US private sector payrolls (ADP (NASDAQ:ADP)) disappointed with a 128k gain in May (vs 300k expected, April revised lower from 247k to 202k). The services sector was the strongest with a still modest 104k increase. Factory orders in April rose 0.3% (est. +0.7%, prior revised from 2.2% to 1.8%).

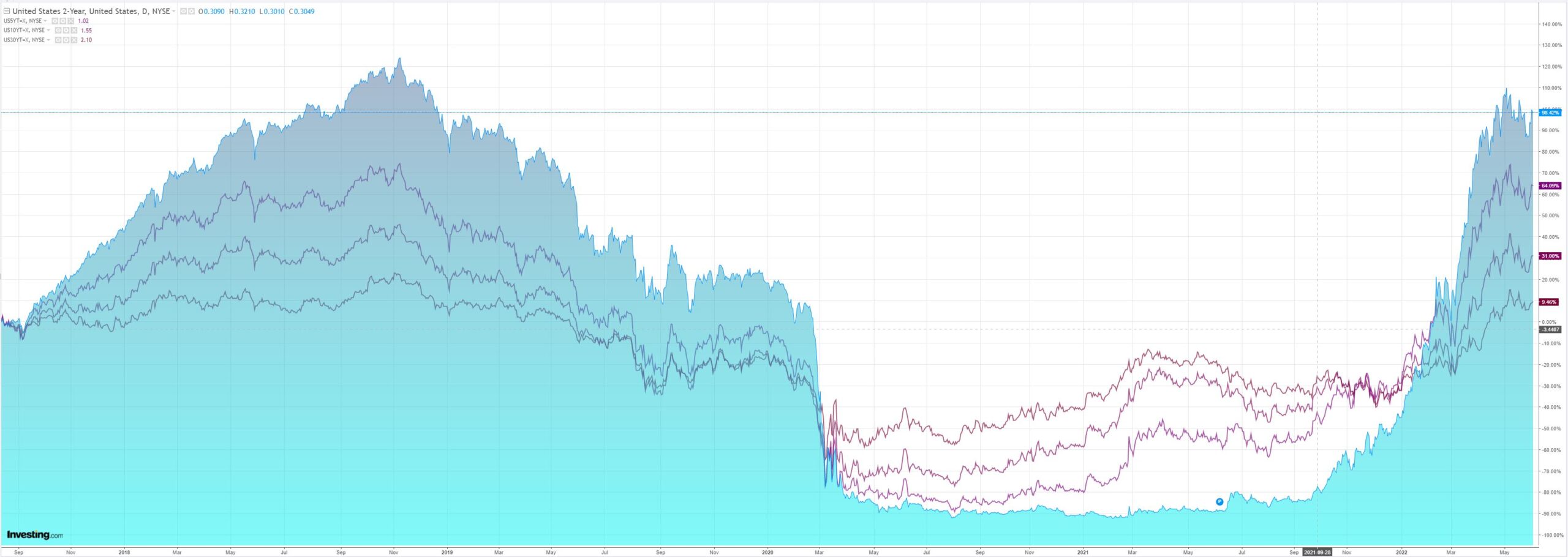

FOMC vice-chair Brainard does not expect a pause in September, adding that market pricing for 50bp hikes in June and July seems reasonable. Mester also supports 50bp hikes in June and July, but added it is not clear what will happen in September. If there is “compelling evidence that inflation is moving down, then the pace of rate increases could slow…but if inflation has failed to moderate, then a faster pace” could be needed. She said it is too soon to say that inflation has peaked, and that recession risks have increased but it is still likely that a downturn can be avoided.

Event Outlook

Aust: Housing finance approvalsare set to fall in April given the housing cycle has now peaked and market turnover has sharply declined (Westpac f/c: -3.0%); owner-occupiers are expected to be hit harder than investor loans for the month (Westpac f/c: -3.5% and -2.0% respectively).

NZ: Strength in residential construction activity should continue to support building work in Q1 although capacity constraints are limiting the gains (Westpac f/c: 2.0%).

Japan: The final estimate of the May S&P Global (NYSE:SPGI) services PMI is due.

Eur: Retail salesare expected to post a muted lift in April with inflation and conflict limiting the full rebound in consumer spending (market f/c: 0.2%). The final estimate of the May S&P Global services PMI is also due (market f/c: 56.3).

US: Non-farm payrollsshould continue to reflect healthy gains in employment growth in May (Westpac f/c: 370k; market f/c: 323k) pushing the unemployment rateto its likely low for the cycle (Westpac and market f/c: 3.5%). The historically tight labour market should continue to support robust growth in average hourly earnings(Westpac f/c: 0.3%). Meanwhile, the S&P Global and ISM non-manufacturing PMIwill likely reflect a healthy services sector in May (market f/c: 53.5 and 56.5 respectively).

The key event was this:

Private sector employment increased by 128,000 jobs from April to May according to the May ADP® National Employment ReportTM.

Of course liberating the Fed to pause, hopefully.

There’s only one problem, the rally is so focused on commodities still that it is self-defeating for the Fed to stop.

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed. Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website. Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.