Headline CPI prices surged by 1.0% (0.97% unrounded) mom in May, beating consensus expectations of a 0.7% increase. Energy prices spiked 3.9% mom as gasoline prices reached record levels and food prices increases 1.2%. Yoy headline CPI inflation made anew 40-year high of 8.6%.The core CPI also beat expectations, rising 0.6% (0.63% unrounded) mom versus consensus at 0.5%. The yoy rate dropped from 6.2%to 6.0%, because of base effects. The strength in core inflation was across the board. Core commodities rose 0.7% on the back of 1.0% and 1.8% increases in new and used car prices, respectively. Along with the sharp drop in auto sales last month, this suggests that the auto industry was hit by a fresh bout of supply shortages last month. Meanwhile apparel prices increased 0.7% and other goods were up 0.8%. Core services were also very strong in May, increasing by 0.6%. The main drivers were 0.6% increases in OER and rental prices, and a 0.4% rise in medical care services. The reopening-related components showed continued large increases. Lodging was up 0.9% and recreation services increased 0.5%. Airfares spiked 12.6%, contributing nearly 11bpto the core. In the last three months alone, airfares have risen 48%. Some of this strength is likely to reverse in the coming months.

Stepping back, we are struck by the fact that there were almost no pockets of weakness in this report. The data are consistent with our view that inflation is no longer just a function of goods supply-chain disruptions. Inflation is also being driven by strong consumer demand because of a red hot labor market and strong wage inflation. Accordingly, inflation has become embedded in the more cyclical service sectors (e.g.,housing) as well. The Fed has telegraphed 50bp rate hikes in June and July. Its next decision point is in September. Although our base case remains a 25bp hike, today’s print increases the risk of another 50bp increase. The market is pricing a more aggressive Fed response on the back of today’s print. FOMC OIS now reflects 155 bps rate hikes through the September FOMC, assigning some probability to a 75bps hike in July.

There is only one trade in town now. Buy DXY. Even the perennially DXY bearish Goldman has capitulated:

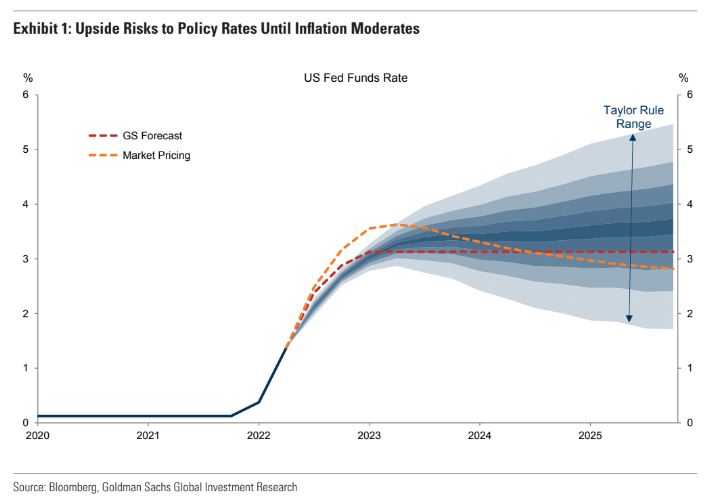

Friday’s data and subsequent price action were a microcosm of the broader market environment: inflation is far too high in major developed markets, and central banks need to tighten financial conditions to slow the economy down and lower inflation. Our modeling suggests the distribution of risks to policy rates in the US is still skewed to the upside over the medium-term, based on the range of possible outcomes for US inflation (Exhibit 1; we simulate inflation outcomes through a Taylor Rule, where the inflation distribution is calibrated to match the Philly Fed’s Survey of Professional Forecaster). At some point financial conditions will tighten enough and/or growth will weaken enough such that the Fed can pause from hiking. But we still seem far from that point, which suggests upside risks to bond yields, ongoing pressure on risky assets, and likely broad US Dollar strength for now.

It is increasingly likely that this cycle is going to end in a firey credit event mushroom cloud. Perhaps it will be macro-led. Candidates present themselves all over:

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed. Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website. Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.