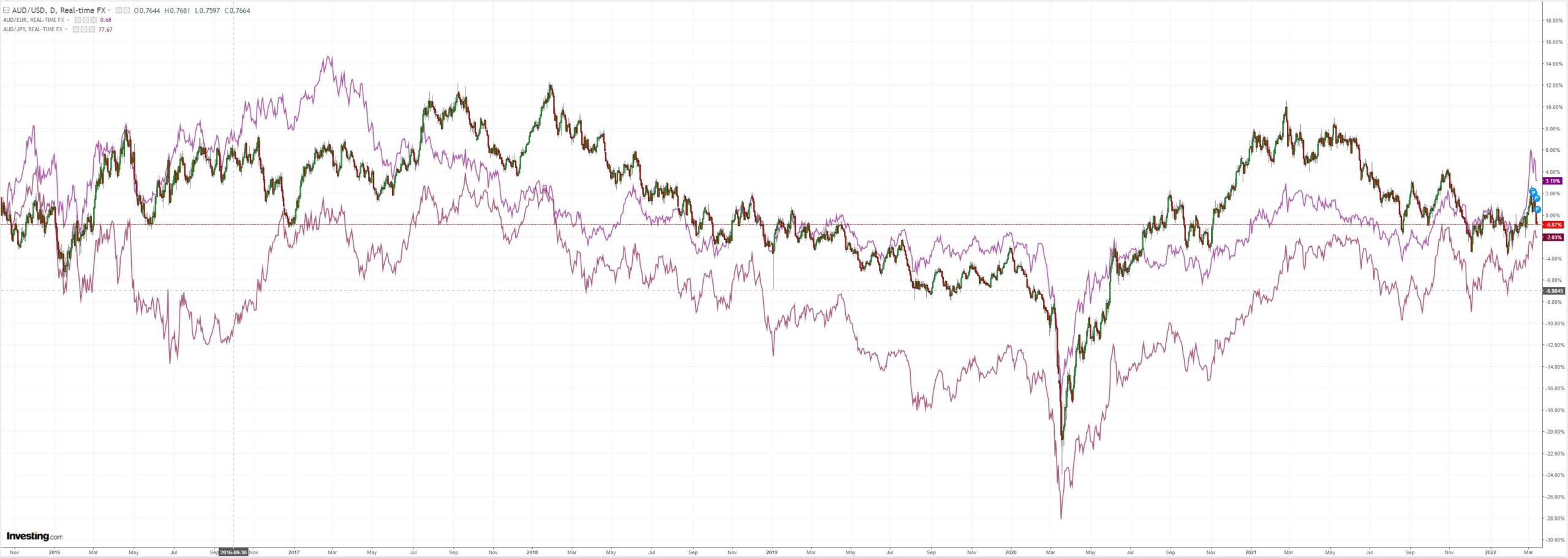

The key to the suddenly not so strong AUD is the pace at which China worries are overtaking Ukraine bullishness for commodities. BMO with more:

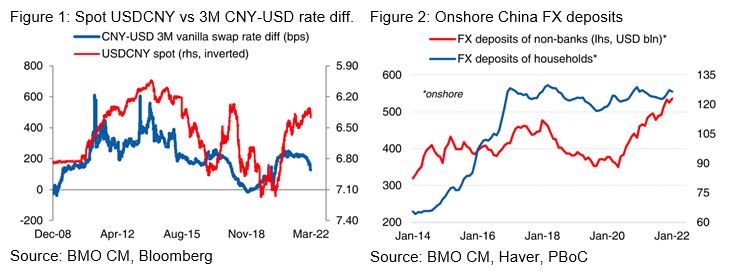

USDCNY/CNH/HKD: Spot USDCNY is now the main (or most important) mover in the FX market week to-date. We think there may be more than one factor driving the move lower in the RMB. On the administrative side, PBoC set the USDCNY mid-rate considerably above market expectations yesterday and today (i.e by an average of 140pips). In one of last week’s FX Dailies, we noted that the recent performance of the RMB was at odds with expectations for looser monetary policy in China (relative to the Fed), and the potential for narrower profit margins for SoEs and exporters (Figure 1). We didn’t think USDRMB would bounce quite as much as it has so soon (we were flagging the bottom in the 6.25/6.30 range), but this week’s decline in energy prices has also taken us by surprise. That development, in combination with a very low chance of a 50bps rate hike from the Fed tomorrow, are probably a relief for the PBoC, leaving the central bank with more flexibility to allow the RMB to respond to fundamentals (and flows). Given the move in USDHKD closer to the top of the HKMA’s trading band, we suspect that non-resident investors are now trimming their exposures to China, given the recent escalation of tensions between the West and China over Russia (i.e. a degree of outflows). The build-up of the trade surplus and the surplus of onshore foreign liquidity (Figure 2) are still enormous buffers against a sharp RMB depreciation. And after two (2021) hikes in the RRR on foreign currency deposits, we don’t think many Chinese investors or Chinese corporates and banks are significantly short of USDs. Policymakers in China have been preparing for the start of the Fed’s tightening cycle for months, and the recent depreciation of the RMB will be warning sign to USD shorts to ‘get their houses in order’. On the macro side, policymakers do not want to encourage a severe misalignment (RMB overvaluation) as fundamental developments evolve, and we think it’s quite clear that they see downside risks building for global industrial output and international trade growth; these downside risks have only increased since the lockdown of Shenzhen was announced. But we should also note the dynamic in other currency pairs as well: this depreciation of the RMB is not occurring alongside severe USD strength along other key axes at the moment (i.e. EURUSD). As such, this phase of RMB depreciation is offset somewhat by weakness in the USD vs other key currencies. We see additional short-term upside squeeze risk in spot EURCNH, though our medium-term fundamental view for this pair is still for additional weakness.

I expect more CNY weakness ahead as the PBoC is forced to cut more than it cares to admit. In the context of tightening Fed, this is very bad for commodities, EMs because trade and capital accounts come under simultaneous pressure. It is also bad for the AUD:

Where CNY goes, AUD follows. Or is it the other way around? Given the Aussie quarry is often a good leading indicator for Chinese carry.

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed. Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website. Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.