The big data release of the night was US jobs of course. TD has the wrap:

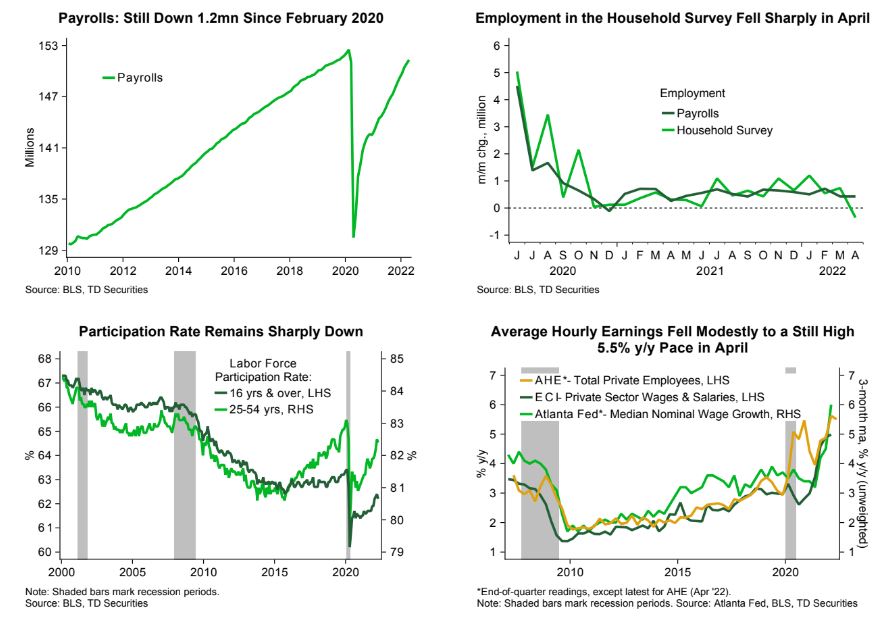

Payrolls rose a robust 428k in April, above the 380k consensus but closer to our slightly more optimistic 400k forecast. The unemployment rate stayed unchanged at 3.6%, as a result of the large decline in the employment series from the household survey combined with a retreat in the participation rate. Average hourly earnings slowed to 0.3% m/m after posting a solid 0.5% m/m advance in March.

•The April report continues to support the view that the labor market remains very solid, but that it is slowing at the margin. We think today’s report supports the Fed’s inclination to front-load interest rate hikes until it reaches a more neutral stance.

We expect the Committee to increase rates by 50bp in both June and July,and to deliver a 25bp hike at each meeting between September and March 2023.

You can expect that all you want, but I suspect markets will have long ago priced a recession before the Fed gets that far.

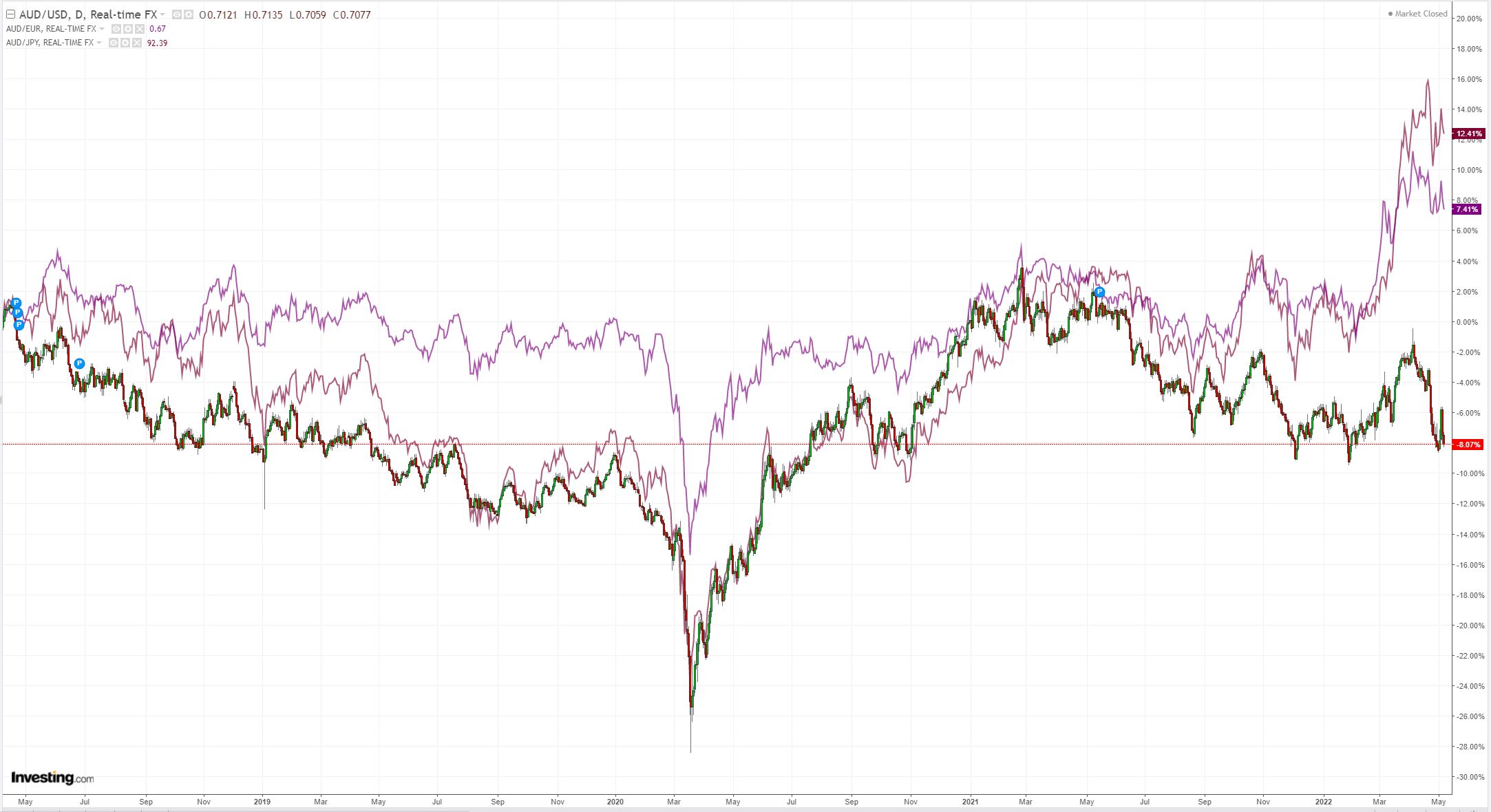

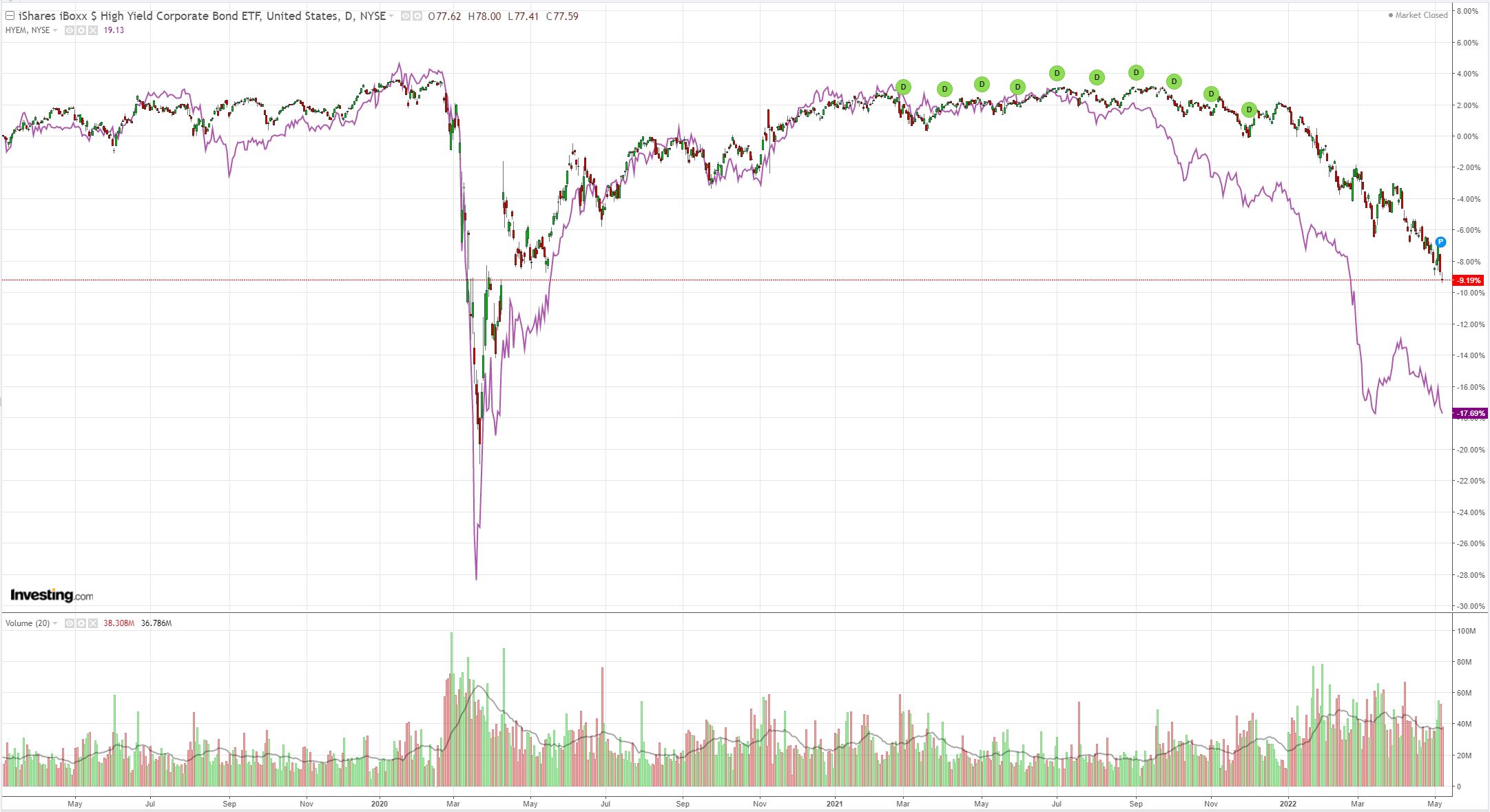

In the financialised economy, asset prices rule everything and the most important to US households is stock prices. As Fed hikes gut the stock market, the consumer will retrench and excess US inventories become a big problem for the supply side of the economy.

The subsequent drawdown will send a trade shock to Europe where domestic demand is already on its knees, and to China where domestic demand is curled up in a little ball under the bed.

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed. Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website. Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.