Citi has some nice analysis of the DXY bull market:

Running with the bulls

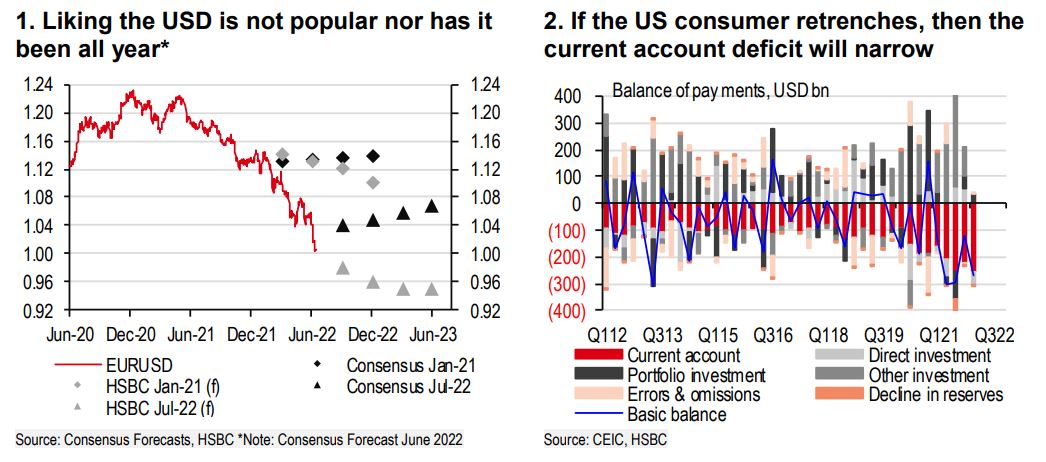

The dollar’s bull run started close to a year ago and is showing little sign of coming to an end, as we discussed in the previous edition of the Currency Outlook (see Currency Outlook: The pause that refreshes, 9 June 2022). In fact, we believe it has more room to run and we have upgraded our USD forecasts further, especially versus European currencies. Our belief in the strong USD has been in place for nearly a year given the hawkish Fed and slowing global growth but remains non-consensus. Despite us adopting a strong USD stance nearly a year ago, we have not been bullish enough. What stands out, however, is the consensus looking for the USD to fall, as it has done so consistently. A prime example is EUR-USD which forecasters still see rising in the year ahead (Chart 1). There are many arguments put forward for why the USD will decline but these continue to be misjudged.

Take, for example, US recession risks and what this could mean for the USD. The speed of a US slowdown matters. Plus, the old adage of when the US economy catches a cold, then the rest of the world feels worse still holds. The US consumer has been a key support for the global economy in the last few quarters, as evidenced by the strength of private consumption in the annual accounts relative to other economies, the relative retail sales trends, and the widening US current account deficit (Chart 2).

While some might see that deficit as another risk to the USD, it highlights just how important the US has been to the rest of the world. As Fed policy tightening takes hold, it might represent a further downside risk to global growth dynamics, if the US consumer steps back and others do not fill the void. Based on our framework, this supports the case for a stronger rather than weaker USD.

Don’t mess with the bull

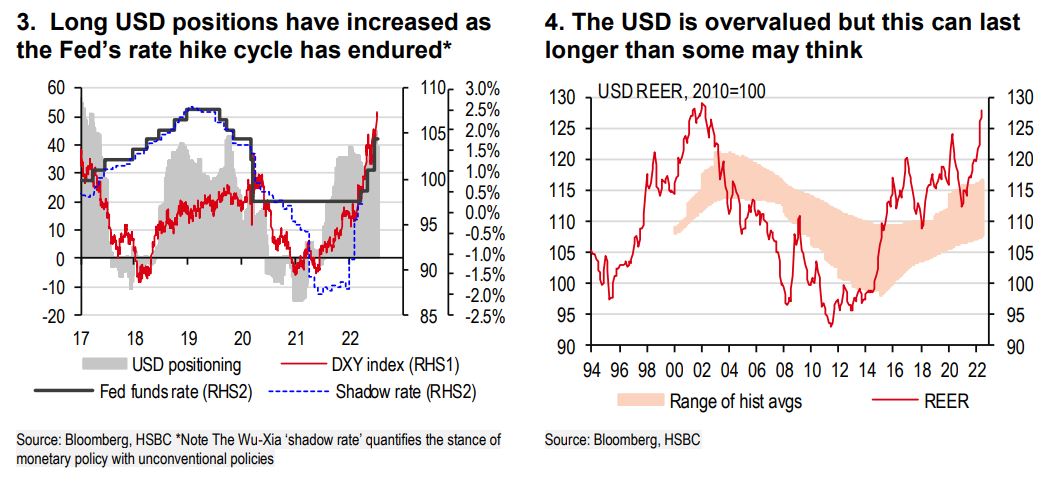

There are three other popular narratives to say the USD should go down: 1) USD long positioning is extended at a time when Fed hikes may be fully priced in; 2) the USD is overvalued; and 3) foreign demand for US equities will slow sharply. There is some truth to these points, although there are important nuances. The short-term positioning does appear to being long USD but a Fed pause or even possible cuts does not always mean it should weaken. For instance, the USD was resilient after the end of the Fed’s last tightening cycle in December 2018 and that strength persisted even when rate cuts started. Critically, much depends on what is happening elsewhere, which is core to our current thinking.

As for valuation, we also agree that the USD is overvalued. On some measures, it is back to the expensive levels of the early 2000s (Chart 4). The drivers of such a deviation from ‘fair value’ are very different between now and then. For the latter, broad USD strength was a function of large capital inflows amid the tech bubble. That is not the case this time round. It is also worth bearing in mind that the USD’s overvaluation persisted for around two years in the early 2000s. The point being a currency’s overvaluation may be a warning sign that a correction could eventually occur but there is no obvious near-term signal.

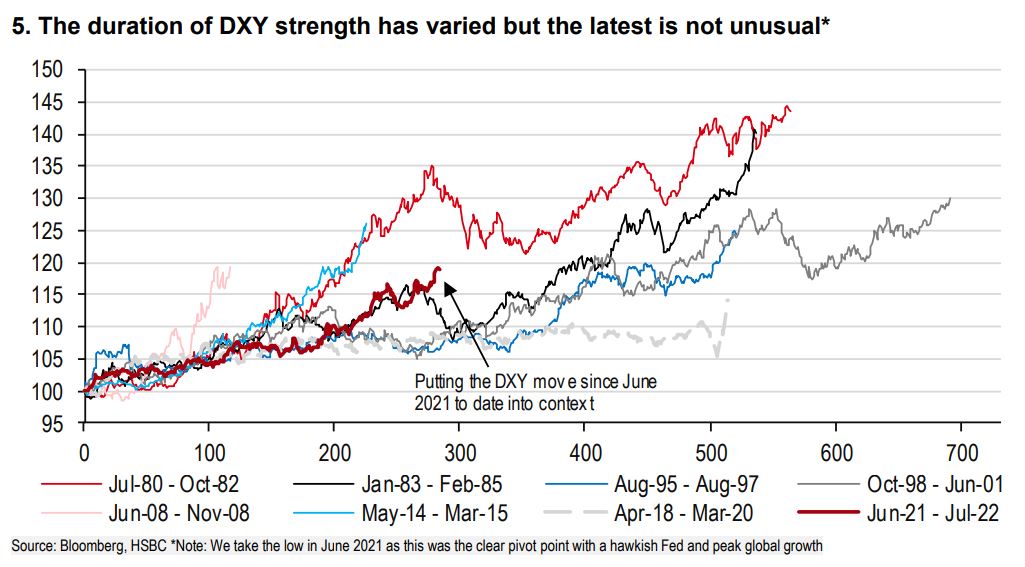

This is also highlighted by the duration of some of the USD bullish trends over the past few decades (Chart 5). The current trend may seem lengthy but it is not historically.

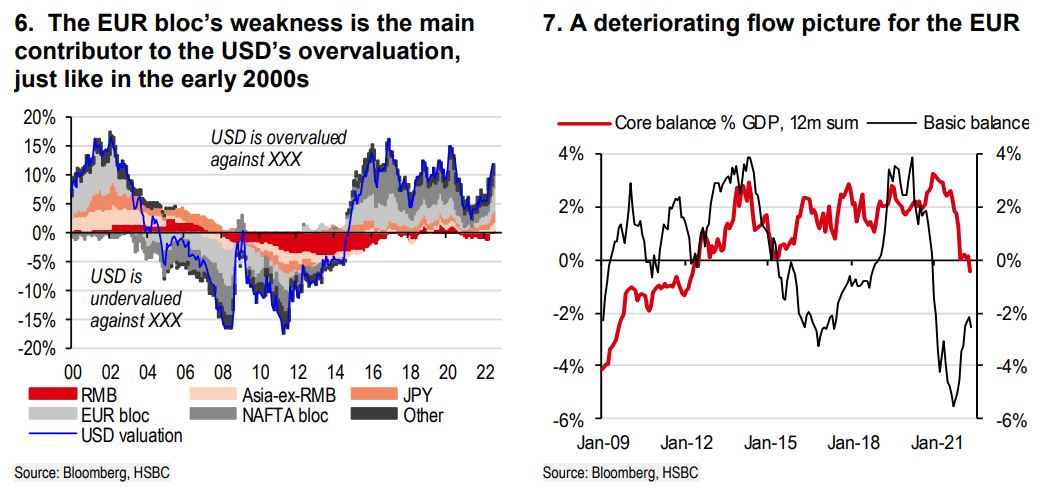

An important observation is how the USD’s recent overvaluation is more in response to European currency weakness, although not to the same magnitude as in 2000 (Chart 6). Back then the EUR fell to a record low (0.82 in October 2000) and, the Eurozone was running at basic balance deficit of 12.5% of GDP. The region’s current account deficit was nearly 6% of GDP while the combination of net portfolio and FDI outflows were 6.5% of GDP. This is historically very large. It is unclear whether such a large net outflow will occur this year but the signs have not been upbeat (Chart 7). The current account is deteriorating given a slower export cycle and higher import costs associated from the ongoing war between Russia and Ukraine. For example, in the 12 months ending April this year, the Eurozone’s current account surplus has declined from EUR312bn to EUR182bn. This could get worse.

Not a bull market

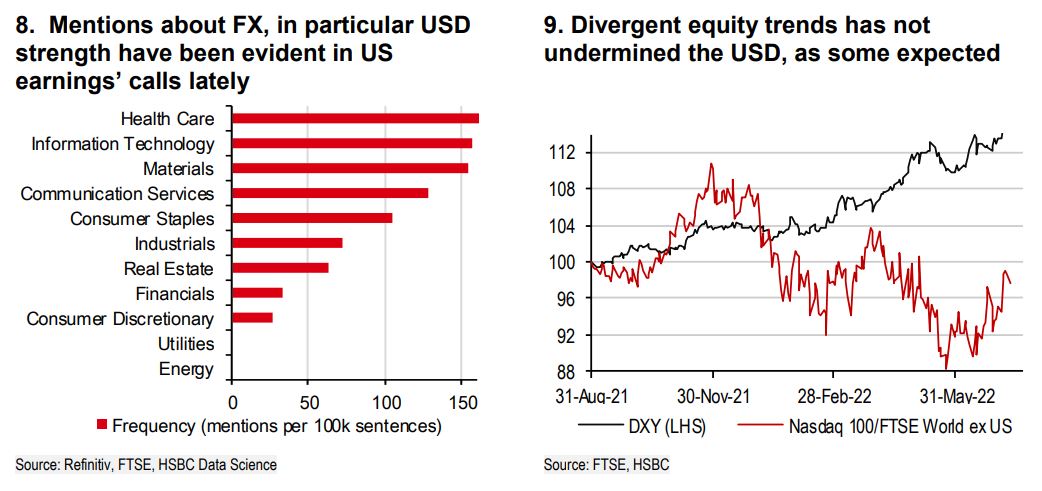

Despite the flow support to the EUR and other currencies looking less supportive, there is an ongoing discussion how the USD’s resilience is creating problems. The impact on US earnings’ is noticeable, especially for US health and technology companies (Chart 8, see Data Matters: The circle of strife, 5 July 2022). This probably helps to explain why foreign demand for US equities slowed. The latest US balance of payments data show that through Q4 2021 to end Q1 2022 foreigners sold over USD400bn of US equities. This is an eye-watering amount. One would think that this would have dented the USD but as we know, this did not happen. The weakness of US growth equities relative to other equity market and the USD has not been a strong relationship (Chart 9). An explanation comes down to foreigners’ demand for US debt being a potent offsetting factor, purchasing nearly USD600bn in the same period.

Conclusion – hold the bull by its horns

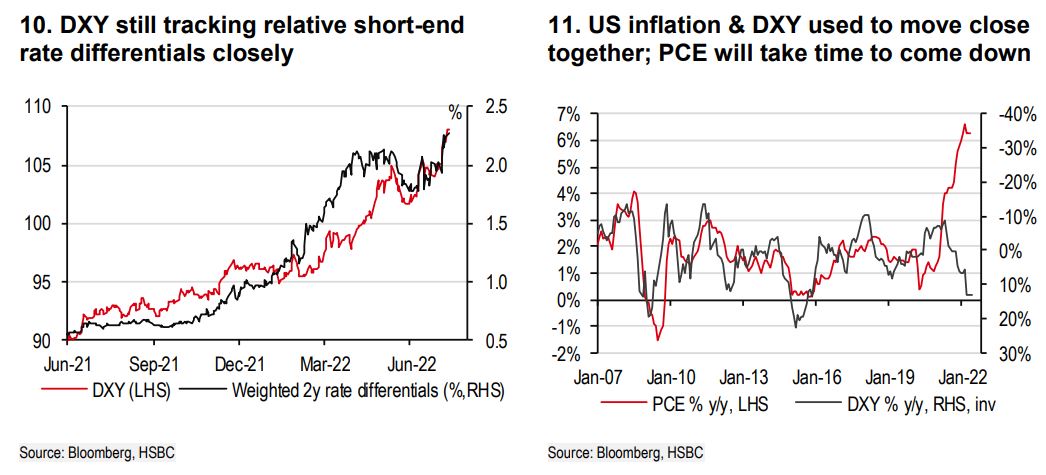

There has been a fixation with how the USD is poised to weaken. Positioning is not favourable, the USD is deemed to be expensive and its resilience is impacting some US corporate sectors negatively. We understand all of these points. However, these are not persuasive enough for us to think differently for now. In fact, we are emboldened in believing the USD has more upside. There has been too much attention paid to the USD’s frailties but not enough to the increasing ones elsewhere, which are causing the USD to be overvalued. Global growth is slowing and the downside risks are intensifying, which is USD positive. To assume that a softer US growth outlook could challenge the USD is not definite if it dampens the global growth outlook. The USD’s yield advantage remains supportive but too much tightening is priced in for others (Chart 10). Plus, the Fed may be in no rush to cut rates when inflation could prove sticky and rate hikes for other currencies are likely to do even more harm than good (Chart 11). This USD bull run is not over yet (Table 1).

This is an especially amusing DXY bull market given the market hysteria surrounding the rise of CNY and commodities as new reserve currencies earlier this year. In my twenty-plus years in markets, I’ve yet to see a declaration of the end of DXY hegemony make anybody money.

I, too, see this bull market running further. All of the reasons cited by Citi fit into a base case of mild US recession. But the unusually high probability of a deeper recession risk case is the one that concerns me.

If a market shock is triggered by Fed tightening and the US consumer buckles, industry will liquidate the US goods inventory mountain. This will spill over into a major trade shock for already very weak Europe (on war and energy) and China (on property and OMICRON).

The tearaway DXY of the past few weeks is a signal that this risk case is rising.

In particular, with the Chinese property adjustment turning nuclear meltdown, the possibility of a feedback loop of doom forming around a falling CNY and commodities versus a rising DXY is intensifying.

The AUD can sink deep into the 50s if such non-linear events transpire.

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed. Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website. Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.