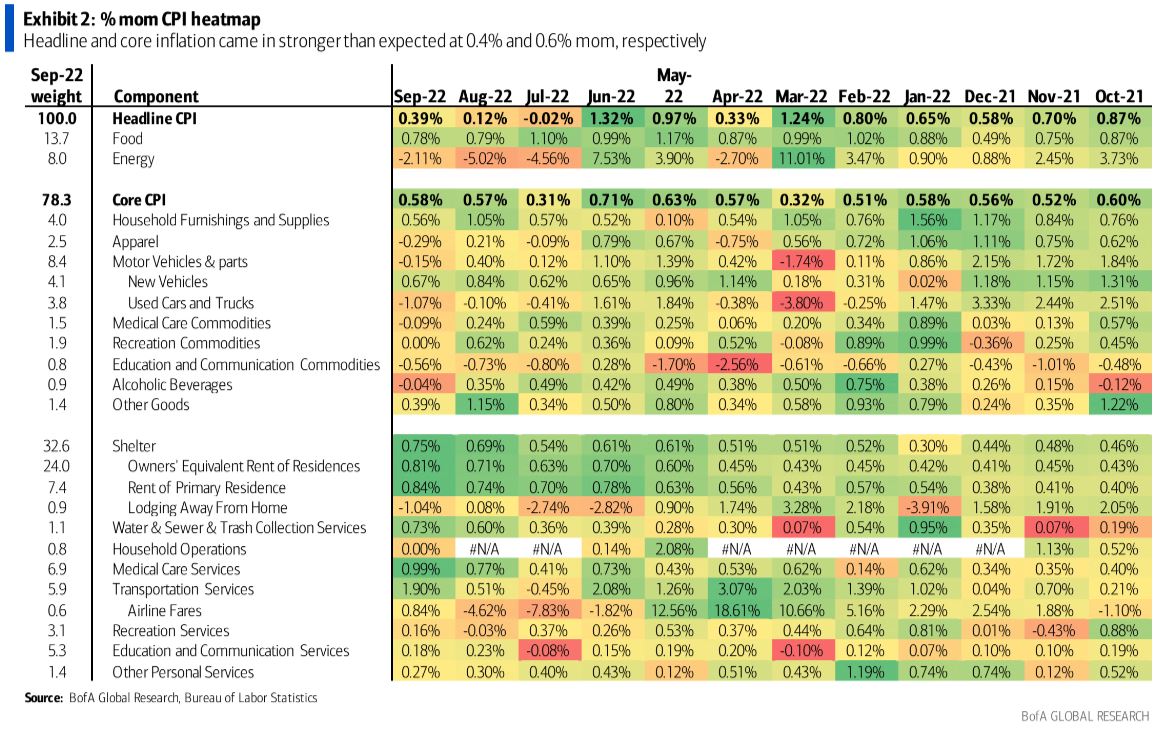

Headline CPI prices rose 0.4% in September, compared toour0.2% forecast. Energy prices fell2.1% m/m and food prices rose 0.8%. Both numbers were slightly stronger than we were expecting(BofA:-3.5% and 0.7%, respectively).Y/y headline CPI inflation dropped to 8.2% from 8.3%.

The key upside surprise was in core inflation. Core CPI rose 0.6% mom vs. our expectation of a 0.4%increase. The y/yrate surged to 6.6%, which marks a 40-year high. The strength in core inflation was driven by core services, which rose by 0.8% m/m after a 0.6% m/m increase in August. Shelter inflation rose to 0.8% m/m (0.75%) from 0.7%m/m previously. Both rent and OER moved up from 0.7% m/m to 0.8% m/m, but lodging away from home fell by 1.0% m/m. Elsewhere transportation services were a big contributor. Airline fares rose by 0.8% m/m, after three consecutive monthly declines, and motor vehicle insurance increased by 1.6% m/m, up from 1.3% m/m in the prior two months. Car and truck rentals were also up 2.5% m/m. Medical care services rose by 1.0% m/m, though we may soon see some softer readings there.

Meanwhile, core goods inflation was softer than expected at 0.0% m/m. On average over the previous three months, core goods inflation has posted a 0.2% m/m increase, compared to the 0.6% m/m average in 2Q. Used car prices fell more than we had projected (-1.0% vs.-0.1% expected). New vehicles, on the other hand, were stronger than we expected (0.7% m/m vs. 0.5% m/m). Used car prices could continue to slide given the trajectory of wholesale prices. Apparel prices also fell for the second consecutive month, down 0.3% m/m. Appliances fell for a fourth consecutive month (-0.7%m/m). We would expect further declines over the coming months in these categories as businesses work off excess inventories.

The substantial slowdown in core goods inflation is consistent with the notion that supply chain pressures are easing. We continue to expect a period goods disinflation, followed by deflation. However, core services inflation has now inched ahead of core goods inflation on a y/ybasis(6.7% vs. 6.6%). Shelter inflation is a lagging indicator, and alternative rent data suggest there is moderation in the pipeline. Nonetheless, we think sticky-high services inflation is a reflection of the resilience of the labor market, since services are labor-intensive and produced domestically.

So from the Fed’s perspective, the inflation mix in the September CPI report strengthens the case to stay hawkish. In our view, the Fed needs to slow the labor market down significantly to bring inflation back to target. And so far, labor market gains remain solid despite the unprecedented pace of monetary tightening. This also means there is no conflict at the moment between the Fed’s two mandates: both are sending a clear signal to raise rates significantly further.

And they will until everything breaks. But, for now, it’s another tactical bounce lasting however long tactical positioning takes to correct.

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed. Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website. Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.