US housing starts fell 4.1% in January (est. -0.4%), and building permits rose 0.7% (est. -7.2%). Completions are tracking below the path implied by permits due to resource shortages, although the data remains consistent with a robust path for the housing market in 2022. Weekly initial jobless claims rose to 248k (est. 218k, prior 225k), but continuing claims fell to 1593k (est. 1605k, prior 1619k). The Philadelphia Fed business survey fell from 23.2 to 16.0 (est. 20.0). – still an elevated level.

FOMC member Bullard continued to advocate for a front loaded policy response to inflation pressures, still favouring 100bp in rate hikes over H1, with balance sheet reductions commencing in Q2. He said forecast for temporary price pressures have proved incorrect and that there are risks that inflation will remain high. He added that a lot of policy normalisation has already been priced in.

Event Outlook

Japan: With the January CPIrelease expected to print at near pre-pandemic levels, the BOJ has started to indicate a focus on wages growth (market f/c: 0.6%yr).

Eur/UK: COVID-19 concerns should continue to weigh on European consumer confidence in February (market f/c: -8.0). Although omicron temporarily softened consumer spending in the UK, a rebound in retail salesis anticipated in January (market f/c: 1.2%).

US: Existing home salesare expected to fall in January with a lack of inventory hindering sales activity (market f/c: -1.3%). The January leading index should meanwhile reflect the US’ robust economic momentum (market f/c: 0.2%). The FOMC’s Evans and Waller will take part in a policy panel concerning the Fed’s new policy strategy. Mester and Williams will both discuss the economic outlook at different events. Brainard will speak on central bank digital currencies.

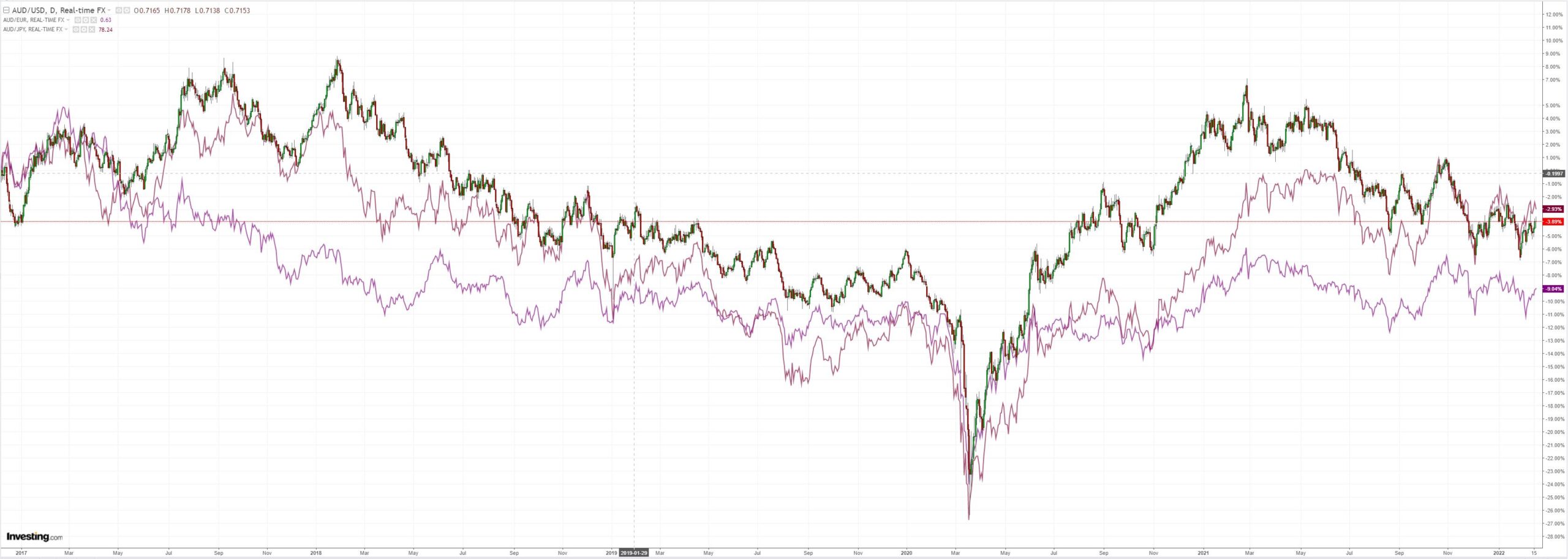

The AUD is being supported by interest rates balderdash. Barclays (LON:BARC) is typical:

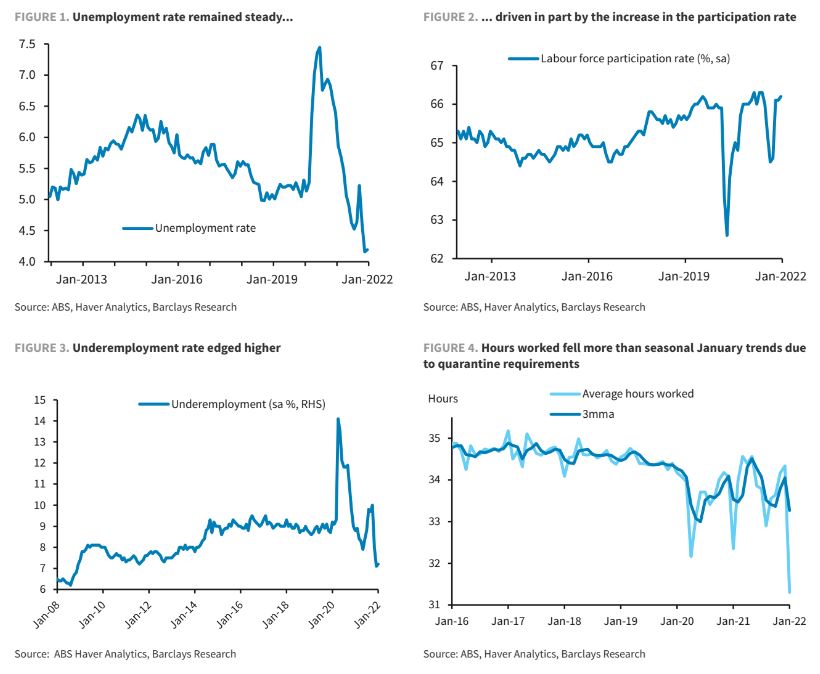

The unemployment rate was steady in January, driven by an increase in the participation rate. The declines in hours worked and full-time employment likely were caused by the spread of the Omicron variant, which exacerbated seasonal weakness in January. We still expect the RBA to hike in August. Australia’s unemployment rate remained at 4.2% (4.19%; Dec: 4.16%) in January, higher than our forecast. We think this was partly driven by a higher participation rate. A weaker report (in terms of hours worked) was expected due to the rapid spread of the Omicron variant through Australia in January, which led to more people having to quarantine.

The January jobs report was also affected by more people taking annual leaves as domestic and international borders reopened. We expect the February labour market report to reverse the drop in hours and full-time employment as quarantine requirements have been lowered.

We think the steady unemployment rate despite the spread of COVID will continue to support the RBA’s view of “faster than expected progress” in reaching its goals. We expect the RBA to start increasing the cash rate from August 2022.

My own view is that employment is being exaggerated by the need to over-hire during OMICRON. That said, it is clear that the labour market is in rude health thanks to collapsed immigration.

The issue is, is Australia suddenly going to diverge from the rest of the world and keep growing fast as it slows down. No.

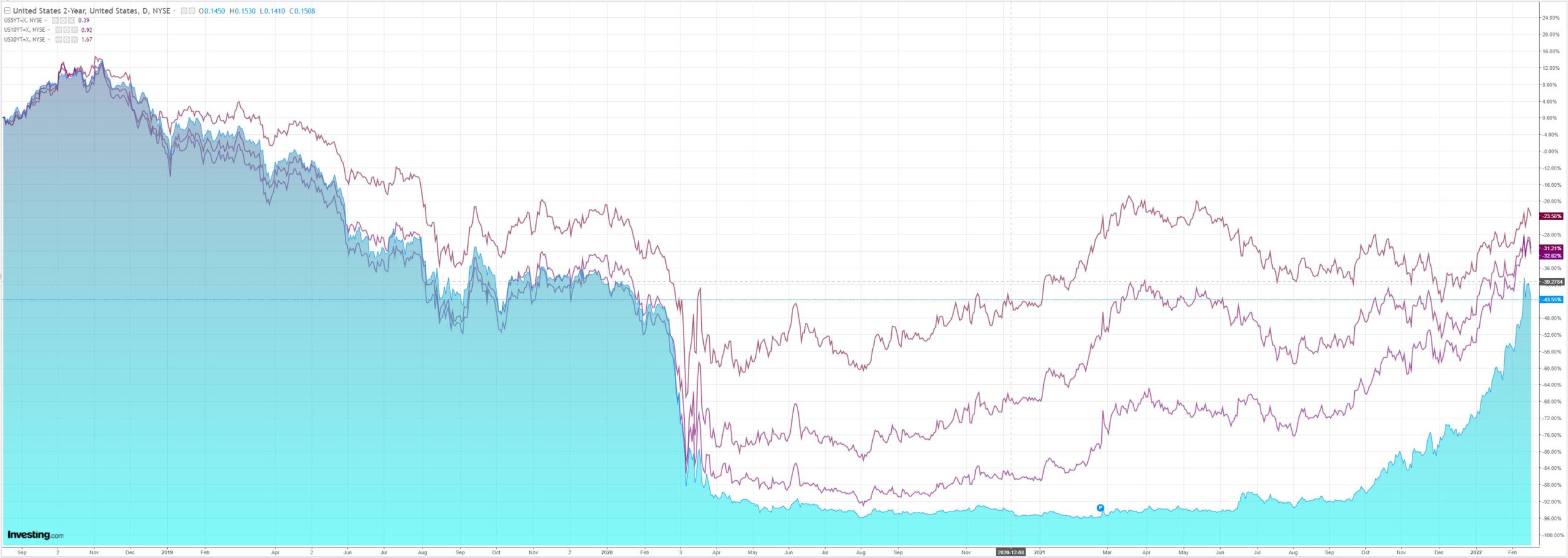

Interest rate markets are now pricing the local cash rate at 2% within 14 months, higher than in the US at that juncture. That’s a joke unless the RBA is happy to halve house prices.

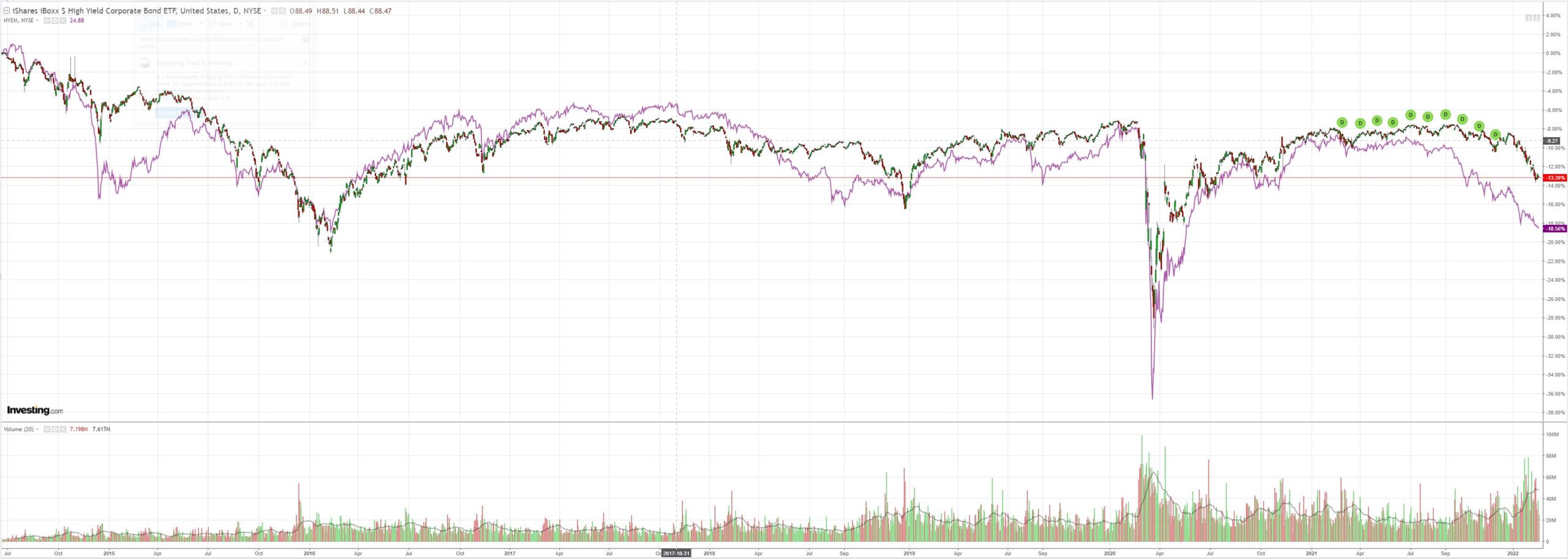

Watch junk spreads. They’re telling us what’s more likely coming. A credit event and lower AUD as the Fed reset does its dirty work.

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed. Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website. Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.