US PMIs for March surprised higher, with Composite rising to 58.5 (est. 54.7, prior 55.9) on gains in both manufacturing and services. The report cited rising domestic demand and export new orders. Prices remained at very high levels. The Outlook slipped, but remains at “encouragingly resilient” levels despite the rising geopolitical concerns. Weekly initial jobless claims fell to 187k (est. 210k), as did continuing claims at 1.35m (est. 1.40m). Durable goods orders in February fell 2.2%m/m (est. -0.6%m/m, prior revised to +0.8%m/m from +0.7%m/m). The ex-transport reading was also soft at -0.6%m/m (est. +0.6%m/m, prior revised to +1.3%m/m from +1.0%m/m). Kansas Fed manufacturing activity survey rose to a record 37 (est. 26, prior 29).

FOMC member Evans said he is comfortable with increasing rates by 25bp at the remaining FOMC meetings this year, but is “open minded” regarding a 50bp tightening. He doubts the Fed’s path would drive the economy into recession., and also supports the plan to reduce the balance sheet quickly. Kashkari has pencilled in 7 hikes – a significant shift by this dovish member. Waller said he is monitoring rising home prices for possible stability risks.

Norges Bank raised its policy rate by 25bp to 0.75%, as was widely expected, and flagged that more is likely to come in June. The statement highlighted ongoing improvements in activity, flagged heightened uncertainty in light of the war in Ukraine, and emphasized that “price and wage inflation has been higher than expected and wage expectations have risen”. Norges warned that “if there are prospects of persistently high inflation, the policy rate may be raised more quickly”.

Swiss National Bank kept its policy rate on hold at -0.75%, as was widely expected. The central bank warned the war in Ukraine could hurt economic growth.

EurozoneComposite PMI fell to 54.5 (est. 53.8, prior 55.5). UKComposite PMI remained firm at 59.7 (prior 59.9, est. 57.5).

Event Outlook

China: The final estimate of the Q4 current account balance should confirm the robust strength of exports as it leads the surplus to a near 15-year high.

Eur/Ger/UK: EuropeanM3 money supply growthis expected to hold steady in February, indicating ample liquidity for the economy (market f/c: 6.3%). Concerns surrounding the Russia-Ukraine conflict are anticipated to weigh on GermanIFO business confidence in March (market f/c: 94.2) while intensifying inflationary pressures should also dampen UKconsumer sentiment(market f/c: -30). As a consequence, weakening purchasing power are a real risk to retail sales(market f/c: 0.7%).

US: Robust underlying strength in demand should continue to buoy pending home salesin February although rising rates should cool this dynamic over 2022 (market f/c: 1.0%). Meanwhile, the final estimate for the March University of Michigan sentimentsurvey will reflect the impact of inflation concerns and geopolitical uncertainties on confidence (market f/c: 59.7). The FOMC’s Daly, Waller, Williams and Barkin are all due to speak at separate events.

We revise our bullish AUDUSD target from 0.7350 to 0.7550, we would look to buy dips below 0.7300 and see the pair in a range between 0.7200 and 0.7600. Second-tier data indicators show rising inflationary pressures, pointing to further risks of an earlier-than-expected hawkish turn in RBA policy rhetoric. Meanwhile, markets will likely continue to view AUD as a clean expression of commodity price strength.

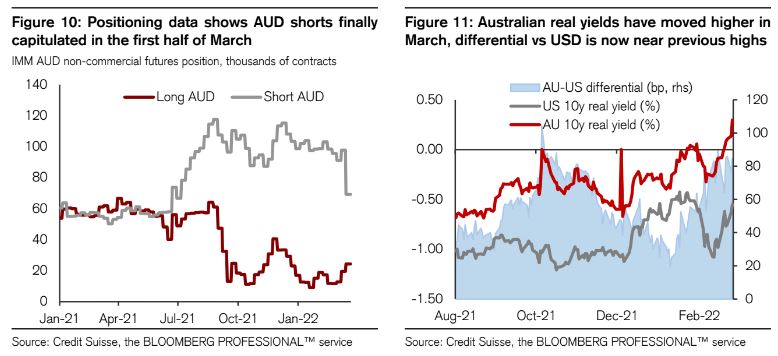

Since our most recent update on AUD on 2 March (link), the balance of drivers of AUD price action has shifted very rapidly to glass half full. Fears of systemic market events related to Russia sanctions have not realized, sentiment around Chinese assets has improved sharply following statements of support by local authorities on 16 Mar and Febemployment data surprised stronger than expected on 17 Mar. These factors have likely all played an important part in driving AUDUSD through our 0.7350 target and to the highest level since Nov 2021, but seem overshadowed by the broader tendency of markets to view AUD as a proxy for commodity prices. IMM data in fact show that a large portion of highly persistent (and often discussed) AUD short positions were liquidated in the week up to 15 Mar (seeFigure10), ahead of many events that we list above.

On the domestic side, another element that has helped AUD is the fact that markets continue to see hawkish shifts in US monetary policy as a reason to anticipate similar developments from the RBA, despite ongoing pushback from the latter. Since 2 Mar, Fed policy tightening expectations implied by OIS in 2022 have increased from 132bp to over 200bp, and from 120bp to 180bp for the RBA. Similarly to the US, the recent increase in Australian nominal yields appears to be driven by real yields, which have accelerated above0% and have pushed the differential vs the USD equivalent back to the levels last seen in Nov 2021 (seeFigure11).

For the time being, we think the positive thrust of both international and domestic factors is likely to persist. All things equal, this suggests that AUD dips back towards the 200dma around 0.7300 will find buyers, with the Oct 2021 highs around 0.7550 as a near-term target, and potential for spikes as high as near the June 2021 highs around 0.7600. On the international front, actual AUD terms of trade have largely unwound the bulk of the strength seen at the onset of the Ukraine war in late Feb and in early Mar, but this is unlikely to be seen as a lasting challenge to AUD strength, as Europe’s frenzied quest to secure new energy sources is likely to channel expectations of further capacity expansion and investment in Australia’s growing LNG industry. The same applies to food exports, with the current concerns about crop planting in Ukraine likely suggesting that Australia’snet agricultural exporter role will remain a net source of support for the currency.

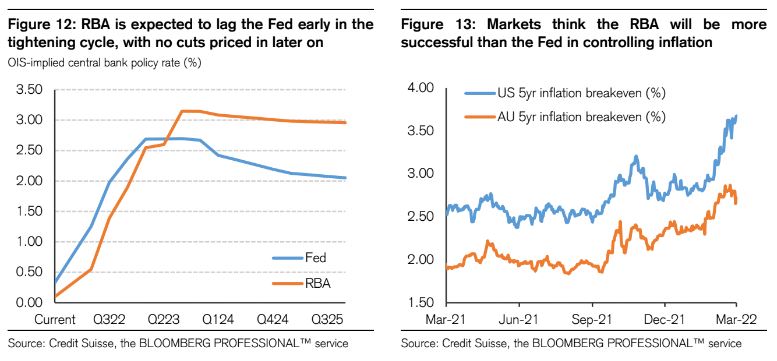

On the domestic front, RBA policy remains in focus. As shown in Figure12, markets are anticipating the RBA to lag the Fed in hiking rates in 2022, with the first full rate hike priced in by the 7 Jun meeting. Markets also expect the RBA tightening cycle to end with a higher terminal rate, with limited pricing for rate cuts beyond the peak of the cycle. This is consistent with more-suppressed inflation expectations, as 5-year AUD inflation breakevens have not followed their USD equivalents higher in the past few weeks. Possible explanations include expectations that the RBA will be more successful than theFed in pushing inflation lower over the medium-term, but also considerations about FX strength easing the blow of rising commodity prices in domestic terms, the still lower level of local CPI (3.5%yoy in Q4) compared to near-8% last seen in the US, and perhaps the lower frequency of Australian inflation and wages data (Q1 CPI and wage growth data releases are due on 26 Apr and 17 May respectively).

Nevertheless, recent data suggest that the risk remains in the direction of further hawkish developments. The Westpac consumer confidence indicator fell in March to the lowest level since Sep 2020, with inflation concerns playing a key role in the decline. While it certainly is notable that Governor Lowe did not discuss this specific data point in his comments on Monday, we think it merits attention, especially with most in markets seeing Federal elections (date still TBD, but likely on 21 May) as a strong obstacle against the RBA hiking rates ahead of the 7 June rate decision, 3 meetings from now. While we acknowledge and fully understand the reasons that underpin these expectations, we also see a risk that the RBA might see further data prints in line with the narrative that emerged from the March consumer confidence indicator as the qualifying factor for the“pervasive shift in inflationary psychology” that Governor Lowe discussed earlier this week.

The Melbourne Institute inflation gauge for Feb on 3 April and the Mar employment report on 14 April will be in focus on this front. And even if a sudden full RBA U-turn on policy patience and a pre-election hike remain at this point still a far tail risk (especially at the upcoming rate decision on 5 April), the possibility of markets moving to further price in the US 5yr inflation breakeven (%)AU 5yr inflation breakeven (%) possibility of a 50bp hike at the 7 June meeting, from currently 35bp, seems like relatively low-hanging fruit.

With all this said, our near-term AUDUSD target revision from 0.7350 to 0.7550 is a fairly moderate one–why is that? The main reason is that while many factors have indeed turned more constructive for AUD, or have potential to do so, the hurdle of a large short position, which we have repeatedly highlighted as a bullish factor for AUD since early Q1, seems much less pressing now than at any point since mid-2021. CAD, where IMM net positioning data has been long since Jan, offers an important cautionary tale on this front, as USDCAD is still trading above 1.2500 even with a much more hawkish monetary policyand an equally supportive terms-of-trade backdrop.

In short, until the Fed gains enough traction with its rate hikes to drop commodity prices the AUD is biased upwards.

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed. Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website. Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.