This article was written exclusively for Investing.com

Yields have risen sharply across the Treasury curve and have even started showing signs of inversions. While rates in bonds are soaring, and even, perhaps, indicating a not so bright economic outlook, the S&P 500 has been rising. It is especially odd considering the dividend yield of the S&P 500 is moving lower and against the trend in the bond market.

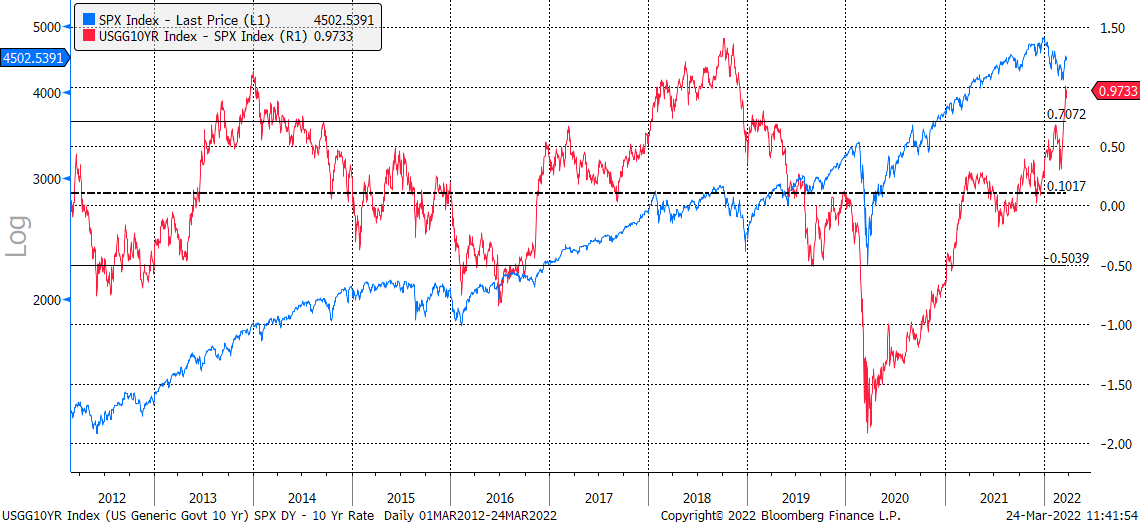

Historically, the difference between the S&P 500 dividend yield and the 10-year Treasury rate is wide. Over the past 10 years, the average spread between the 10-year Treasury rate and the S&P yield has been around 10 basis points (bps). That spread has widened to around 97 bps in recent days, at the very upper bound of that historical range.

The standard deviation between the historical average has been around 60 bps, which places the spread in a range of -0.5 bps and 0.70 bps. The current spread is more than one standard deviation above that historical range, and typically when the spread widens by this much, it eventually leads to a contraction.

Spread Widens

The big spread also tends to lead to markets that go through a period of consolidation or decline, such as witnessed from 2014 through 2016 and during much of 2018. It is yet another example of the market's similarities today with the market of those two periods.

It indicates that the current dividend yield of the S&P 500 is too low given where the 10-year Treasury rate is. The last time the dividend yield of the S&P 500 was this low, or in this region was back in the late 1990s, during the prior stock market bubble.

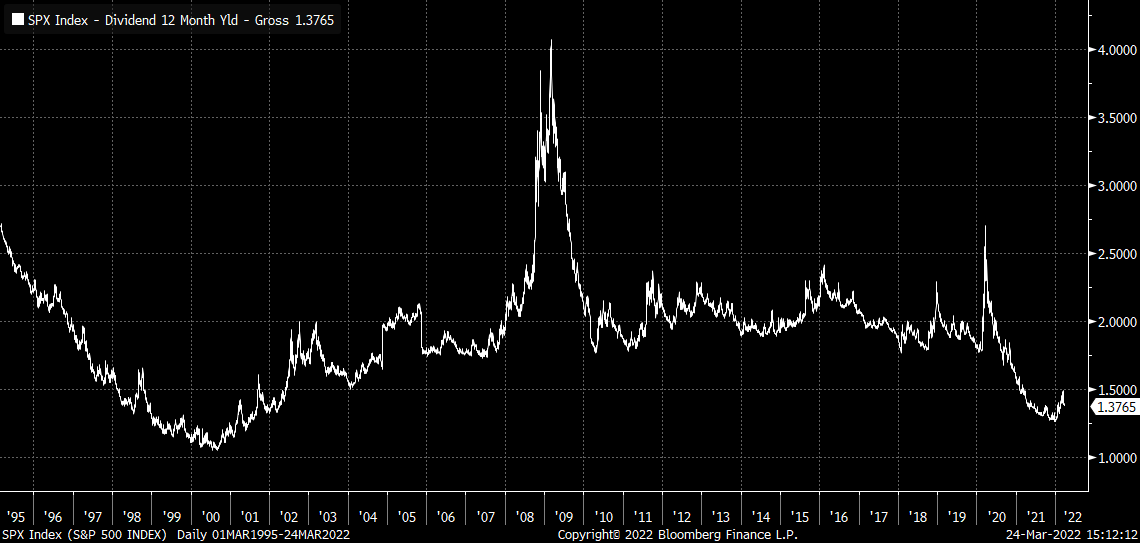

A Big Disconnect

Over the past 10-years, the dividend yield of the S&P 500 has averaged around 1.92%, within one standard deviation of that average between 1.68% and 2.17%. A return to just 1.68% would put an immense hurt on the value of the index.

Consensus estimates call for the S&P 500 to have a dividend of $67.83 per share over the next twelve-month period. Assuming the lower end of the range for a potential dividend yield on the S&P 500 would put the index at around 4,060. But to get back to the historical average of 1.92%, the index would slide to 3,570.

Of course, it isn't to say the market is due for a big dive, but one would think that with Treasury yields moving higher, the dividend yield of the S&P 500 should start to move higher with it over time. After all, the S&P yield versus the 10-year is now at a historically wide point, which typically hasn't lasted for very long.

It is possible too that the 10-year Treasury is misaligned and that its value is what needs to fall back to the S&P 500 yield to help contract the spread. But what is clear is that currently, there is a mispricing in the market and something is off base. Given that the Fed is on a mission to tighten monetary policy, reduce the size of its balance sheet, and tighten financial conditions, the odds favor the S&P 500 being the one offsides.