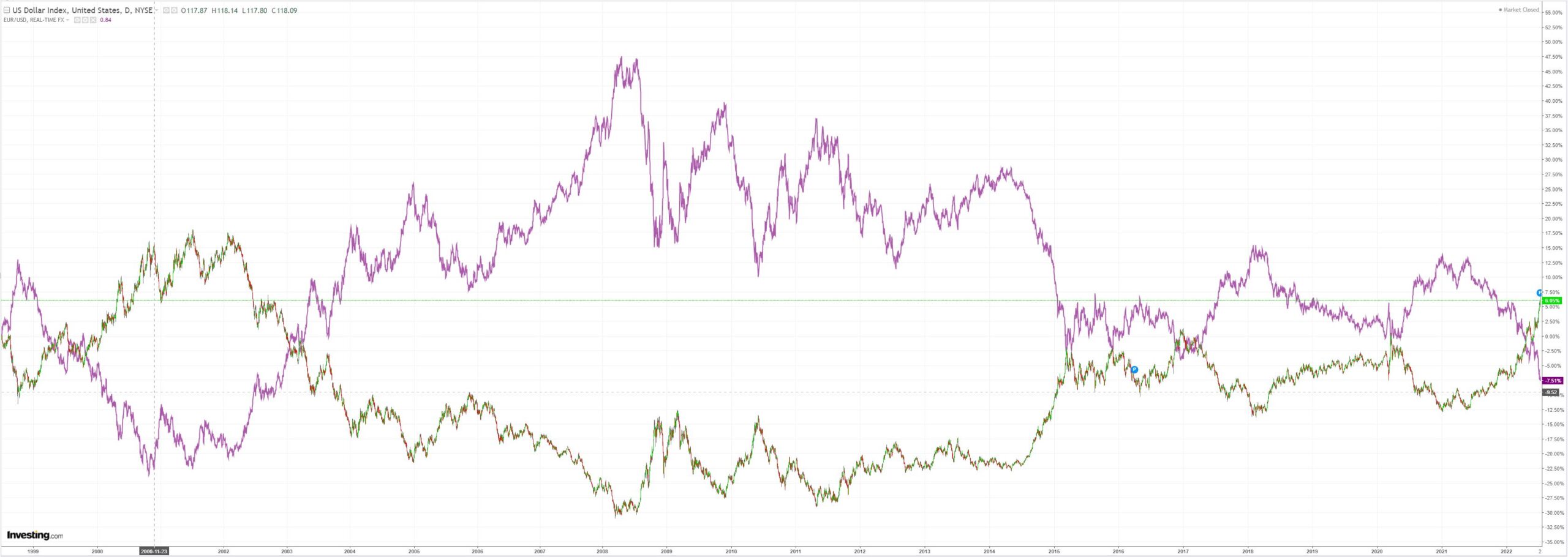

DXY is in a historic blowoff as EUR heads for god knows where

AUD hit new lows in the 66s but managed to rebound as the Fed hosed 100bps hikes. As if that matters!

Oil is going to crash any day:

The great metals “super cycle” is an utter bust:

Adieu miners (LON:GLEN):

EM stocks (NYSE:EEM) cracked as Chinese jingle mail smashed that bourse:

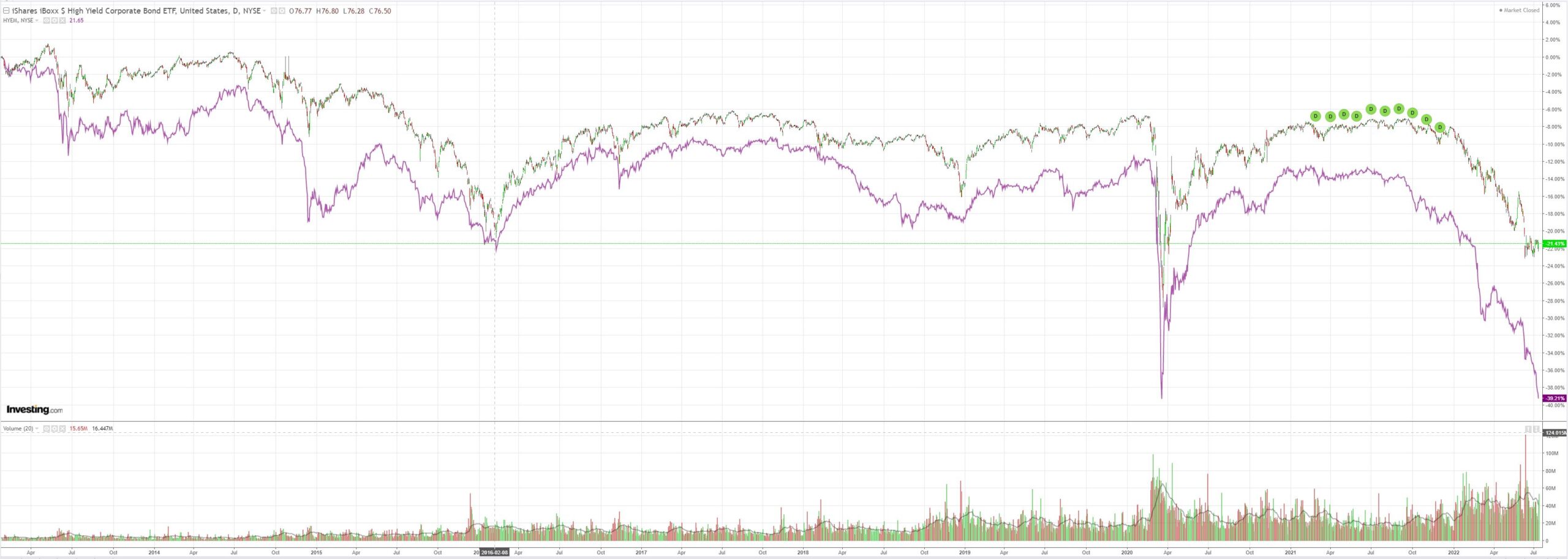

EM junk (NYSE:HYG) is something to behold:

Silly Treasuries were sold even as inflation goes up in smoke:

Stocks held on. Good luck with that!

Westpac has the wrap:

Event Wrap

US PPI rose 1.1%m/m and 11.3%y/y in June (est. +0.8% and 10.7%). The core measure rose 0.3%m/m and 6.4%y/y (est. 0.5% and 6.6%). Weekly initial jobless claims rose 244k (est. 235k, prior 235k), with continuing claims at 1331k (est. 1380k, prior 1372k).

FOMC member Waller played down risk of a 100bp July hike, at least until he sees more data on retail sales and housing. The CPI data was a “major disappointment,” but not a big surprise. He had already penciled in a 75bp hike and the data merely assured it. He suggested market pricing may have overreached. He does not expect a recession given the strength in the labour market, but the economy could slow. He will support ongoing hikes until he sees “significant moderation” in core PCE prices toward the 2% goal. Bullard favoured sticking with a 75bp hike for July, rather than a larger move: ?So far, we?ve framed this mostly as 50 versus 75 at this meeting. I think 75 has a lot of virtue to it? (because it brings the rate to roughly neutral). ?As of today, I would advocate 75 basis points again at the next meeting.?

Event Outlook

NZ: The resilience of the BusinessNZ manufacturing PMI will be tested in June as downside pressures mount.

China: GDP growth will be hit hard by COVID-zero lockdowns over Q2 (market f/c: -2.0%qtr; +1.2%yr). The weakness in consumption will continue to weigh on retail sales over the near-term (market f/c: -1.2%yr ytd). However, building momentum in fixed asset investment and ongoing strength in industrial production has provided some underlying support to the economy (market f/c: 6.0%yr ytd and 3.5%yr ytd respectively).

Eur: The trade deficit is set to remain wide given the strength of energy prices (market f/c: -?35bn).

US: Elevated gas prices are set to buoy retail sales in June although broad-based inflation and higher rates are also affecting spending capacity (market f/c: 0.9%). With import prices expected to remain elevated given ongoing supply issues (market f/c: 0.7%), industrial production will likely remain weak in June (market f/c: 0.1%); for similar reasons, weakness in the Fed Empire state index is anticipated in July (market f/c: -2.0). Business inventories are expected to continue building at a robust pace (market f/c: 1.4%). However, another historically weak print is anticipated for the July University of Michigan sentiment survey given ongoing inflation pressures and aggressive financial tightening (market f/c: 50.0).

This is all so yesterday. Something is going to break soon and it looks like it may be China as its property crash metastasises into a banking crisis.

Commodities and AUD are in the direct line of fire.