US NFIB small business optimism fell to 97.1 (est. 97.5, prior 98.9), with supply chain constraints pushing up prices and a tight labour market being cited as factors behind the fall in the index to an 11-month low. The trade deficit in December at -USD80.7bn (est. -USD83bn, prior revised to -USD79.3bn from -USD80.3bn) made a record annual deficit of -USD859.1bn, on surging consumer goods imports.

Event Outlook

Aust: The February Westpac-MI Consumer Sentiment survey should be supported by the tentative signs of easing omicron impacts, although the shifting interest rates outlook may partially offset.

China: M2 money supply growth should remain steady in January and is ample for robust activity growth (market f/c: 9.2%). Meanwhile, new loans for January should point towards strong credit growth, setting the scene for an acceleration in investment throughout this year (market f/c: CNY3750.0bn). Note, the M2 and loan data is due 9-15 January.

Ger: Although trade surplusis expected to narrow in December, the outlook for 2022 is positive as the global recovery ensues (market f/c: €11.0bn).

US: The final estimate of December’s wholesale inventorieswill confirm the willingness of firms to work through supply issues and rebuild stock. The FOMC’s Bowman will speak to the Independent Community Bankers of America; meanwhile Mester will discuss the economic and policy outlook.

3rd party Ad. Not an offer or recommendation by Investing.com. See disclosure here or remove ads.

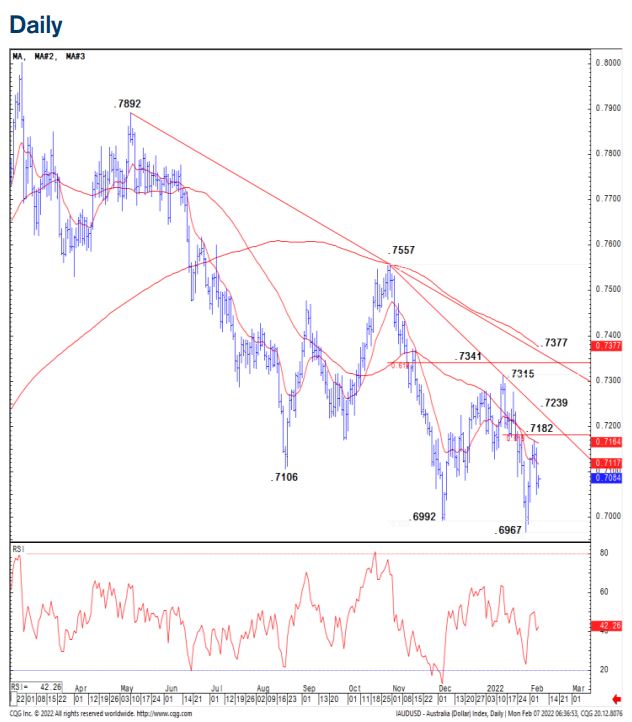

AUDUSD fell sharply on Friday to suggest that the corrective recovery has already ended AUDUSD fell sharply on Friday after the rejection of its key falling 55-day average and is showing signs the corrective strength of the past week is coming to a close. Although further weakness is needed to reestablish the core downtrend, we remain with our bearish view. Support is seen at .7063 then .7033, below which should reinject additional downside momentum for a further move back lower and an eventual retest of the January lows at .6966, with a sustained break below opening the door to the 50% retracement of the entire 2020/21 uptrend at. 6758. Immediate resistance moves to .7109, but with strength above here ideally capped by the 13-day exponential moving average, seen at .7156. A continued break above would see scope for a longer consolidation phase, which we expect to be capped by the 55-day moving average at the very latest, seen at .7162. We look for a move back lower with an eventual retest of the key support at .6966.

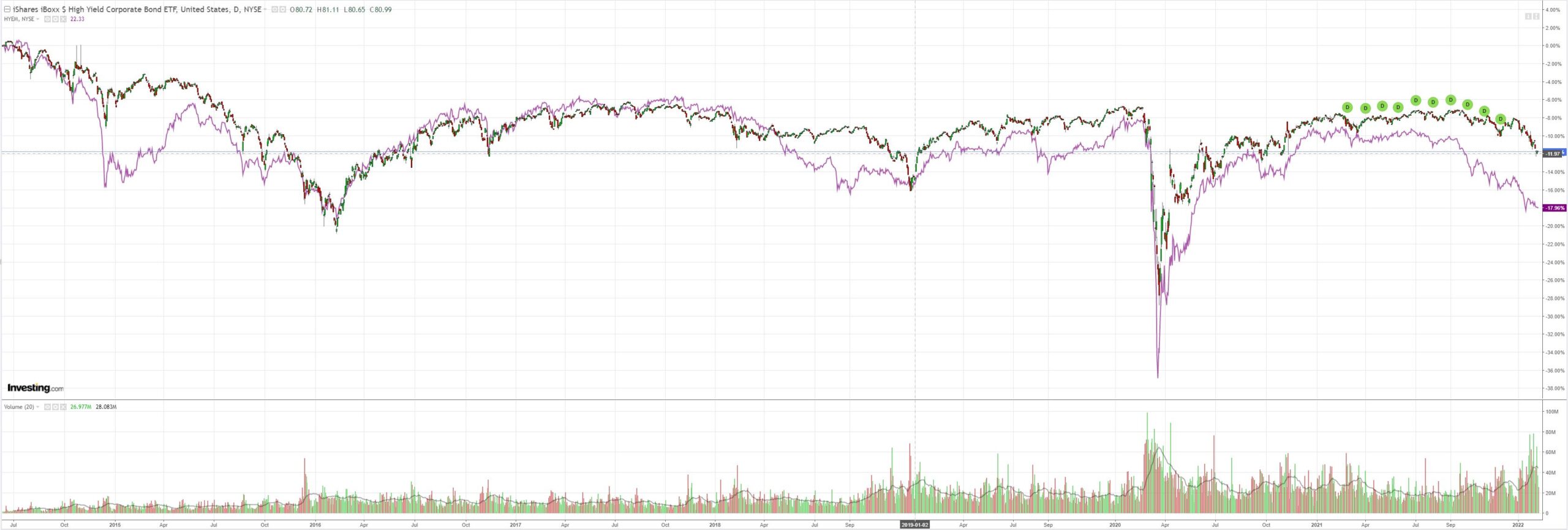

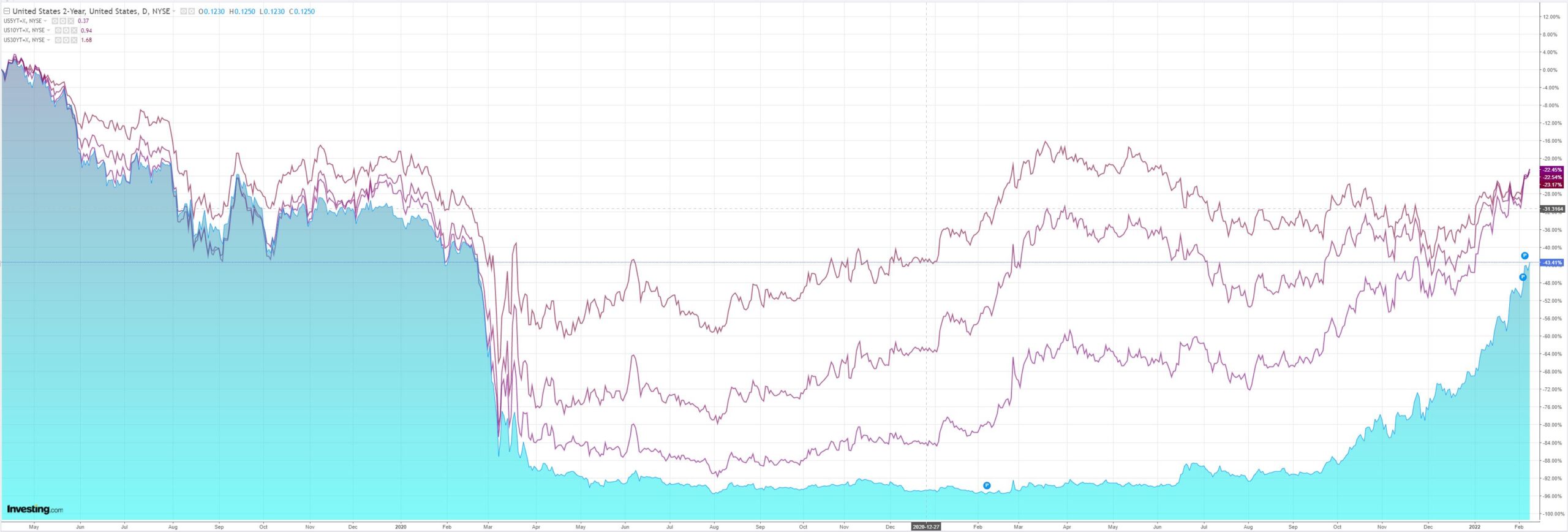

Trend lower until the Fed breaks.

Which stock should you buy in your very next trade?

With valuations skyrocketing in 2024, many investors are uneasy putting more money into stocks. Unsure where to invest next? Get access to our proven portfolios and discover high-potential opportunities.

In 2024 alone, ProPicks AI identified 2 stocks that surged over 150%, 4 additional stocks that leaped over 30%, and 3 more that climbed over 25%. That's an impressive track record.

With portfolios tailored for Dow stocks, S&P stocks, Tech stocks, and Mid Cap stocks, you can explore various wealth-building strategies.

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed. Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website. Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.