UK production data for April was weak across the board. GDP fell 0.3%m/m (est. +0.1%m/m, prior unchanged at -0.1%m/m), ONS noting that this was the first month since Jan. 2021 that all component sectors contracted. Industrial production fell 0.6%m/m (est. +0.3%m/m), manufacturing -1.0%m/m (est. +0.2%m/m), construction -0.4%m/m (est. -0.5%m/m), and services -0.3%m/m (est. +0.1%m/m).

Event Outlook

Aust: The May NAB business surveywill provide insight into how the Federal Election result and the RBA’s first rate hike was received.

NZ: Supply and staff shortages will be adding further upward pressure to food pricesin May (Westpac f/c: 0.8%).

Eur/UK: The ZEW survey of expectationsshould continue to reflect the weakness in European confidence in June. Meanwhile, the UK’s ILO unemployment rateis expected to push further below pre-pandemic levels in April (market f/c: 3.6%).

US: Ongoing supply issues are expected to keep producer priceselevated in the near-term (market f/c: 0.8%), which in turn will continue to impact small business optimismin the NFIB’s May survey (market f/c: 93.0).

Nomura sums it up:

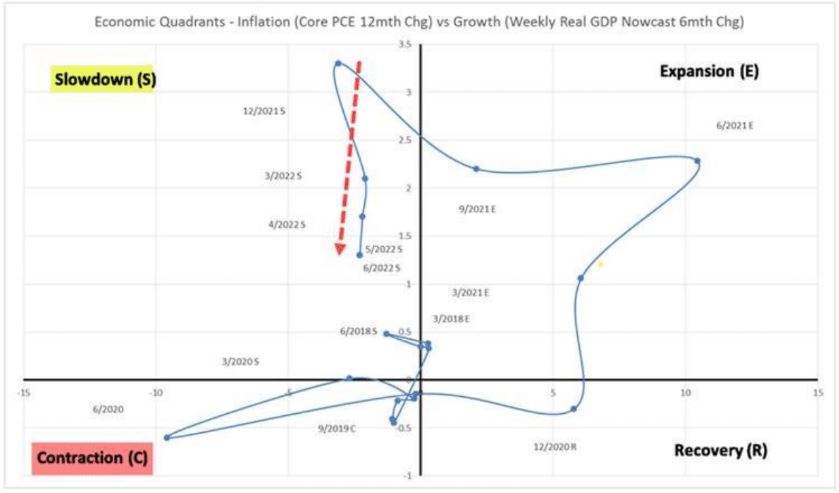

This past Friday’s blistering US CPI upside shocker, alongside the horrific outputs on U Mich -Sentiment and -Inflation Expectations, crystalized the “worst fears confirmed” of a market which simply has nowhere left to hide except for USD and Long Vol, as even Commods are “giving back” today, on repricing of the Central Bank “FCI tightening left tail,” which means “hard landing” Recessionodds again ratcheting higher and pricing a full Fed “cut” btwn Jun23-Dec23.

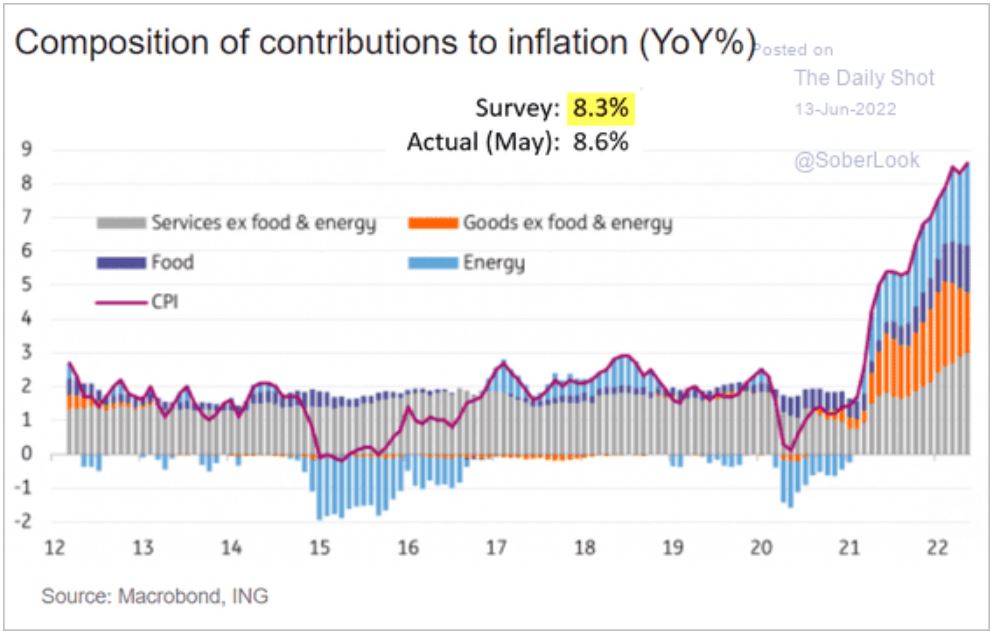

Yep. The Fed has to kill oil and it will take a major recession to do it. It is no more complex than that. Goods are deflating. Services will as housing slows and Labor markets ease. It’s all about energy (which is food) now:

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed. Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website. Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.