We need to pan out today to get the full grasp of what’s happening. DXY is on a historic tear:

AUD appears to be rolling into a historic bust reminiscent of previous Chinese busts:

Oil is now officially deflationary, down year on year:

I hope nobody bought Goldman’s commodities drivel:

Big miners have all broken support. Short-term iron ore stability is keeping it orderly but if you think that will last then I’ve got a bridge I will sell you:

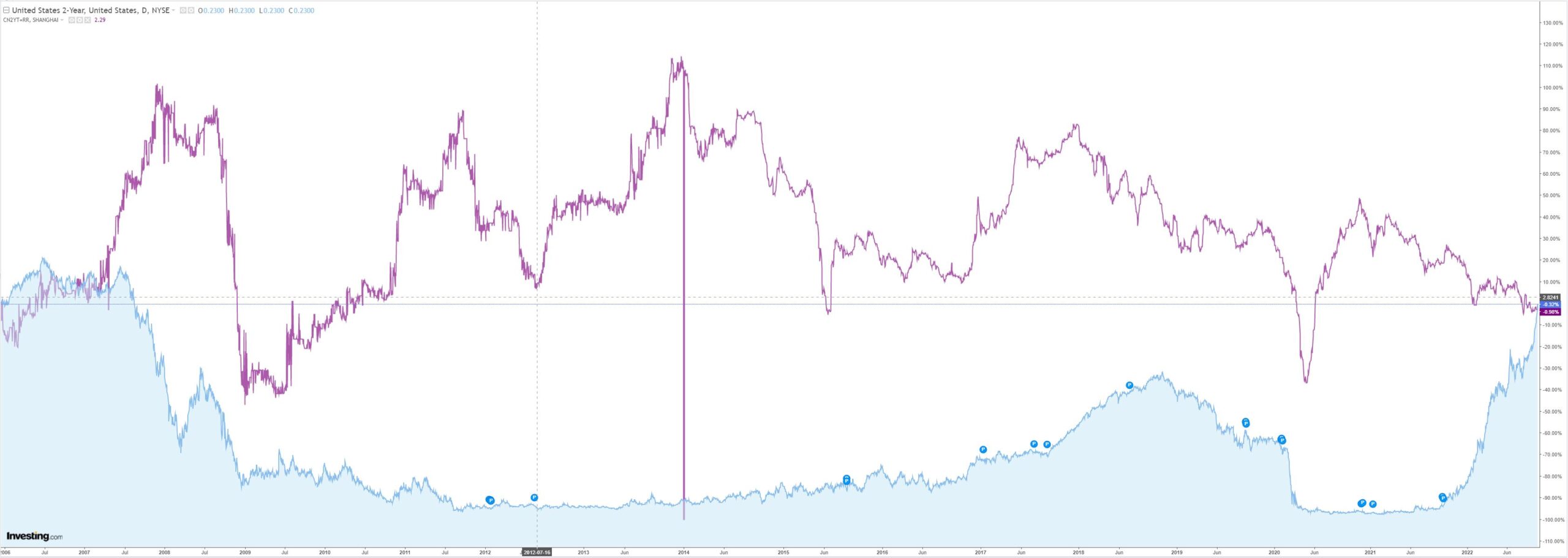

CNY is also at historic support. There are signs China will try to hold it there with the PBoC imposing new reserve ratio requirments for FX yesterday.

The risk is they can’t hold it. The entire post-WTO rise of CNY was premised on the Chinese economy transitioning from eternally-led to internally-led growth. That dream turned out to be little more than the greatest property ponzi scheme in the history of the world.

We should all feel quite privileged to have seen it. It will never happen again.

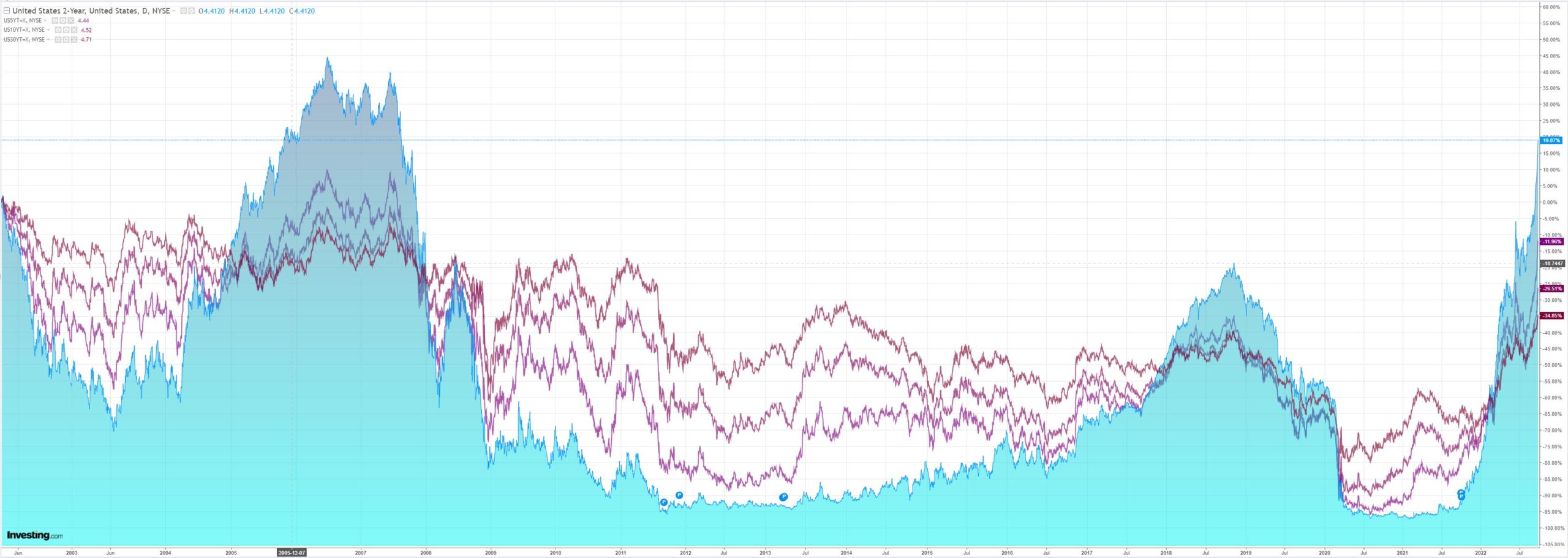

But, it is over, and that means China can no longer support levels of interest rates so far above the DM economies it was stealing production from. Whether at the short end of the curve or the long:

Pantheon sees China trying to slow the CNY crash:

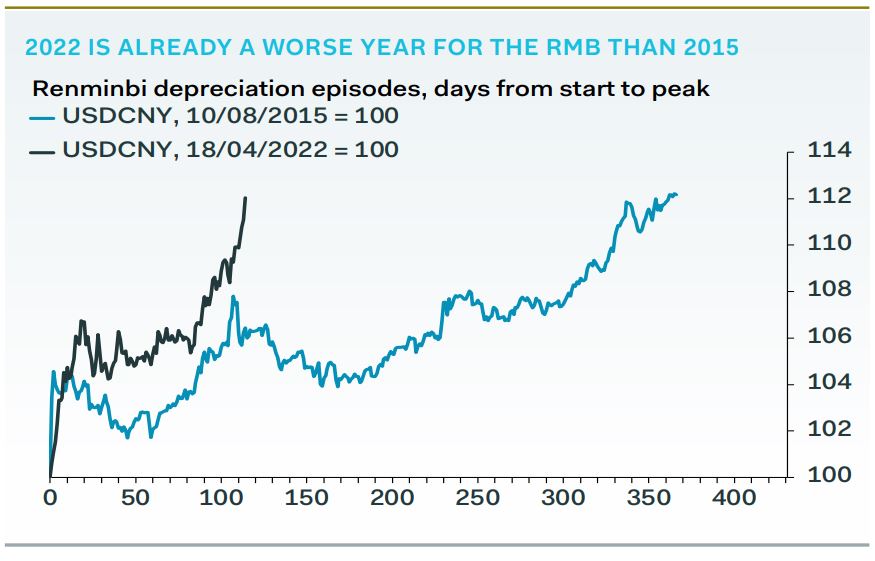

Pressure continues to build on the renminbi, which hit 7.16 on Monday and the PBoC is clearly worried. The central bank announced a hike in the risk reserve ratio for FX forwards to 20%, from 0% currently, a move which is estimated to increase the cost of forward dollar buying by over 500bp.

The currency’s performance is in line with broad dollar strength, and roughly in keeping with widening interest rate differentials. But the risk for the PBoC is that large drops in the RMB may trigger capital flight, as in 2015, sparking a self-perpetuating spiral which imperils the domestic financial system; state banks have reportedly already been ordered to buy domestic equities, amidst a market sell-off.

A currency doom-loop was already a worry, even before the latest plunge in the currency, with the sharp depreciation earlier this year preceding several months of declines in China’s FX reserves, despite sizeable trade surpluses. The spiral may already be upon us. Given its financial system is already weakened by the ongoing property crisis, this is arguably a bigger problem for China than elsewhere.

One risk to dismiss, however, is a coup ousting President Xi. Rumours flew over the weekend, but appear to have stemmed from a single Twitter (NYSE:TWTR) account which backed the claim with a video of military vehicles on a road, and later fabricated air traffic maps. We will eat this Monitor if the rumours are true.

I remain skeptical that we will see a meaningful turn in the property market after the National Congress (though that is a risk if they throw the kitchen sink). Moreover, neither has China meaningfully cut its policy rates even as property starts sink like Japan in 1989. More cuts are surely ahead.

Finally, how can the looming G20 meeting cook up a solution to this given the obvious trade implications alongside already worsening geopolitical relationships? Happy coordination between nations seems a thing of the globalisation past.

So, I still think the base case for CNY is lower and, as such, underneath the great post-pandemic inflation scare is a deflationary dragon waking in China that has only begun to disgorge price destruction.

Most obviously in its path (ironically given the DM inflation scare) are commodities and the AUD.

Australian dollar nose dives into firey Chinese hell

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed. Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website. Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.