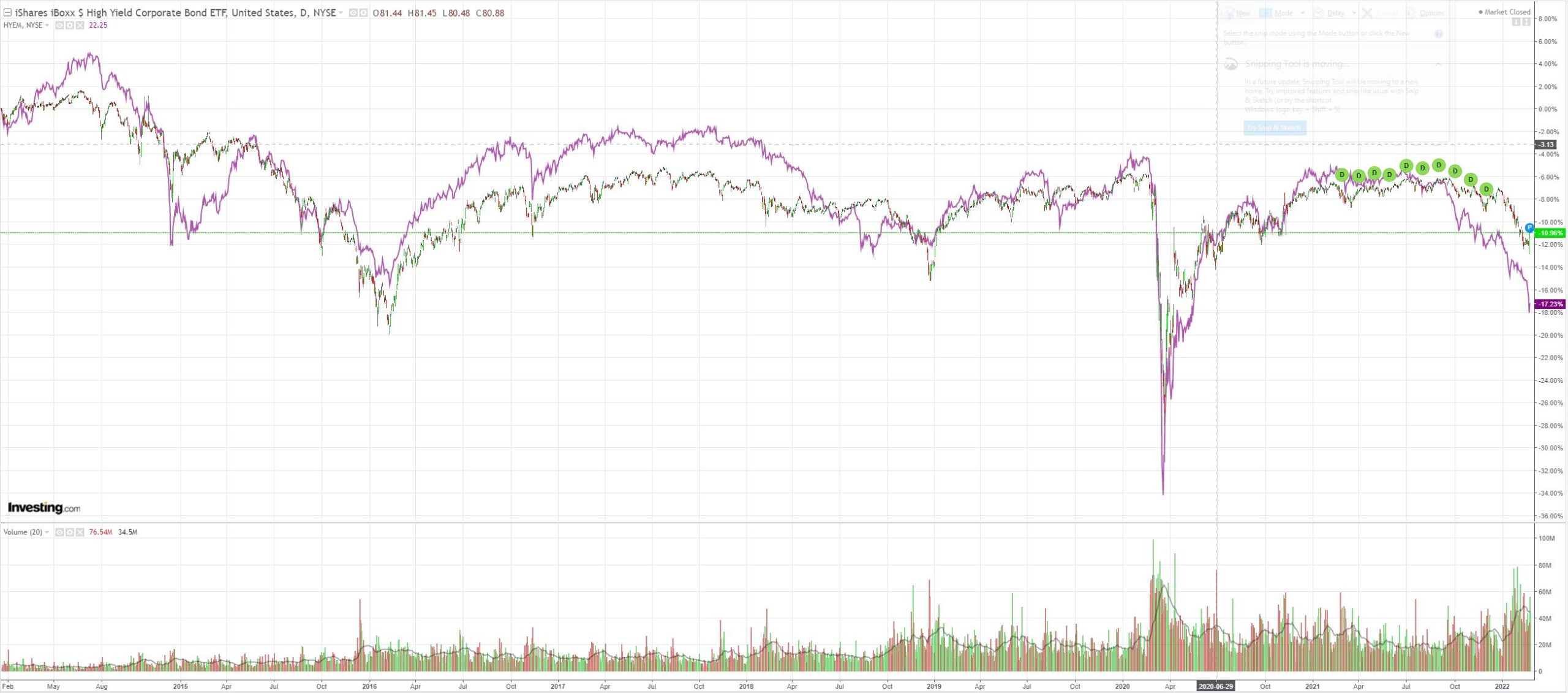

There is the distinct possibility of cascading credit events, exploding bank spreads on counterparty risk, and crashing stock markets.

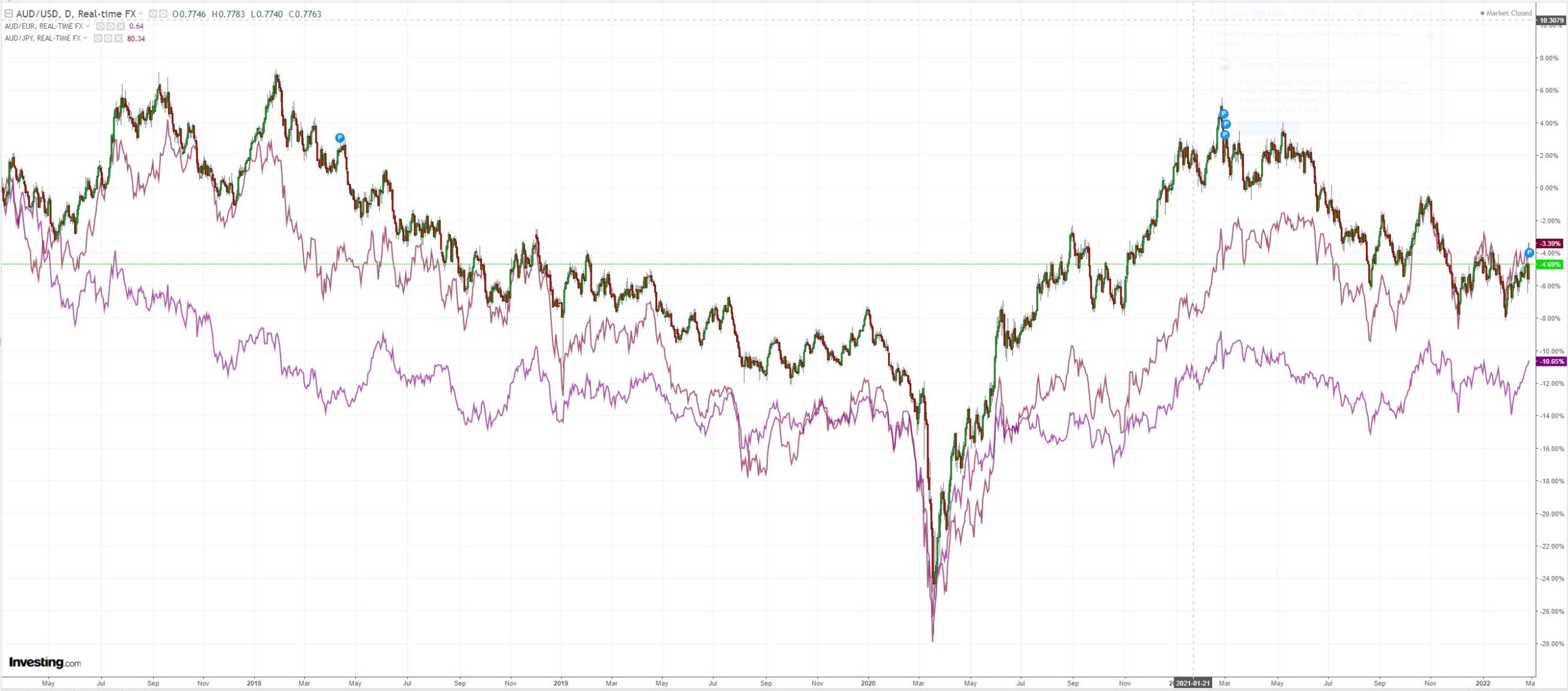

These are titanic forces pushing both up and down on the AUD but I’d expect down to win out so long as Russia is locked out SWIFT.

The mutually assured destruction of the world’s largest economy is not bullish.

Europe’s mutually assured destruction lands on Australian dollar

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed. Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website. Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.