It was a double blow for EUR and, therefore, AUD Friday night.

Europe is in recession, and it’s going to get worse. Flash PMIs are swooning:

France: The French composite flash PMI decreased by 3.8pt to 47.3, below consensus expectations. The composite decline was broad-based across sectors but skewed heavily towards services, which fell into contractionary territory after four consecutive months of above-50 postings.

Germany: The German composite flash PMI decreased by 3.1pt to 50.8, also below consensus expectations. The decline in the composite index was broad-based across sectors, although unlike the manufacturing output index, the services index remained in expansionary territory.

Periphery: The periphery composite PMI decreased by 1.1pt to 51.7. As in Germany, the composite decline was broad-based across sectors, although the services index remains in expansionary territory, while manufacturing output contracted further.

As well, China’s new premier, Li Quang, showed he is in no hurry for more stimulus to aid Europe’s export economy:

Premier Li Qiang told a summit in Paris that the Chinese economy has shown “upward momentum” this year and fundamentals for long-term sound economic development are unchanged.

China is not only not stimulating, but it is also rapidly evolving into a major threat to European car-makers as EV exports explode. This is a terrific development in geopolitical terms, given it will drive a wedge between the two and it’s not good for the European economy.

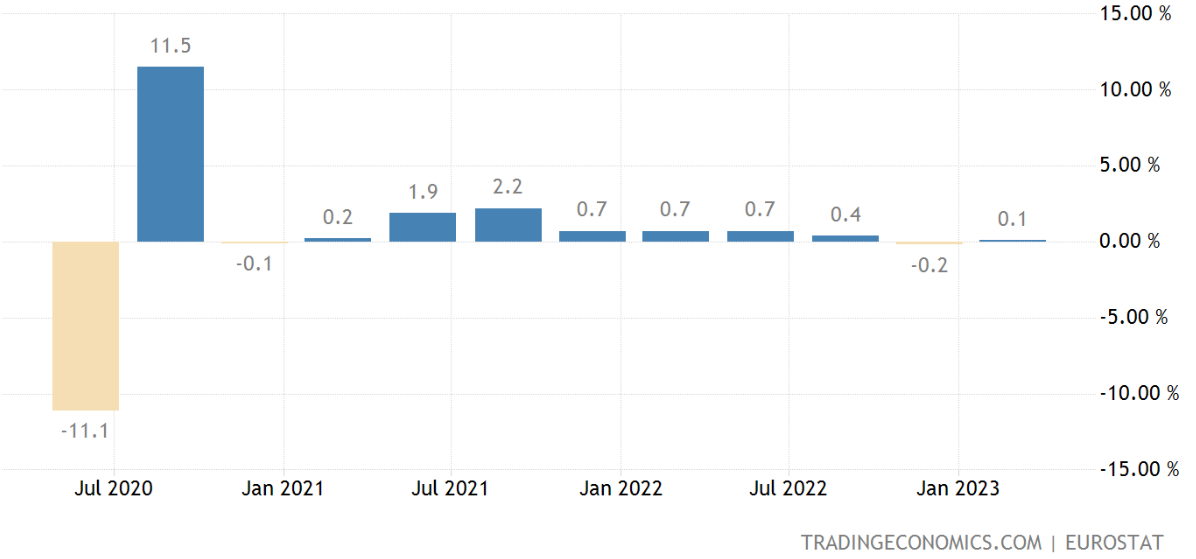

With the ECB still banging on about two more rate hikes, Europe looks set to lead the developed world into contraction. Recalling that it has virtually been there for six months already:

A weak Europe and China versus an AI-juiced US as the last growth man standing is very AUD bearish.

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed. Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website. Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.