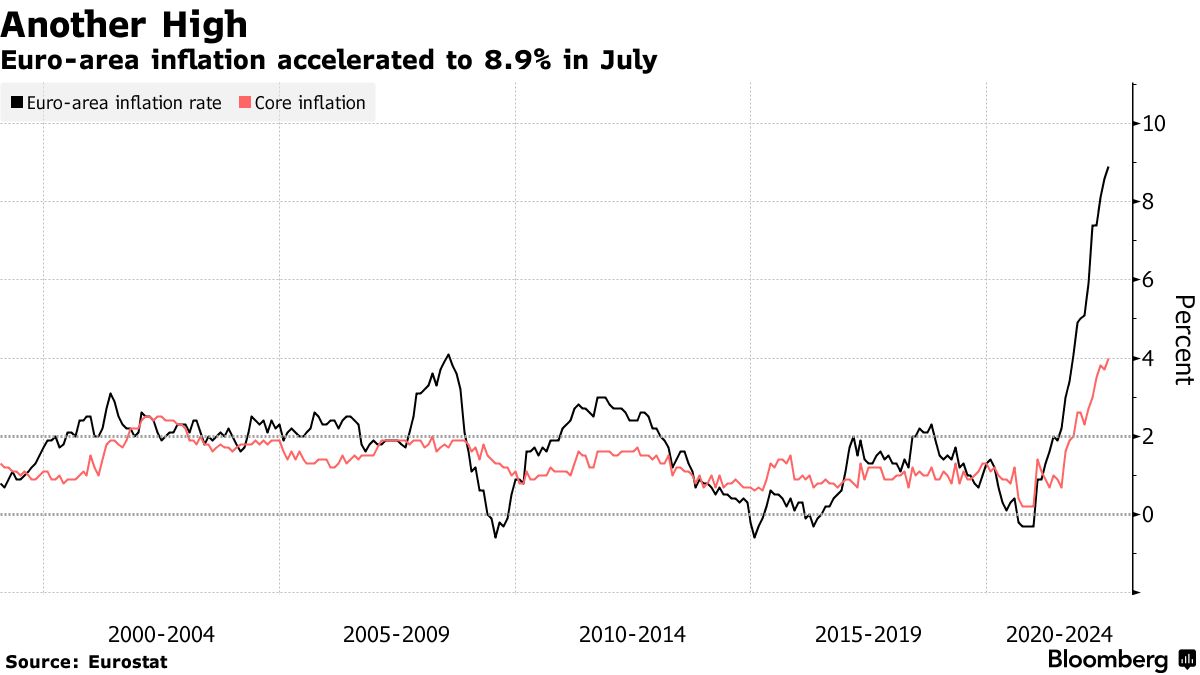

Friday evening printed two nasty inflation outcomes. Europe is still getting worse:

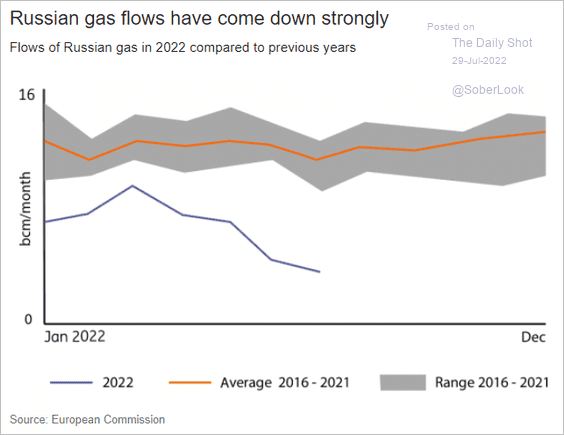

With winter approaching, markets really need to ask if they want to bet on Vladimir Putin’s generosity:

Given his supply to Europe is already stuffed long-term why wouldn’t he go for a little scorched earth on the way out? Surely this makes EUR investable.

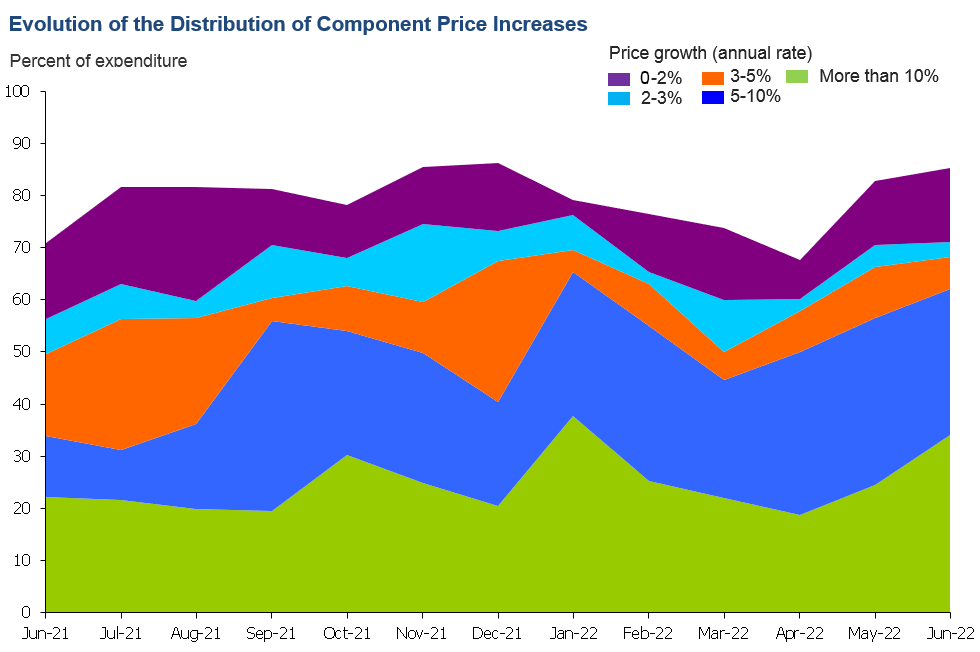

Second, the Fed’s preferred inflation measure, PCE, came in much stronger than expected. Goldman:

The June core PCE price index rose by 0.59% month-over-month, above consensus expectations, and the year-over-year rate increased to 4.79%. Personal income and spending both increased a bit more than expected, and the saving rate dropped to 5.1% in June. The Employment Cost Index rose 1.3% in Q2(not annualized), with firm underlying details. Our composition-corrected wage tracker stands at +5.5% year-over-year in Q2 (vs. +5.4% in Q1), and our quarterly annualized composition-corrected wage tracker based on average hourly earnings and the Employment Cost Index stands at +5.3% in Q2 (vs. +5.6% in Q1).

The notion that the Fed is about to pivot strongly and reflate everything with oil above $100 and PCE still rising strikes me as wishful thinking.

The Fed turned data dependent this week and the data is unequivocal. Its job is not done.

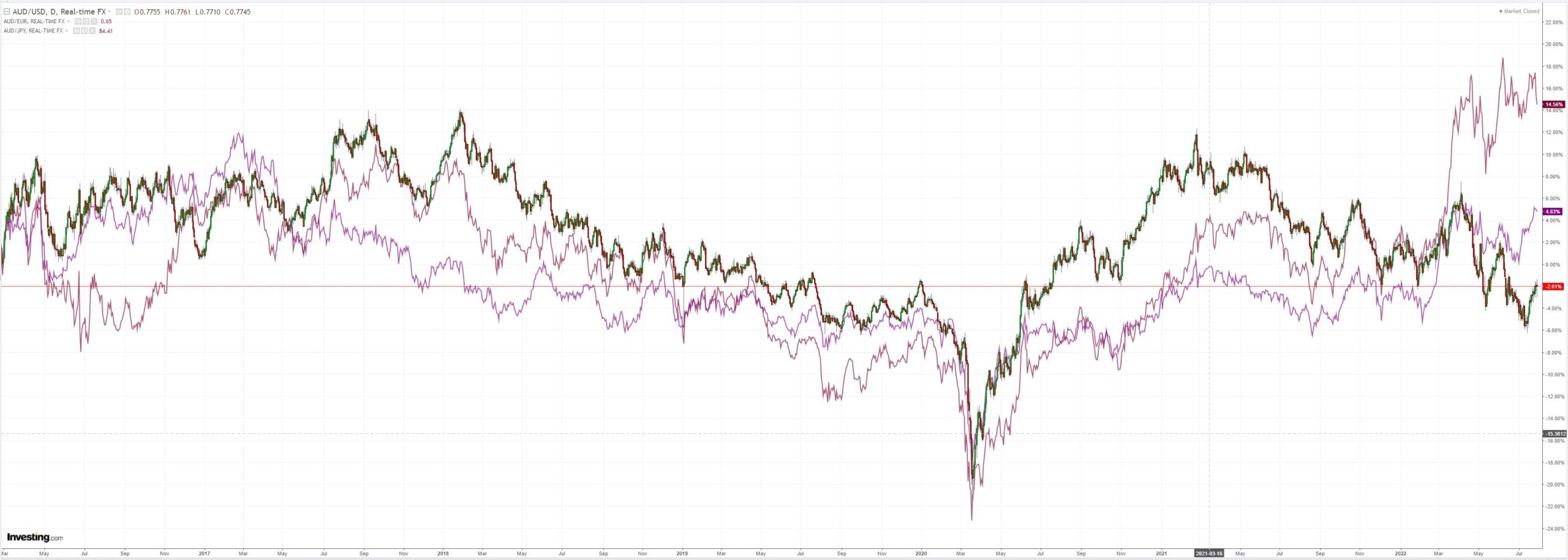

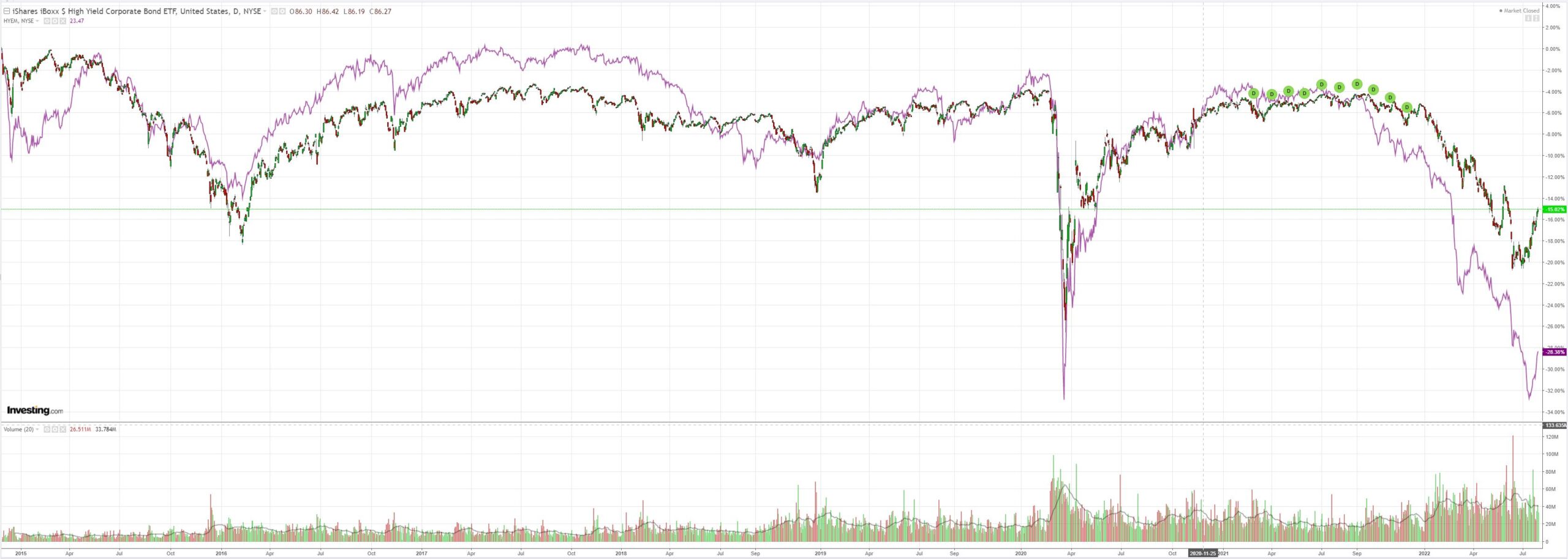

The AUD short squeeze has been fueled by falling yields. Beware.

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed. Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website. Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.