Consumer inflation continued to surge in December, in line with consensus expectations.

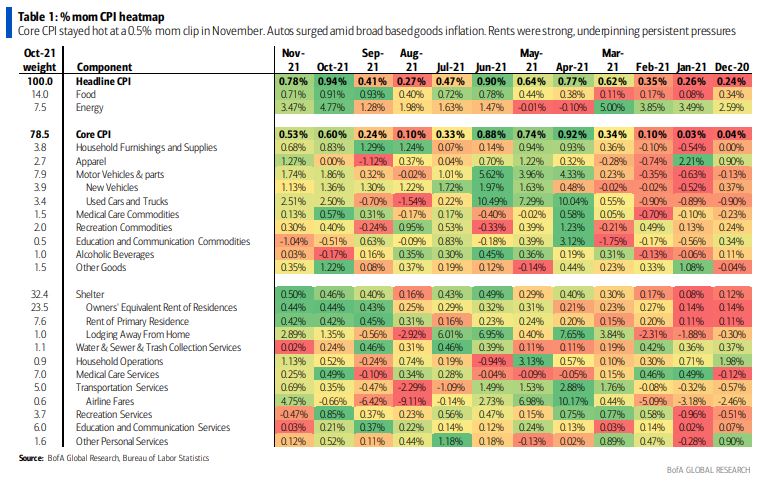

The core CPI rose by 0.55% mom, which boosted the yoy rate to 5.45% from 4.93%— the highest since 1991. Headline CPI was up 0.47% mom as energy prices dropped by 0.4% mom and food rose 0.5% mom. Headline % yoy increased to 7.04% from 6.81%— the highest since 1982.

Core goods were up 0.9% mom and 10.7% yoy. Once more the largest contribution (15bp) was from used cars, which surged 3.5% mom. Supply issues continue in the auto sector, and wholesale prices suggest further upside in used car prices in the months ahead. Outside of autos, core goods components broadly gained as apparel jumped another 1.7% and household furnishings/supplies rose 1.3% mom. Meanwhile education/communication commodities slipped for the third consecutive month, this time by 0.4%. We think the breadth of gains in goods reflects both global supply chain disruptions and the pull-forward in the holiday shopping season, which meant earlier discounting in October.

However, as we have argued repeatedly in recent months, the surge in inflation is not just due to Covid and other distortions. There is a strong underlying cyclical pickup in prices as well, which is most evident in OER and rent of primary residence. Both series increased 0.4% mom for the fourth consecutive month. Travel components were also very strong despite the winter Covid surge. Lodging rose by 1.2% mom and airline fares soared 2.7% mom. Given the timing of the Omicron wave, however, its impact might be reflected more strongly in January prices. Broader transportation services fell by 0.3% mom. This was a smaller drop than expected given unfavorable seasonal factors. Outside of that, services components were mixed. Recreation fell -0.1% mom, education / communication was up 0.1% mom and other personal services popped 0.7% mom. Medical care services grew 0.3% mom.

Overall, the breadth of the inflation supports our call for four Fed hikes this year, along with the start of quantitative tightening. Core inflation is likely to peak in March 2022, after which the yoy comparisons will turn highly unfavorable. But the key question is where core inflation lands in the medium term. And increasingly the risks are that it will land closer to 3% than the Fed’s 2% target.

The rates market generally looked through the close to consensus print. The nominal curve flattened slightly, inflation breakevens were 2-3 bps lower and real rates 1-2 bps higher. The modest declines in inflation breakevens across much of the curve suggest that the persistent components of the print may not have been as strong as feared, though overall the print still endorses a sooner and more aggressive Fed policy response.

The data point for the night was weak Chinese inflation and credit.

Yet DXY was smashed. Partly this is stretched positioning. But one can’t help observing that these moves are precisely what I expect to come later this year as the Fed overdoes it while China keeps up the stimmies.

Are markets already looking through Fed tightening to the economic sag afterward for the US, while looking through the Chinese economic sag to a hopeful boom afterward?

Given that paradigm only drives more inflation via commodities it guarantees that the Fed will have to go even further and risk crushing the cycle to end the stagflation lunacy that has grabbed markets.

God knows, nothing would surprise me anymore!

Australian dollar roars as mighty greenback crumbles

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed. Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website. Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.