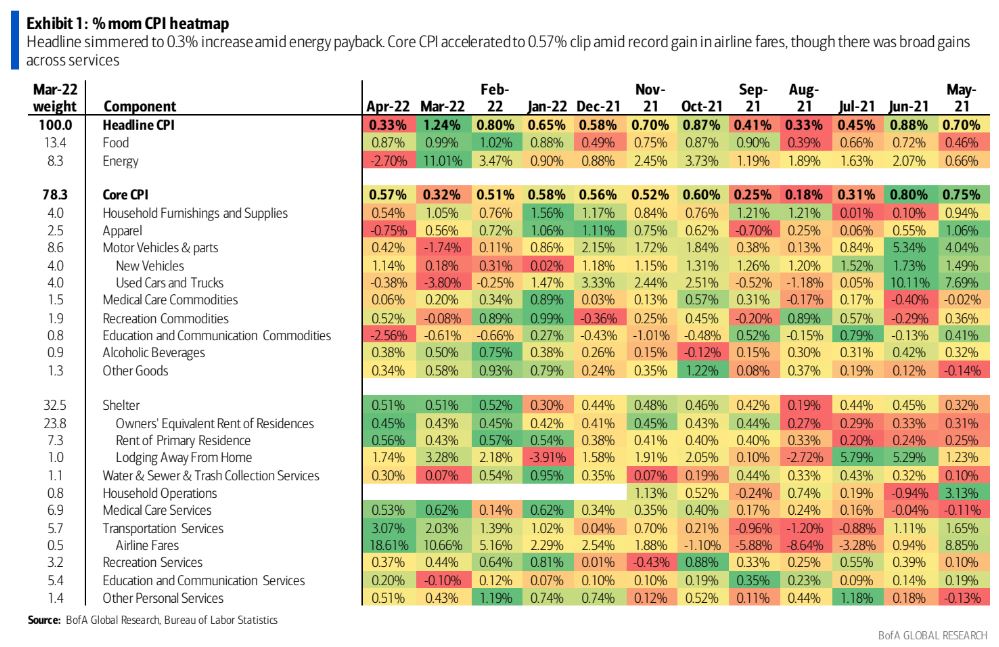

US CPI in April was stronger than expected, headline inflation at +0.3%m/m and +8.3%y/y (vs est. +0.2%m/m and 8.1%y/y, prior 8.5%y/y). Core inflation rose +0.6%m/m and +6.2%y/y (est. +0.4%m/m and 6.0%y/y, prior 6.5%y/y). While the pullback in annual inflation from last month suggests that a peak has been seen, the breadth of rising components raises concerns that inflation pressures will be slow to subside.

A flurry of ECB speakers all carried the same message: inflation pressures warrant the end of current accommodation. The ECB looks to end QE at its June meeting, when it has updated forecasts, and start raising rates early in Q3. Lagarde said that inflation was likely to be at (or above) target through their forecast period, strengthening the case for ending accommodative policy. All speakers (including Villeroy, Nagel, and Elderson) stressed that policy change would be gradual, measured and data dependent.

Event Outlook

Aust: MI inflation expectationswill likely remain elevated, mirroring the 5.1%yr lift in the Q1 CPI. The preliminary estimate for April’s overseas arrivals and departures will provide insight into whether the newly found momentum in overseas travel has sustained.

NZ: Higher mortgage rates are set to continue weighing on REINZ house sales and pricesin April. The minimum wage lift will likely see food pricesrise in April (Westpac f/c: 0.8%). Meanwhile, net migrationflows should remain subdued in March but it should strengthen over the coming months as travel restrictions continue to relax. The RBNZ’s inflation expectationsfor Q2 are set to rise sharply across near-term horizons following the strong Q1 inflation result.

Japan: The current account balanceis expected to remain in surplus in March on account of strong primary income and a smaller trader gap (market f/c: ¥1737.5bn).

UK: GDP growth is anticipated to reflect a decent recovery in Q1 although the Bank of England warns of a sharp slowing in activity over mid-year (market f/c: 1.0%). Below average trade volumes are likely to sustain the trade deficit in March (market f/c: -£7800mn).

US: Supply issues should continue to support producer prices in April (market f/c: 0.5%) and initial jobless claims are set to remain at a very low level (market f/c: 192k).

US inflation has peaked but remained stronger than expected. BofA:

Headline CPI prices simmered down to a 0.3% (0.33% unrounded) mom clip, though this was better than expectations for a 0.2% gain. Energy prices slid 2.7% mom as a pullback in retail gasoline prices led to a 5.4% drop in energy commodities, which was partially offset by a 1.3% increase in energy services. Food stayed hot as food at home climbed 1.0% mom and food away from home rose 0.6% mom. Coupled with negative base effects, yoy headline CPI slowed to 8.3% from 8.5% in March, with the latter month likely reflecting the peak in inflation.

Core CPI was an even stronger beat, rising 0.6% (0.57% unrounded) mom versus consensus at 0.4%. This led to the yoy rate dropping to 6.2% from 6.5%, reflecting the aforementioned unfavorable base effects. One of the main drivers of the upside surprise was a record 18.6% increase in airline fares, which added 13bp to core CPI alone and reflects a boost from reopening pressures. This contributed to a broader transportation services increase of 3.1% mom, with car truck rental and motor vehicle insurance prices also both rising 0.8% mom. Adding to the reopening theme, lodging gained 1.7% mom.

Even outside of the reopening-related categories, which we view as positive noise this month, there were notable broad based gains across services amid tight labor markets and accelerating wages. OER rose 0.45% mom and rent of primary residence accelerated to 0.56% mom. Medical care and other personal services both gained 0.5% mom, and recreation was up 0.4% mom. Water/sewer/trash and education/communication services both rebounded from negative readings in March to 0.3% mom and 0.2%, respectively.

Core goods was more mixed. On one hand, new cars rose 1.1%—a new methodology update likely contributed to a stronger reading this month, see That new car smell— household furnishings/supplies and recreation goods both rose 0.5%, alcohol was up 0.4% mom, other goods rose 0.3% mom, and medical goods edged up 0.1% mom. On the other hand, education/communication collapsed 2.6% mom, apparel slid 0.8% mom, and used cars fell 0.4% mom. There have been mixed signs of progress on supply chains in the US, which can help explain the more mixed readings across goods. Looking ahead, the Russia/Ukraine conflict and China lockdowns remains risks to commodity prices and global supply chain conditions, which could lead to further choppiness. On net, we expect fairly strong core goods inflation through this year, around 5% by yearend.

Overall, this was a noisy report given the move in airline fares, so some of the strength should be faded. That said, underlying inflation pressures remain elevated—we recommend keeping an eye out on trimmed-mean/median later this morning—which should leave the Fed comfortable maintaining their front-loaded rate hiking path. We still view the risks of a 75bp rate hike as low given the noise, but clearly this report adds to the debate on the margin.

The question is, will inflation come down fast enough to sink yields and lift stocks before the growth scare sinks stocks anyway.

At this stage, the answer looks like no. If so, AUD is still on a hiding to nothing.

Australian dollar sucked into American inflation black hole

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed. Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website. Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.