Despite rising bond yields last year, the strong V-shaped recovery in global equity markets from the COVID crisis of early 2020 largely continued over 2021, powered by ongoing growth in corporate earnings. U.S. equity performance remained preeminent, though there were sector winners among both value and growth areas of the market. Slowing earnings growth but ever-rising bond yields will likely only heighten the challenges faced by global equities in 2022.

2021 in retrospect

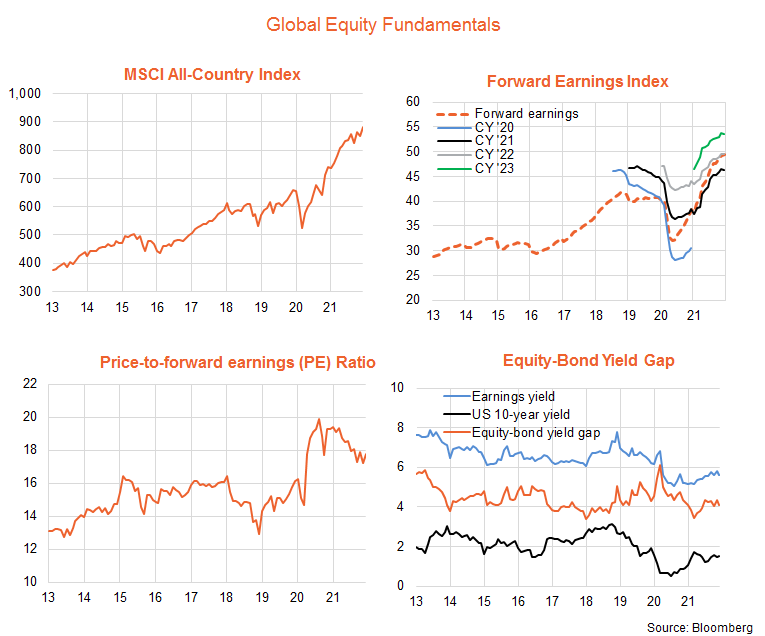

In local currency terms, global equities returned 21.4% in 2021. As evident in the chart below, this reflected a lift in forward earnings (29.1%), partly offset by a decline in the price-to-forward earnings (PE) ratio from 19.3 to 17.8 (-7.7%). Dividends added 2.3% to returns.

The fall in the PE ratio was likely encouraged by the rise in bond yields, with the yield on 10-year U.S. Government bonds rising from 0.92% to 1.51%, or 59 basis points (bps). The downward pressure on the PE ratio would have been greater were it not for the fact the global equity risk premium (or difference in the forward earnings yield less U.S. 10-year bond yield) fell modestly, 4.3% to 4.1%, though still remaining broadly in line with its average of recent years.

Rising Oil prices and bond yields were a major driver of relative sector performance, with the value-orientated energy and financials sectors taking out the first and third place among the 11 major sectors. That said, the more range-bound performance of bond yields over the second half, together with the sheer earnings strength of America’s FAANG stocks, allowed the technology sector to finished the year in second place overall, as evident by the U.S. again outperforming Europe and Japan.

Emerging markets had a fairly muted return, with Australia somewhere in between from a performance perspective.

2022: Challenges of the year ahead

The key challenge for the coming year will be a maturing of the post-COVID global earnings rebound and the likely continued re-normalisation of interest rates. Current expectations are that global forward earnings should rise by a still admirable 10% over the coming year, though this is well down on the near 30% surge in 2021.

Meanwhile, one legacy of the supply-demand imbalances produced by the COVID crisis is uncomfortably high inflation in many countries, especially the United States. The U.S. Federal Reserve has strongly signaled its intention to end bond purchases within the next few months, and raise interest rates at least two to three times this year. My base case view is that this should send U.S. 10-year bonds to at least 2.25% at some stage in H1’22, or a lift of another 75 bps from end-21 levels. If the equity risk premium absorbs half this increase (i.e. it shrinks from 4.1% to 3.75%), it would still imply a decline in the PE ratio to 16.7, or 6% below end-21 levels.

All up, 2022 is likely to be another year where earnings largely underpin the market, at least partly offset by an interest rate-induced decline in the PE ratio. 2022 will be more challenging, however, with a smaller earnings contribution whilst the interest rate pressures will remain at least as great.

Key themes for the year ahead

Rising interest rates and a potentially continued strong U.S. dollar could be key trends that help determine the global equity market winners and losers for the coming year. Another theme could be the allure of companies with relative earnings dependability, as distinct from those with ‘blue sky’ earnings potential many years down the track.

In turn, this suggests three potential investment ideas:

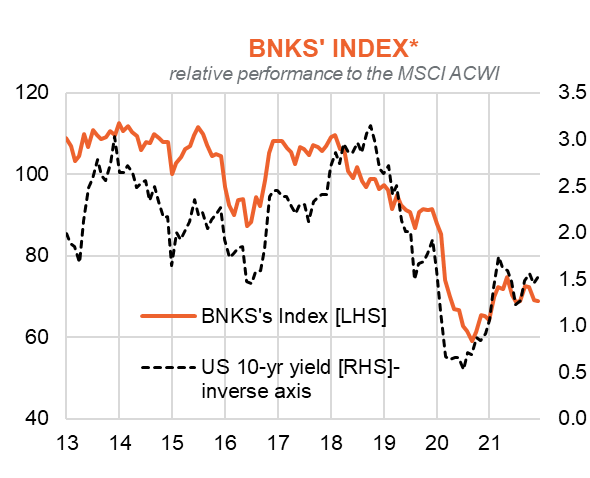

Global banks (via the BNKS ETF)

As noted above, financials were among the top sector performers in 2021, and rising bond yields may well further underpin this sector’s performance in 2022. Provided higher interest rates don’t unduly slow economic growth or the credit outlook, the chart below highlights that global banks tend to outperform in a rising bond yield environment as the latter helps fatten their net-interest margins (medium-term lending rates rise more than shorter-run deposit rates).

The BetaShares Global Bank ETF (ASX:BNKS) provides exposure to the largest banks in the world on a currency-hedged basis.

*Source: Bloomberg. Past performance is not an indication of future performance or the Index or the ETF. You cannot invest directly in an index. The graph shows the performance of BNKS’ index and does not take into account BNKS’ fees and costs. The Index which BNKS aims to track is the Nasdaq Global ex-Australia Banks Hedged AUD Index.

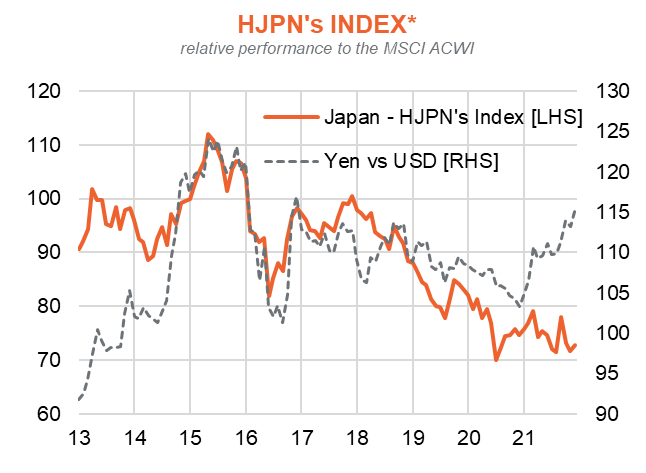

Japanese stocks (via the HJPN ETF)

Along with shorting Japanese bonds, overweighting Japanese equities has been an unsuccessful ‘widow trade’ for many years. Indeed, Japanese stocks did not display much outperformance last year even though the Yen weakened – which ordinarily tends to help the export-sensitive Japanese market. Political instability and COVID-related concerns appear to have held back investor sentiment last year even though growth in corporate earnings was ultimately quite robust.

With the U.S. dollar likely to remain firm (thanks to the Fed), COVID and political concerns likely to ease, and Japanese stocks looking relatively cheap compared to their U.S. counterparts, 2022 could be the year in which Japan enjoys at least some time in the sun.

The BetaShares Japan ETF (ASX:HJPN) provides currency-hedged exposure to large Japanese listed companies that tend to derive a substantial share of their revenues from export markets.

*Source: Bloomberg. Past performance is not an indication of future performance or the Index or the ETF. You cannot invest directly in an index. The graph shows the performance of HJPN’s index and does not take into account HJPN’s fees and costs. The Index which HJPN aims to track is the S&P Japan Exporters Hedged AUD Index.

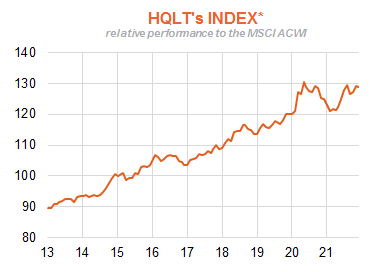

Global Quality (via the HQLT/QLTY ETFs)

Not quite growth and not quite value, ‘quality’ global companies are those that tend to enjoy an above average return on equity without undue leverage. It’s the consistency of their earnings growth that makes these companies attractive, and as evident in the chart below, they have tended to enjoy market-beating returns over recent years. Indeed, over the market cycle, ‘quality’ as a factor has tended to outperform in most periods except the early stages of recovery from an economic downturn/bear market (as last evident in mid-2020).

At a time when many speculative growth companies (with strong potential for earnings growth at some stage in the future) may come under pressure from rising interest rates, ‘quality’ companies may continue to hold up relatively well in 2022.

The BetaShares Global Quality Leaders ETF – Currency Hedged provides currency-hedged exposure to 150 global companies that rank most highly in terms of a carefully selected range of ‘quality’ criteria, such as return on equity, earnings stability and balance sheet strength. Exposure to these companies is also available on an unhedged basis via the QLTY ETF, which may be favoured by investors who (not unreasonably I think) retain a negative view on the Australian dollar.