The Dallas Fed manufacturing survey index disappointed at 8.7 (est. 11.0, prior 14.0), with a notable slide in the six-month ahead expectation measure to 8.2 from 20.6.

US President Biden announced his Administration’s proposal for a USD5.8trn Budget, with increased defence and domestic spending, although these proposals tend be watered down eventually.

Event Outlook

Aust: Our Westpac Card Tracker indicates retail salesshould post a relatively strong gain in February with QLD and NSW flooding events only being a slight offset (Westpac f/c: 1.5%). The boost to national income should aid the 2022/23 Federal Budget’s focus in supporting the supply-side of Australia’s economic recovery (Westpac f/c: -$76.9bn).

UK: Net mortgage lendingshould soften over the course of the year as rates continue to rise (market f/c: £5.4bn).

US: January’s FHFA house pricesand S&P/CS home price index are expected to robust monthly gains given the strength of demand and softness in supply (market f/c: 1.3% and 1.5% respectively). Inflation concerns are likely to continue weighing on consumer confidencein March (market f/c: 107). Meanwhile, February’s JOLTS job openingsshould continue to point towards extraordinary demand for workers (market f/c: 11000k). The FOMC’s Harker is due to speak on the economic outlook.

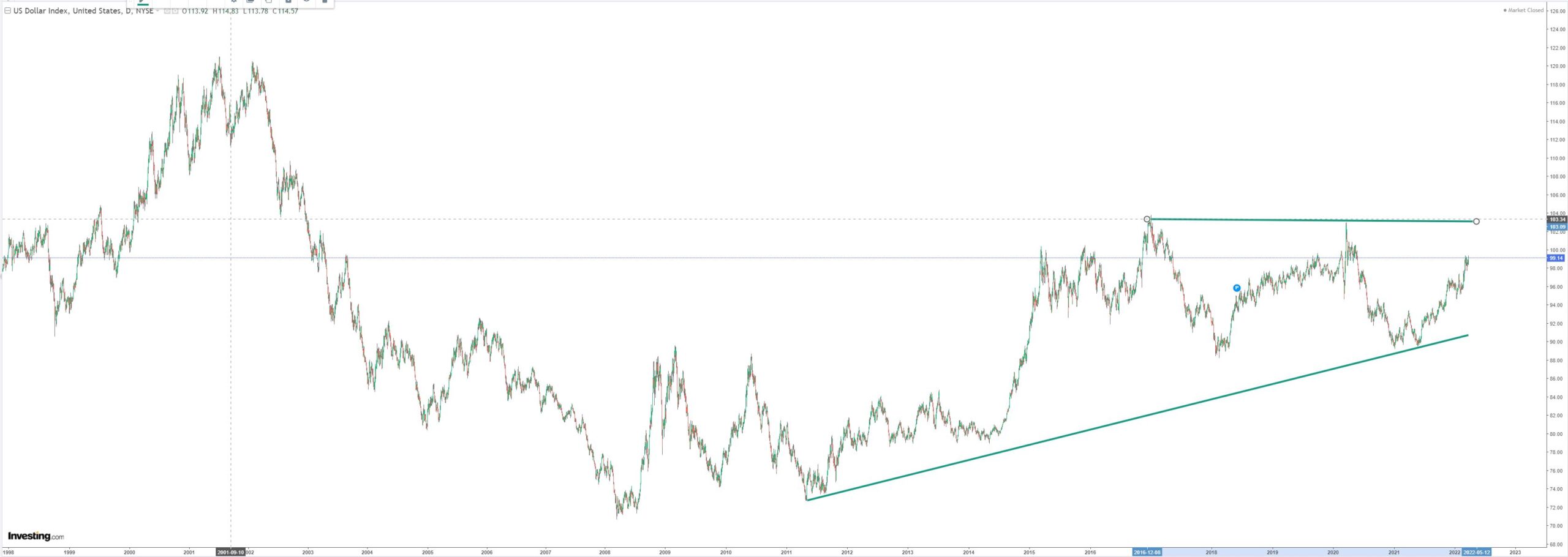

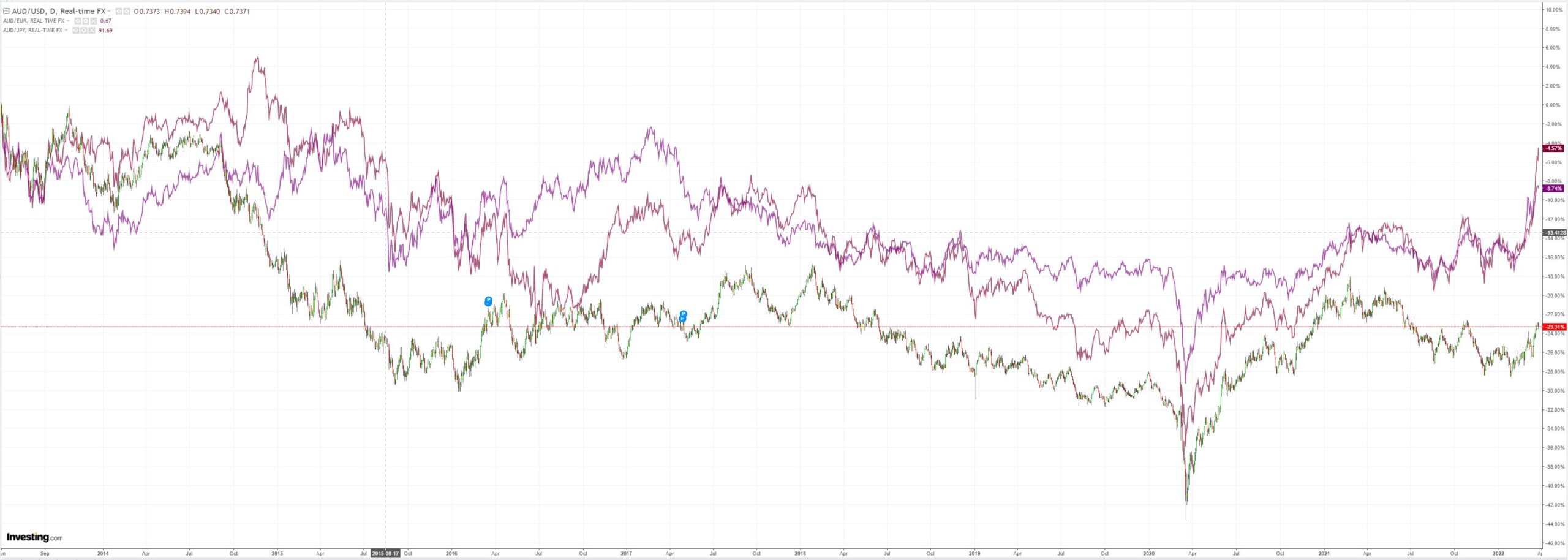

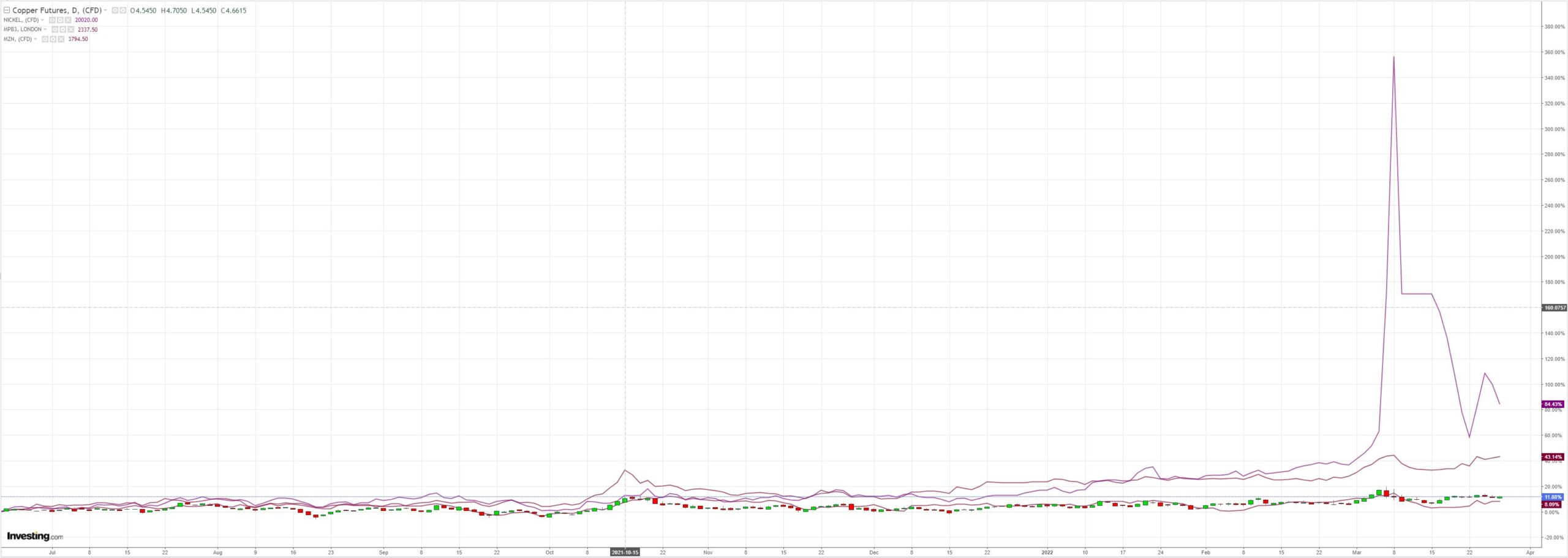

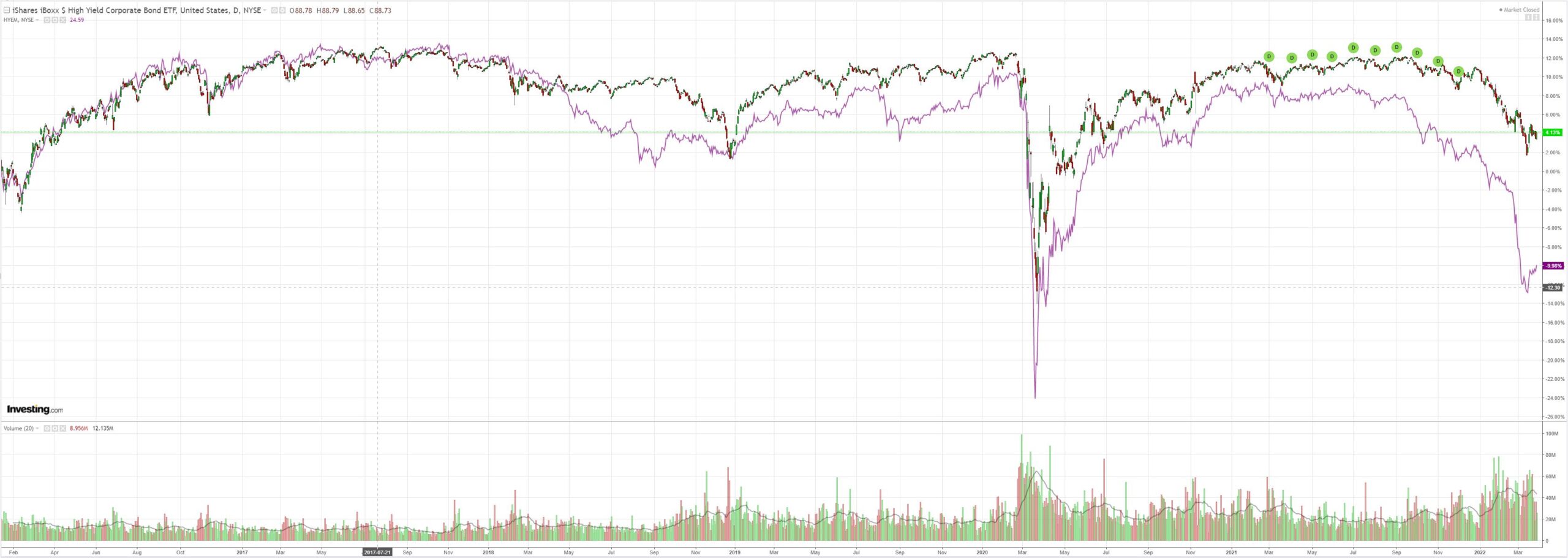

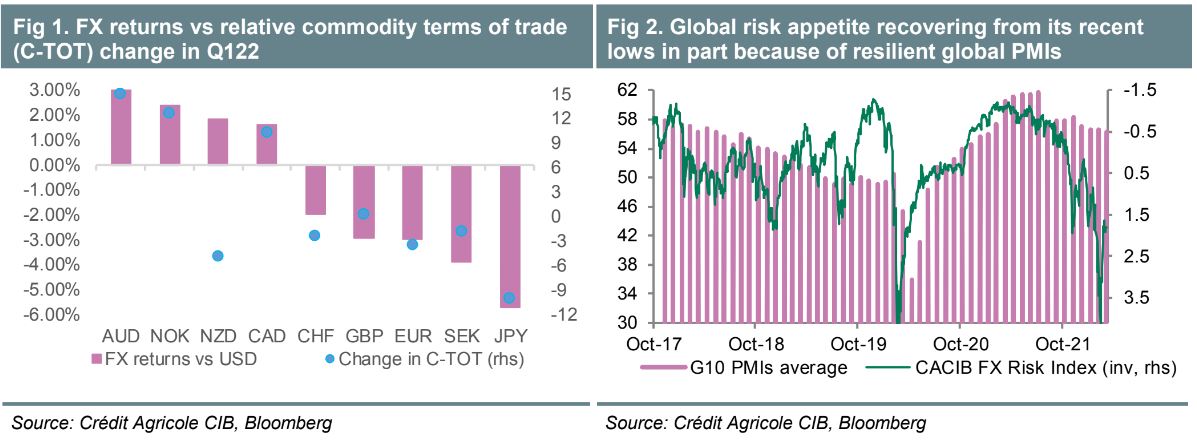

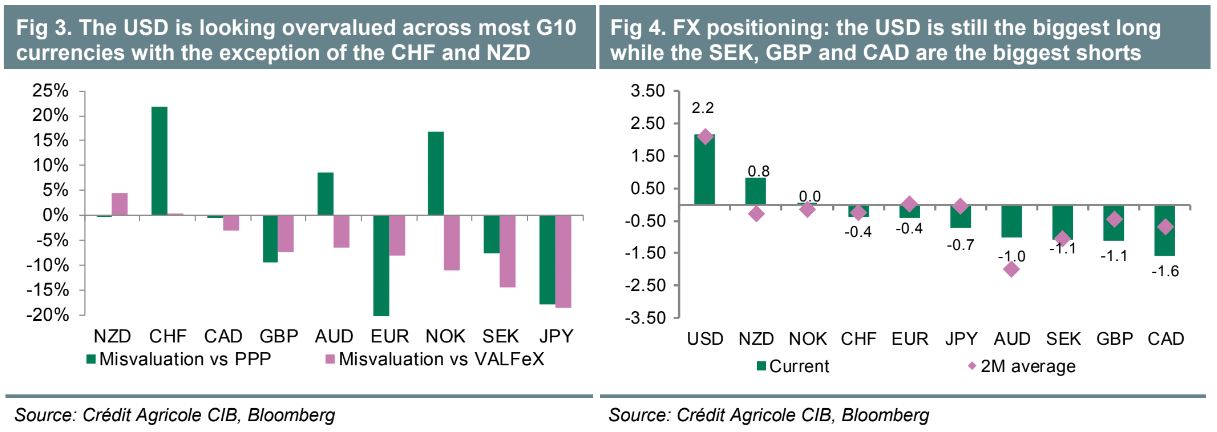

A key question ahead is whether ‘C-TOT’ can remain a dominant FX market driver or if ‘RoRo’ and the ‘USD smile’ will stage a return. With commodity prices likely to remain very elevated for now and with market risk sentiment having recovered of late (Figure 2)–potentially because investors believe that the global recovery will continue despite the above risks–a carry-over of the dominant Q1theme into Q2 should see G10 commodity currencies outperforming while the likes of the JPY and the EUR could remain on the defensive in the near term.The ‘RoRo’ and in particular the ‘USD smile’ market themes may stage a comeback, however, especially if the risk appetite that fuels demand for high-yielding USD proxies at present wanes in Q222. Among the triggers of a potential renewed risk aversion spike will be a more protracted conflict in Ukraine, worsening energy and food crises as well as tighter global financial conditions on the back of even more hawkish central banks. The developments could take their toll on global economic sentiment and risk appetite and support the safe-haven USD.Given the limited exposure of the US economy to the above headwinds and the hawkish Fed, the reign of the high-yielding, safe-haven King USD can resume in Q2. As in Q1, however, FX overvaluation and an overhang of market longs may limit any USD outperformance (Figures3 and 4).

PMIs were supported by supply-side backlogs and prices but demand was weakening fast. Equities always pretend there’s a soft-landing coming when the Fed tightens. There never is and this cycle is much more precipitous.

My base case remains the Fed breaks something in due course, DXY roars and AUD busts as equities realise a profits recession is coming in 22/23.

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed. Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website. Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.