So, how far does the AUD breakout have to run? It’s a question of commodities versus growth. Barclays (LON:BARC):

Markets have moved a lot faster than we expected. In our inaugural FX Views, we argued that the dollar was in the process of peaking and that commodity currencies are our preferred long exposures – and we have backed this view up with a number of trade recommendations too. Yet, market moves have been a lot faster and stronger than we initially expected (and than our forecasts envisaged).

And the forward picture for risk sentiment may not be as clear. The rally in commodity currencies and softening of the dollar has taken place in a setup where equity risk premia have compressed dramatically. Since early March, the VIX has declined by 15 points and this sentiment has partly supported the FX moves. At the same time, several risks both for equities and commodities lurk.

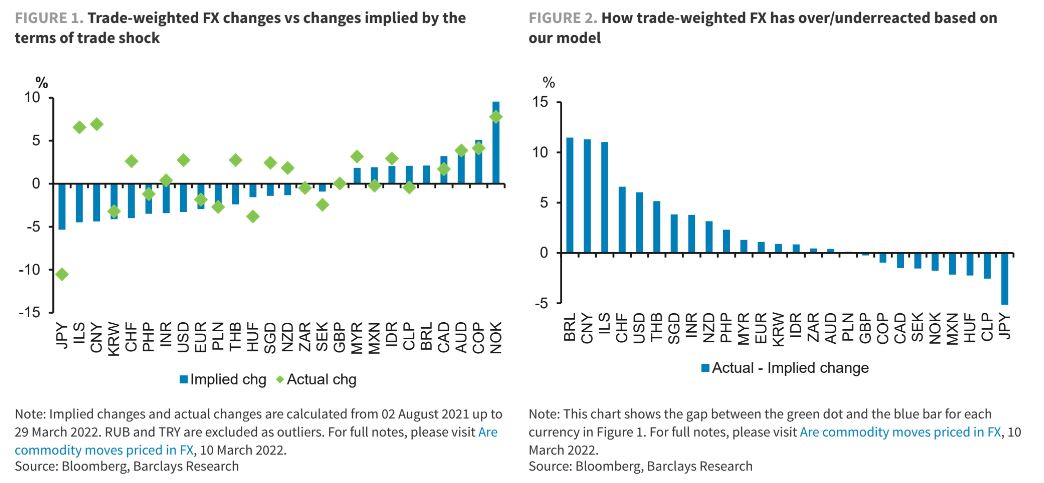

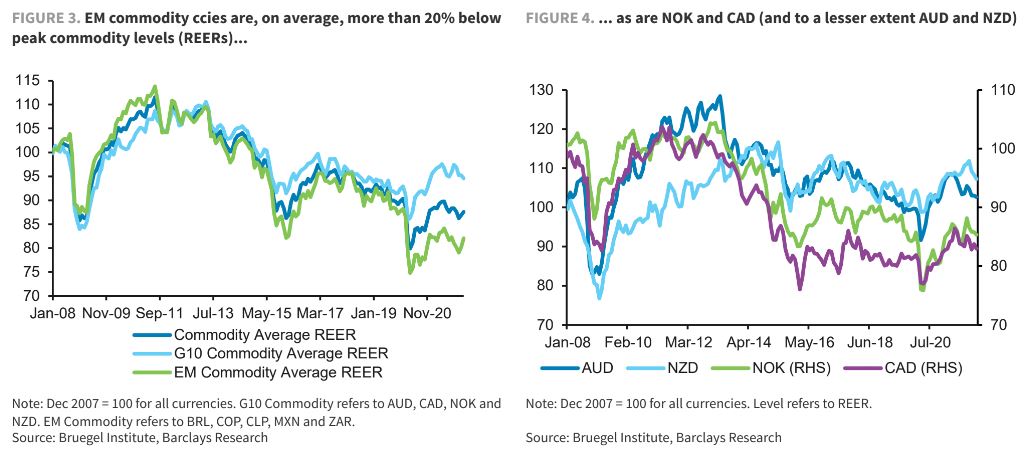

Time to throw in the towel? The big picture is that commodity currencies are coming off of very cheap starting points. Real effective exchange rates across most commodity exporters are hovering more than 20% below levels they were valued at during previous commodity booms.

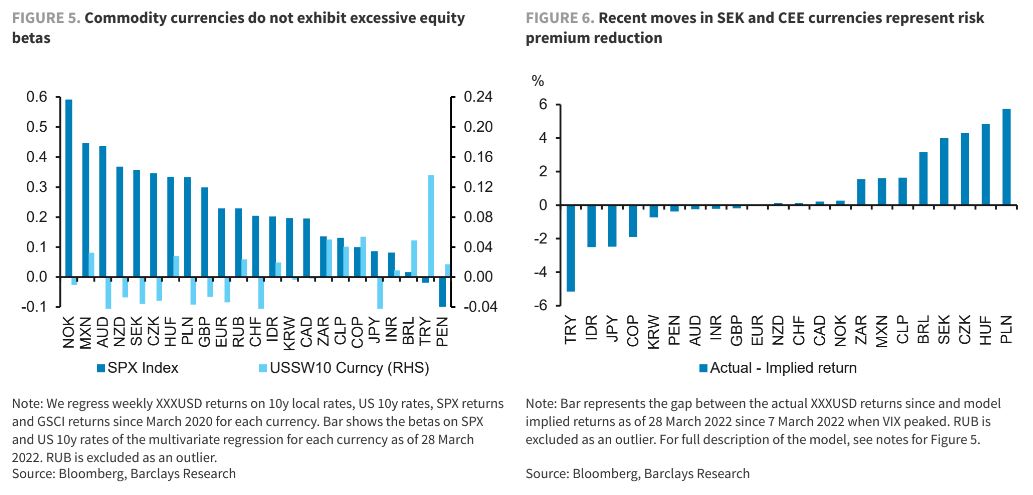

Managing tactical risks. Rotating funders can help hedge commodity currency exposures, in the event of an adverse risk move. To identify which currency might be most exposed to an equity sell-off, we run a factor regression where dollar crosses are regressed against changes in local 10y rates, US 10y rates, SPX returns and GSCI returns. We find that the average beta of commodity currencies to equities is not materially different to that of the EUR. SEK and CEE currencies are direct hedges if there is a flare up in the Russia-Ukraine war. Within the commodity space, the beta to risk can be further reduced by tactically bringing down the exposure to MXN and NOK, in particular. AUD would also underperform substantially in a risk-off scenario where yields stay high or rise further.

My own view is that global recession is coming much faster than most think, which will add double the downside to AUD as commodities crash and DXY rockets.

That said, until that panic emerges in full, AUD is clearly biased upwards on Ukraine war commodity price impacts.

These extreme opposing forces risk above all greater volatility and the AUD outlook takes on the dimensions of a boom and bust.

My base case is that this will fully play out in 2022.

Australian dollar boom and bust in battle of central banks

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed. Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website. Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.