US CPI inflation was stronger than expected in June, rising 1.3% m/m and 9.1%y/y (est. 1.1% and 8.8%) – a high since 1981. The core rate rose 0.7%m/m and 8.8% (est. 0.5% and 5.7%). Nearly every major component increased. Energy prices rose another 7.5%, housing costs 0.8%, food/beverage prices 1.0%, and transportation 3.8%.

The Fed’s Beige Book of regional economic conditions reiterated that the economy expanded at a moderate pace, but “several Districts reported growing signs of a slowdown in demand, and contacts in five Districts noted concerns over an increased risk of a recession.”

FOMC member Bostic said “everything is in play” at the July policy decision following the “concerning” CPI report, which could infer a 100bp hike. He is worried about the broadening in inflation. Were the headline pressures driven by one or two factors that have outsized weights, he might think of it differently than if it were broad-based (which it is).

Bank of Canada surprised with a 100bp rate hike (consensus was 75bp), taking the policy rate to 2.50%. It is now the leader in central bank assertiveness, as it front loads the policy path. It indicated more increases are needed, saying that inflation has been higher and more persistent than expected and is likely to stay around 8% over the next few months. It also noted consumer expectations surveys point to higher inflation for longer.

Event Outlook

Aust: Given the robust demand for labour as evinced by high levels of job vacancies, Westpac anticipates employmentto lift at an around trend pace of 35k in June (market consensus 30k). With participation holding steady at record highs, the unemployment rate should tick downwards to 3.8%. Meanwhile, MI inflation expectationswill continue to mirror the strength of inflation in June.

US: Producer inflationis expected to remain at an elevated level given ongoing supply issues (market f/c: 0.8%) and initial jobless claimsare set to hold at a low level (market f/c: 235k). The FOMC’s Waller is also due to speak.

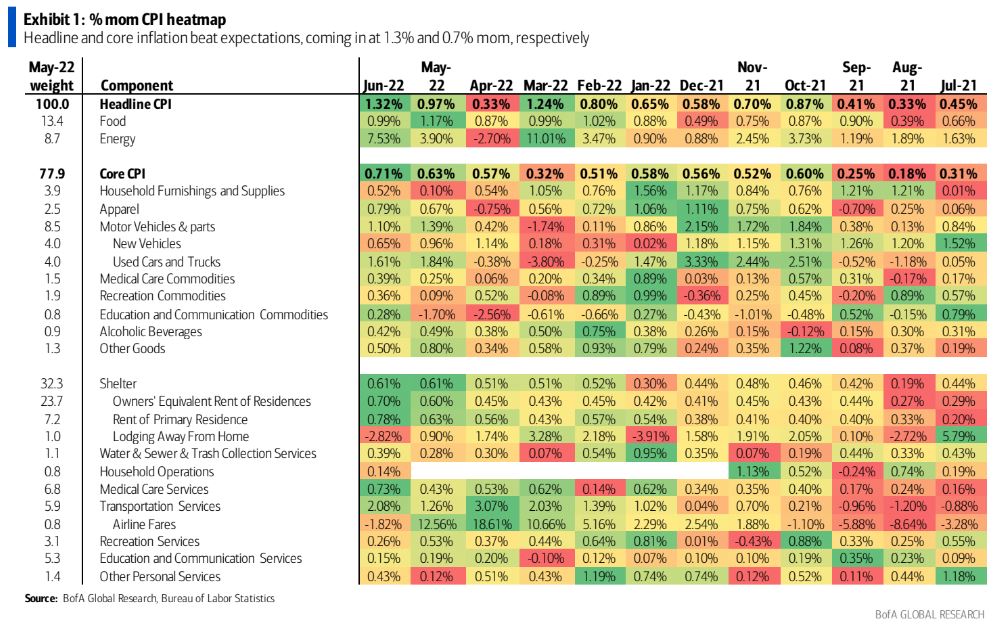

BofA the analysis:

Headline CPI prices surged by1.3% (1.32% unrounded) mom in May, beating consensus expectations of a 1.1% increase. Energy prices spiked 7.5% mom as gasoline prices reached record levels in mid-June. Food prices increases 1.0%. Yoy headline CPI inflation made a new 40-year high of 9.1%.

More importantly from the Fed’s perspective, the core CPI also beat expectations, rising 0.7% (0.71% unrounded) mom versus consensus at 0.6%. The yoy rate dropped from6.0%to 5.9%, because of base effects. The strength in core inflation was broad-based.Core commodities rose 0.8%as new and used car prices took another leg up, rising by0.7% and 1.6% respectively. Apparel, medical care commodities and other goods saw increases of 0.8%, 0.4% and 0.5%, respectively.

Meanwhile core services increased by 0.7%. The main driver was a 0.6% increase in shelter prices (OER and rentals were up 0.7% and 0.8%). Medical care services prices also increased sharply by 0.7%. The one silver lining in this report is that travel-related inflation appears to have cooled off: lodging was down 2.8% and airline fares fell 1.8%. However, airfares remain very elevated: they are up 56% year-to-date.

While the decline in energy prices in the last few weeks points to near-term relief on headline inflation in the coming months, we think the main takeaway from this report is much-stronger-than expected underlying price pressures in both core goods and core services. Our outlook for core goods includes mild deflation over the coming year, but there is little in this report to suggest it is coming anytime soon. In addition, core services inflation is likely to remain sticky given the continued strength in the labor market. One potential nuance is that PCE inflation might come in meaningfully softer than the CPI–as has been the case for the last two months–given the lower weight of shelter in the PCE. The PCE outlook will become clearer after tomorrow’s PPI report.

Nonetheless, the bottom line is that this report keeps the Fed on its tightening path. We continue to expect a 75bp hike in July and a 50bp hike in September. Today’s report is also consistent with our view that the“inflation tax” will weigh on consumer spending, driving the economy into a mild recession.

Whether it is mild or not will depend upon what the Fed breaks along the way.

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed. Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website. Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.