-

Best Buy is a consumer electronics retailer, trading, like many other peers, near its 52-week low. Despite or perhaps because of that, InvestingPro views it as one of the most undervalued stocks.

-

This article shows how we found Best Buy Co (NYSE:BBY), what its set-up is, what headwinds it is facing, and what upside potential it has.

-

If you’re interested in upgrading your search for new investing ideas, check out InvestingPro.

-

Current price/52-week range: $77.12 ($69.07 - $141.97)

-

Market cap: $17.40 billion

-

P/E Ratio: 8.7x

-

Revenue compound annual growth last 5 years: 5.6%

Another Retail Opportunity

As the market continues to search for a direction heading into the summer, a number of sectors are continuing to suffer. Retail is one of them, as investors try to understand whether demand shifts are temporary or permanent, and as inventory challenges continue to pop up for firms.

Last time, we wrote about The Children's Place (NASDAQ:PLCE), a clothing retailer with strong fundamentals even as it is exposed to cost inflation and a difficult environment. This time, using InvestingPro tools, we will analyze another retailer that may be set up to deliver strong returns despite what looks like a difficult short-term situation.

This article will analyze Best Buy (NYSE: BBY), a prominent player in the Specialty Retail industry. Given the InvestingPro model suggested significant upside potential, great financial health, and recent quarterly earnings discussed in detail in this article, we believe the company is poised to outperform the market even amid ongoing inflationary pressures that negatively affect the industry.

Note: All pricing data is as of June 8th closing price.

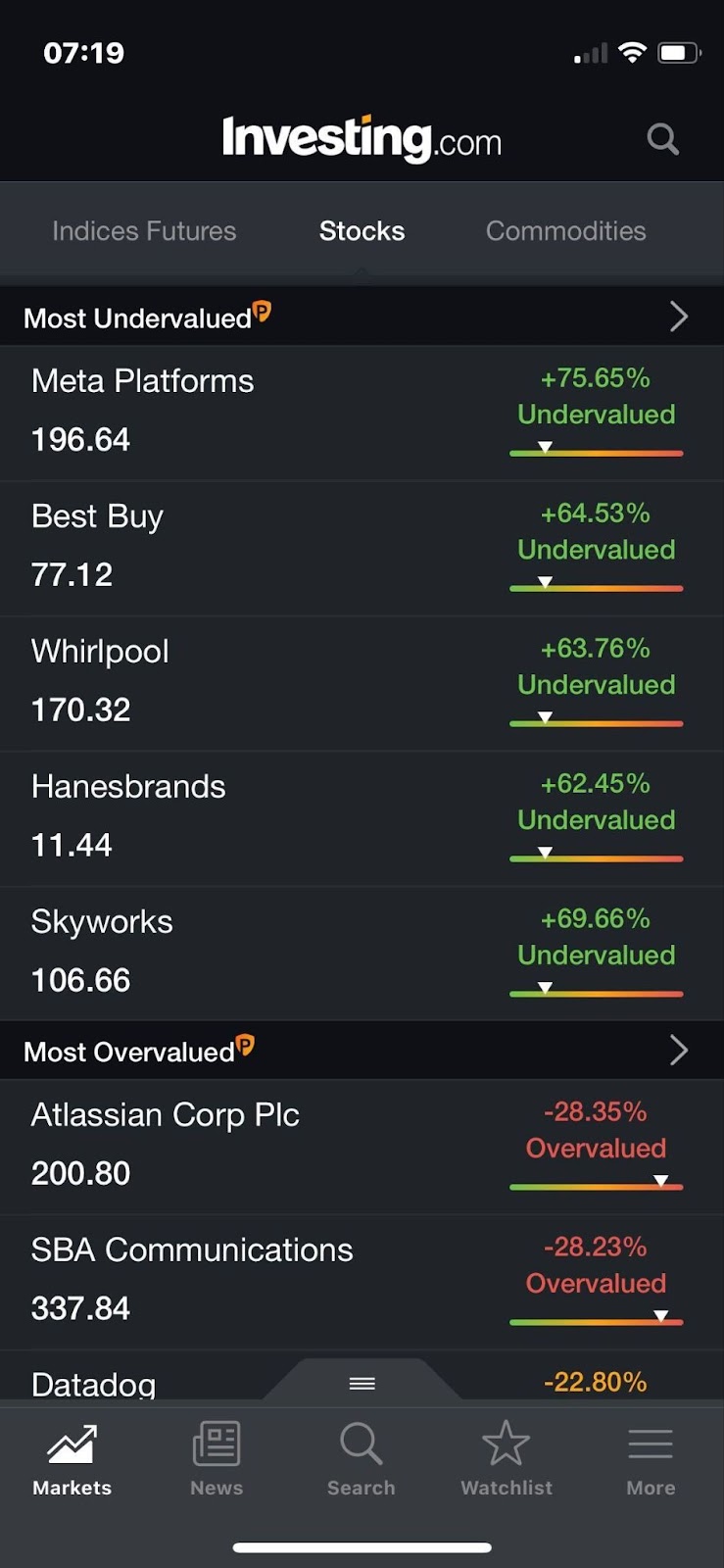

Finding a Bargain Stock

Let’s go step-by-step through the process of selecting Best Buy as today’s stock for analysis. We started with Investing.com mobile app. InvestingPro shows the list of most undervalued/overvalued stocks, out of which Best Buy caught our attention. Given the remaining challenges in the Retail sector, and the recent huge stock selloff following some big players’ disappointing quarterly results, Best Buy seemed an interesting candidate with its 64.5% upside potential. Moreover, the company’s stock price is still down 24% year to date, even after its recovery from the mid-May 52-week low.

Source: InvestingPro

Best Buy: Is Now the Right Time to Invest?

Basic stats:

Best Buy Co., Inc. is one of the prominent players in the Specialty Retail space, selling technology products in the United States and Canada, through its 1,144 stores (as of January 30, 2022) and its websites under the Best Buy, Best Buy Ads, Best Buy Business, Best Buy Health, CST, Current Health, Geek Squad, Lively, Magnolia, Best Buy Mobile, Pacific Kitchen, Home, and Yardbird, as well as domain names bestbuy.com, currenthealth.com, lively.com, yardbird.com, and bestbuy.ca.

InvestingPro shows that the average price target for the 21 analysts who follow the stock, is $94.24 (22.2% upside from current stock price), while the fair value based on InvestingPro models is $126.89 (64.5% upside from current stock price).

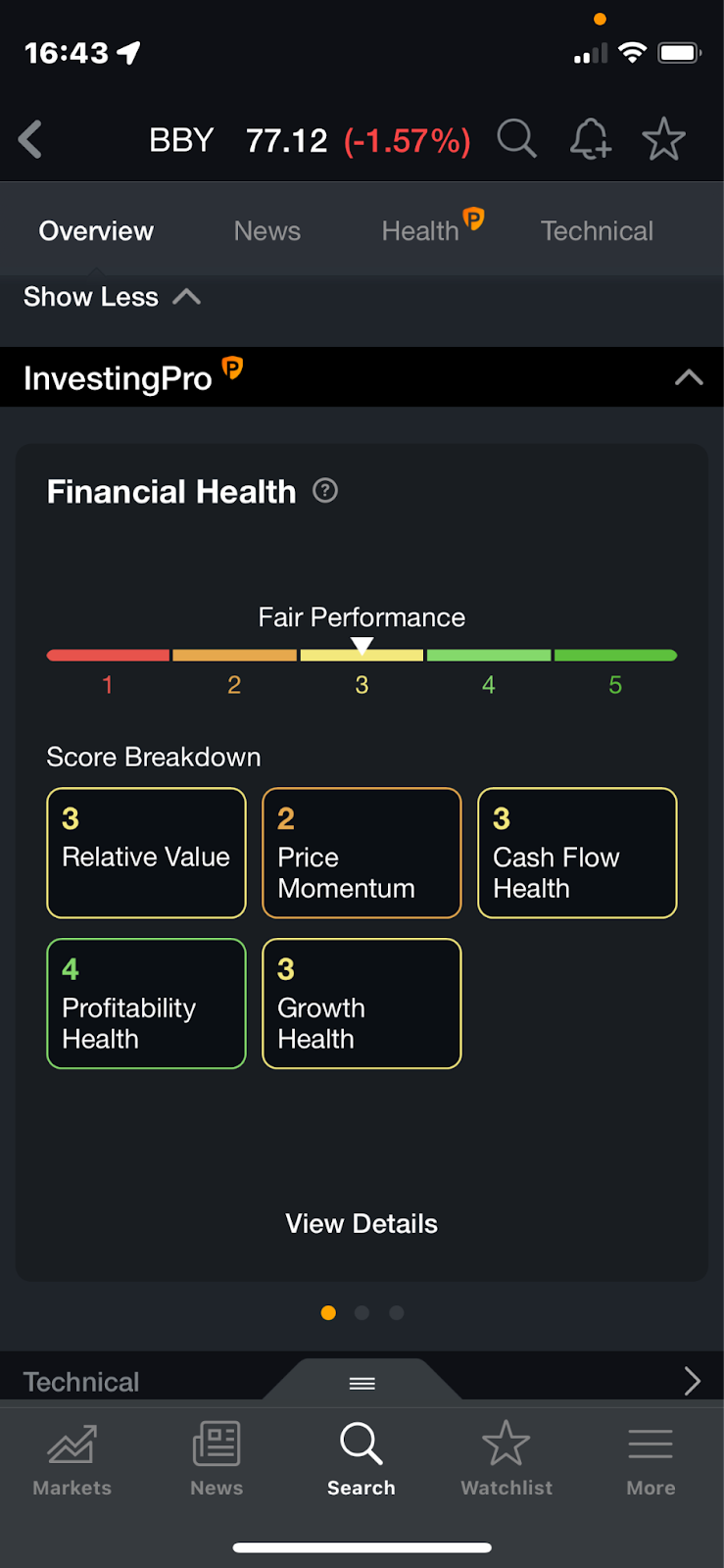

Source: InvestingPro

InvestingPro rates the company’s financial health as a 3 out of 5, positioning Best Buy for fair performance, with profitability health as the highlight.

Source: InvestingPro

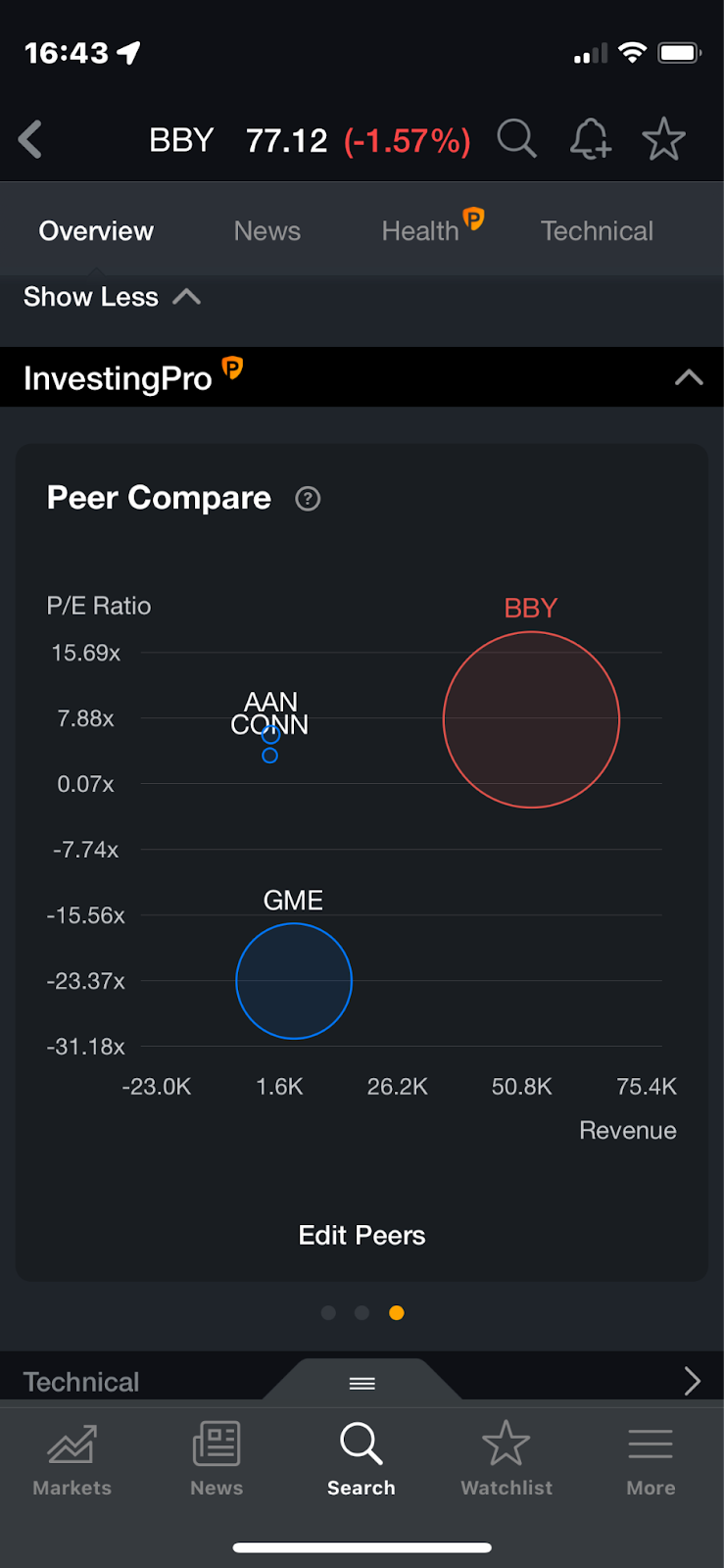

As can be seen from the Performance vs. Valuation Benchmarks graph, all of the company’s peers also have very low PE ratios.

Source: InvestingPro

Facing Uncertain Macro Environment

Best Buy Co., Inc., as well as the majority of its peers, face pressures due to rising inflation and interest rates, affordability issues for key products, the Russia/Ukraine War further weighing on consumer confidence, and further supply chain challenges in China. But the company seems to manage well in this challenging macro environment, as can be noticed from its recent quarterly earnings report. Furthermore, the company is benefiting from rising demand for certain products, such as laptops and computer accessories as many raced to buy products for their home offices due to the COVID-19 pandemic.

Recent Earnings Report & Outlook

On May 24, 2022, the company reported its Q1 results, with revenue coming in at $10.65 billion, beating the consensus estimate of $10.44 billion. EPS was $1.57, compared to the consensus estimate of $1.63. The stock price increased about 14% since the earnings announcement.

Despite the miss, the company lowered its full 2023-year guidance less than feared. It now expects EPS in the range of $8.40-$9.00, compared to the Street estimate of $8.90, and revenue in the range of $48.3-49.9 billion, compared to the Street estimate of $50.12 billion.

Management expressed uncertainty on how long sales declines could persist on the back of elevated stimulus spending in 2022 or overall consumer spending slowing down in 2023 due to inflationary concerns and/or shifts in consumer spending away from durables to experiences.

Despite the lower outlook, the company expects a material sequential improvement in comp sales.

Summary

At a price point of $77.12, we believe Best Buy Co., Inc. is poised for growth. First of all, the recent quarterly results showed the company is managing well despite ongoing macro challenges. Given the stock popped initially after its recent earnings announcement, bouncing back from its 52-week low on May 20, it seems investors are optimistic about the outlook, and the worst may be priced in.

Second, Pro model-based fair value estimate of $126.89 implies an upside of 64.53% in the next 12 months. And finally, the Pro profitability health score of 4 is a reminder that BBY’s business is solid and set up for success.

Disclaimer: The author has no positions in any stocks mentioned in this article.