Both Moderna and Pfizer (NYSE:PFE) commented on their positive outlooks for their vaccines, and treatments for Covid being adaptable to cope with Omicron.

US pending home sales in October rose by a surprising 7.5%m/m (est. +0.8%m/m), with gains across all regions, led by an11.8% gain in the Midwest. The Dallas Fed activity survey pulled back to 11.8 (est. 17.0), from prior 14.6. However, the headline belies a strong survey, with production rising to 27.4 from prior 18.3, and new orders rising to 19.6 from 14.9. Employment and wages were firm, while prices paid rose to another record high of 82.1. The future components were also strong, with future production rising to 51.7 (from 45.8) and future general activity at 28.6 (prior 15.0).

German CPI in November was stronger than expected at 5.2%y/y (est. 5.0%y/y), with a firmer harmonised reading of 6.0%y/y (est. 5.6%y/y), +0.3%m/m (est. -0.2%m/m).

Aust: The current account balance is expected to post its tenth consecutive surplus in Q3, lifting further due to elevated commodity prices and higher volumes (Westpac f/c: $31.0bn). Q3 net exports should positively contribute to GDP as exports continue to outperform delta-affected imports (Westpac f/c: 1.2ppts). The successful health response to delta is anticipated to lift public demand further in Q3 (Westpac f/c: 1.2%). The unwinding of HomeBuilder and partial reversal of Sydney’s high-rise approval spike should see October’s dwelling approvals decline further (Westpac f/c: -4.0%). Meanwhile, private sector credit growth is expected to rise in October as businesses utilise credit to navigate the final stages of the delta lockdowns (Westpac f/c: 0.5%). RBA Deputy Governor Guy Debelle will appear on a panel at the 2021 Symposium on Indigenous Economies at 9:05am, followed by a “fireside chat” at the ACI conference at 1:00pm.

NZ: Measures of activity are expected to hold firm in November’s ANZ business confidencesurvey; inflation gauges should be monitored as prices and costs continue to rise.

China: November’s manufacturingand non-manufacturing PMIs should continue to highlight the underlying strength of China’s economy despite ongoing delta outbreaks and the risk of power outages (market f/c: 49.7 and 51.4 respectively).

Eur: November’s CPIresult is expected to show a further lift, with recent inflation pressures likely to persist well into 2022 (market f/c: 4.5%yr).

US: September’s FHFA house prices and S&P/CS home price index are expected to report robust monthly gains given the strength of underlying demand (market f/c: 1.2% and 1.25% respectively).Ongoing delta concerns are however expected to hold back consumer confidence in November (market f/c: 110.7). Manufacturing’s strength is evident in the Chicago PMI, but supply disruptions and delta remain ongoing issues (market f/c: 67.0). FOMC Chair Powell and Treasury Secretary Yellen will appear before a Senate Panel on CARES Act relief. New York Fed President Williams will also give opening remarks at the New York Fed food insecurity event. The FOMC’sClaridaand Mester will then discuss Fed independence, foundations and responsibilities.

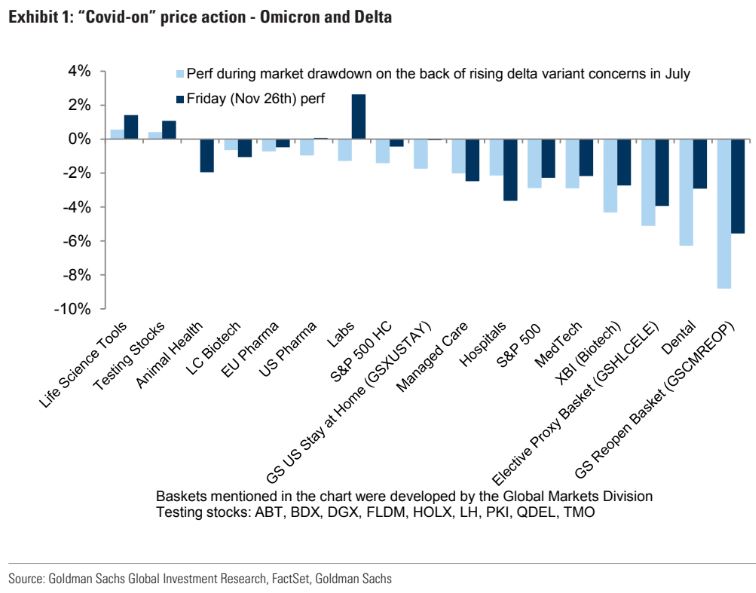

There’s nothing new on Omicron. Goldman offers four scenarios:

(1) in a first“downside” scenario, a large Q1 infection wave leads to a tightening in our global GS Effective Lockdown Index (ELI) that looks similar to the “Delta” tightening but then gradually abates with the distribution of new vaccines and antivirals; (2) in a second and less likely “severe downside” scenario, both disease severity and immunity against hospitalizations are substantially worse than for Delta, with global growth substantially lower than in the first downside scenario; (3) in a third “false alarm” scenario, Omicron spreads less quickly than Delta, and has no significant effect on global growth and inflation, and (4) an upside scenario where Omicron is slightly more transmissable but causes less severe disease, and where a net reduction in disease burden leaves global growth higher than in our baseline. Given the range of medical and economic outcomes, as well as the possibility of a “false alarm”, our Econ team is not making Omicron-related changes to our growth, inflation, and monetary policy forecasts until the likelihood of these scenarios has become somewhat clearer.

It is interesting that the AUD has barely budged from the bottom of its sell-off. There is more going on with that weakness than just a virus scare.

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed. Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website. Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.