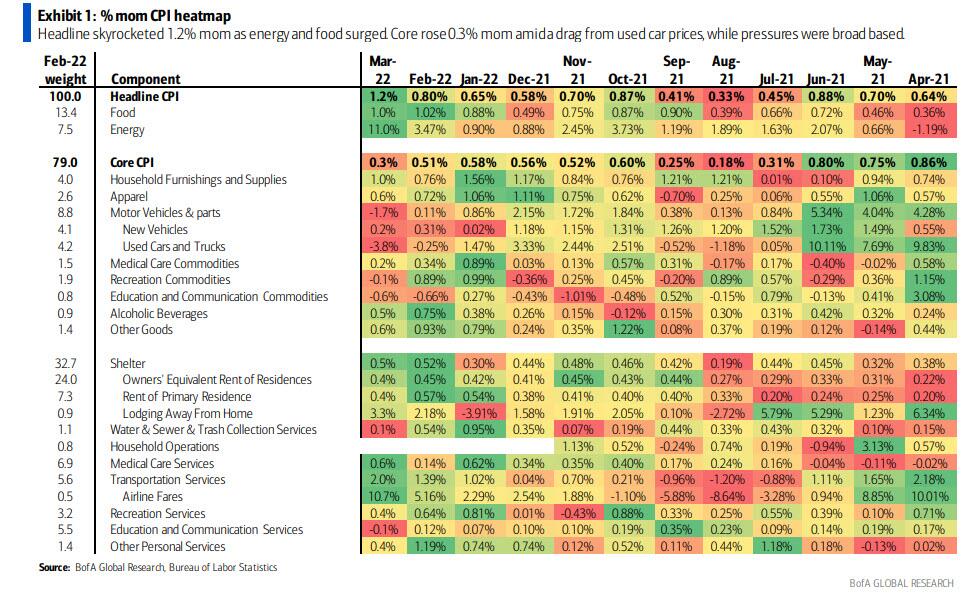

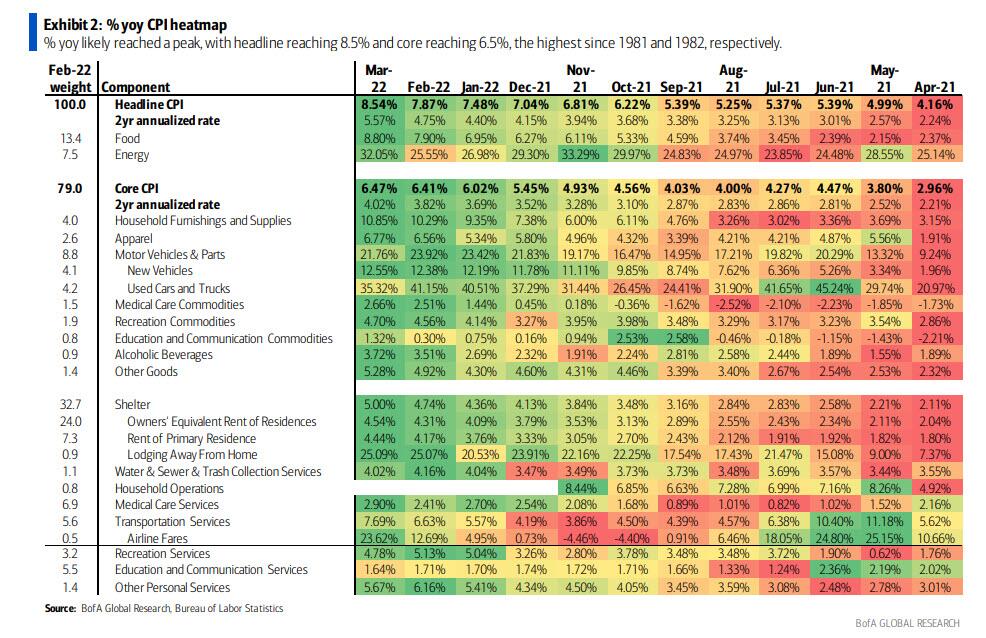

US CPI in March rose 1.2m/m as expected, 8.5%y/y (prior 7.9%y/y) – the highest annual rate since 1981. However, core inflation disappointed expectations, rising +0.3%m/m (est. +0.5%m/m) and 6.5%y/y (est. 6.6%y/y, prior 6.4%y/y). Details suggest that inflation may well have been peaked.

FOMC member Brainard reiterated that controlling inflation is the FOMC’s priority. She expects some tightening in financial conditions to help moderate demand, with easing in supply constraints as well, the combination helping bring inflation down. She welcomed the moderation in core goods prices in the March CPI report, but also warned not to put too much stock into one piece of data.

Germany’s ZEW survey posted a further decline, but less than markets had expected: current conditions fell to -30.8 (est. -35.0, prior -21.4) and expectations fell to -41.0 (est. -48.5, prior -39.3). Eurozone expectations fell to -43.0 from prior -38.7, current conditions fell to -28.5 from prior -21.9.

UK employment data for Feb. met expectations with unemployment at 3.8% (from 3.9%) and earnings growth at 4.0%y/y (from 3.8%y/y).

Event Outlook

Australia: The Westpac-MI Consumer SentimentApril update will be the first since the announcement of budget support measures although concerns around inflation and rising rates are still present.

NZ: Westpac expects the RBNZ to raise the Official Cash Rate by 25bps at the April meeting, although mounting inflation concerns raise a risk of a 50bp hike. Gains in grocery food prices should continue to buoy the food price indexin March (Westpac f/c: 0.5%).

Japan: Elevated commodity and transport costs are anticipated to squeeze machinery ordersin February (market f/c: -1.5%).

China: The trade surplusis expected to narrow in March as lockdowns in certain regions hinder exports (market f/c: US$21.7bn).

UK: Elevated energy prices should continue to lift consumer inflationin March (market f/c: 0.8%).

US: The PPIwill continue to be support by ongoing supply issues in March (market f/c: 1.1%). The FOMC’s Barkin is also due to speak.

Canada: Market expectations lean towards a 50bp hike at the Bank of Canada’sApril policy meeting, as inflation concerns continue to build.

US inflation is red hot but the second derivative is slowing. BofA:

The yoy rates for headline inflation both headed higher this month, with headline jumping to 8.5% (8.54% unrounded) from 7.9%and core increasing to 6.5% (6.47% unrounded) from 6.4%. We think that both reflect the peak for yoy rates but expect inflation to cool to hot levels by year-end, with headline at 6% 4Q/4Q and core at 5%4Q/4Q. For the Fed, it will likely look through some of the noisier components of the report—we recommend keeping an eye out for trimmed-mean later this morning—and conclude that price pressures remain elevated, underpinning the need to hike.

Treasuries rallied up to 10bps, and the curve steepened following the print. The decline in rates was roughly split between inflation break-evens and real rates, as the market priced both a fading in inflationary pressures and less aggressive Fed response. Today’s print is an inflection point, with core MoM inflation cooling to the lowest level since September’21. This shift may challenge TIPS demand, especially as we expect the Fed to begin balance sheet reduction in May. Market pricing for the Fed’s terminal rate declined about 10bps to 3.1% following the report, but fed funds futures through September declined less than 4bps. In general, the print still reflects very strong cyclical inflation components and should not deter the Fed from delivering on three 50bps rate hikes in coming meetings.

Get set for a deflationary bust that ultimately takes in commodities and AUD.

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed. Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website. Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.