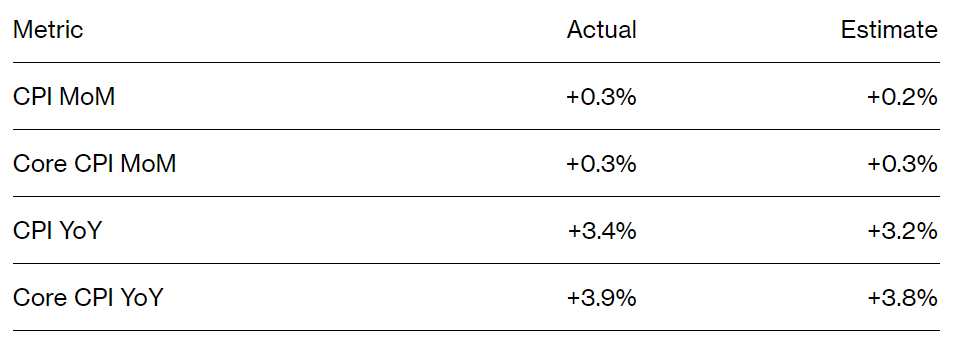

Much of the surprise in so-called core goods, which excludes energy and food, came from pickups in prices for used cars and apparel, despite year-end promotional activity. Services prices also held firm, notably within costs for housing and car insurance, which rose the most on an annual basis since 1976.

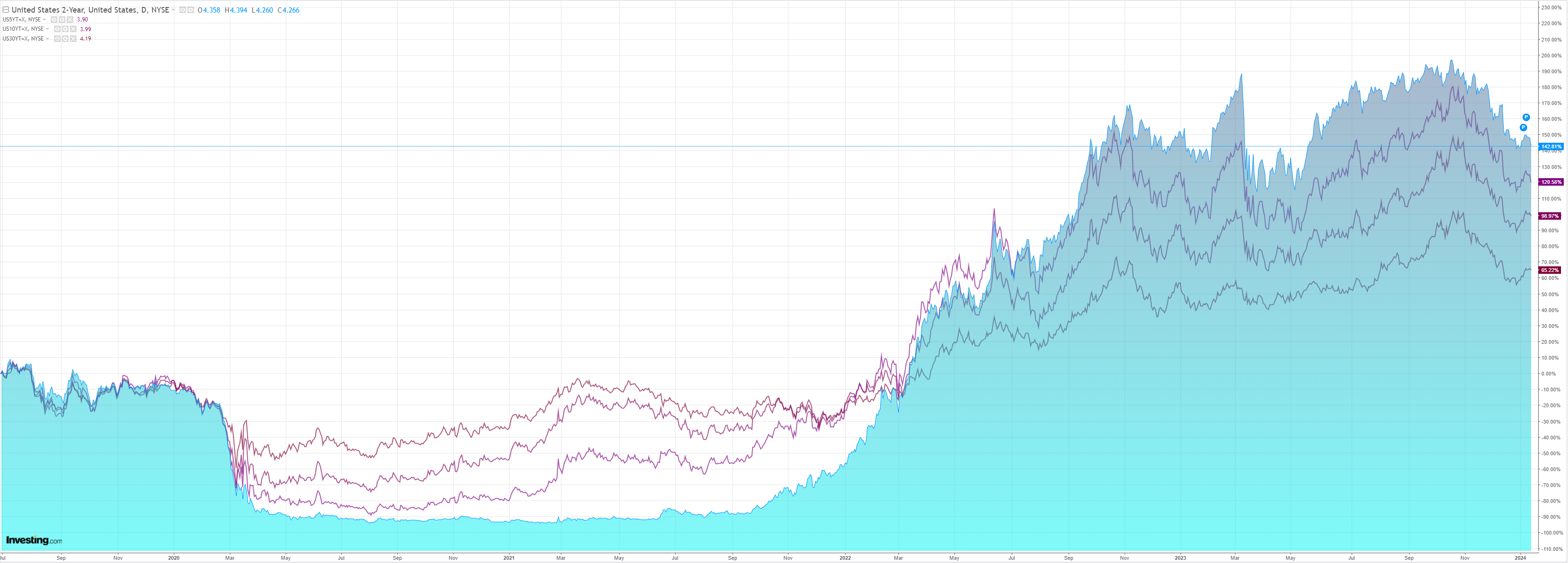

I expect housing and energy costs to keep falling, so I am not concerned yet.

The risk is that either the easing FCI overexcites the consumer and/or energy prices spike on geopolitics. To wit:

Iran captured an oil tanker off the coast of Oman, heightening tensions in the world’s most important trade lane for global crude supply.

It seized the St Nikolas “in retaliation for the theft of oil by the US,” Iran’s semi-official Mehr reported. The ship was previously known as the Suez Rajan, which was involved in a high profile American sanctions bust-up that ultimately led to the removal of 1 million barrels of Iranian oil.

These are precisely the kinds of provocations we can expect to continue. Iran does itself a favour by lifting the oil price, so long as it does not push too hard and bring the US military to bear.

That is still a tail risk, so Iran’s hijinx should lose impact over time.

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed. Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website. Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.