The AUD is getting hosed by the European recession, which will worsen before it gets better. TSLombard:

…the ECB is now acknowledging the impact of monetary tightening on credit, and, indeed, the latest ECB Bank Lending Survey (BLS) and bank credit flow data – key for the heavily bank-intermediated EA economy – show further deterioration. Besides a further tightening in banks’ lending standards, EA firms and households’ demand for loans fell at the fastest pace since the Global Financial Crisis, contracting again well below banks’ expectations for Q2. As we pointed out in the past, the breakdown of the factors behind the freeze in loan demand for firms confirms that, while rising interest rates are a key drag on new borrowing in line with monetary policy tightening, businesses appear to be running out of investment opportunities that need financing (“fixed investment”) – consistent with the EA stagnating since 2022Q3 and, historically, an ominous sign for the health of the underlying economy. What is more, demand for inventory and working capital financing has now also started to contract. Bank credit flow data echo the message from the BLS. Household credit on a 3-month rolling average basis shrank for the first time since the peak of the EA sovereign crisis, while nonfinancial corporates’ credit flows stalled again, confirming that the little gains made in the past few months were a blip.

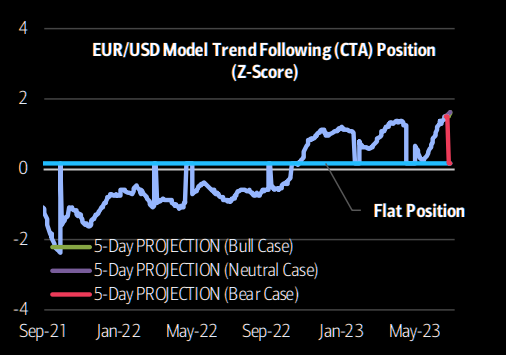

Stocks are cheap but earnings are about to clubbed like a baby seal. I can’t see why anybody wants to be long Europe at this juncture. Yet everybody is:

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed. Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website. Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.