The US observed a partial holiday for Veterans’ Day.

UK 3Q GDP disappointed expectations, at +1.3%q/q and +6.4%y/y (est. +1.5%q/q, +6.6%y/y). Although government spending was firm at +0.9%q/q (est. +0.7%), private consumption undershot at +2.0%q/q (est. +3.1%), fixed capital formation was only +0.8%q/q (est. +2.4%), and business investment was weak at +0.4%q/q (est. +3.5%). Industrial production in September fell 0.4%m/m (est. +0.2%m/m), while services activity rose +0.7%m/m (est. +0.5%m/m) with downward revisions to prior months. Construction was strong at +1.3%m/m (est. +0.2%m/m.).

Event Outlook

NZ: The October manufacturing PMI will highlight NZ’s continued recovery as Auckland’s restrictions eased.

Europe:Industrial production should stabilise in September after August’s drop (market f/c: 0.2%).

US: Hire and quit rates and job openings in September’s JOLTS report will show the strength of the job market as well as the confidence of participants. November’s University of Michigan sentiment survey is likely to again show confidence lagging activity, in contrast to most developed markets (market f/c: 72.5).

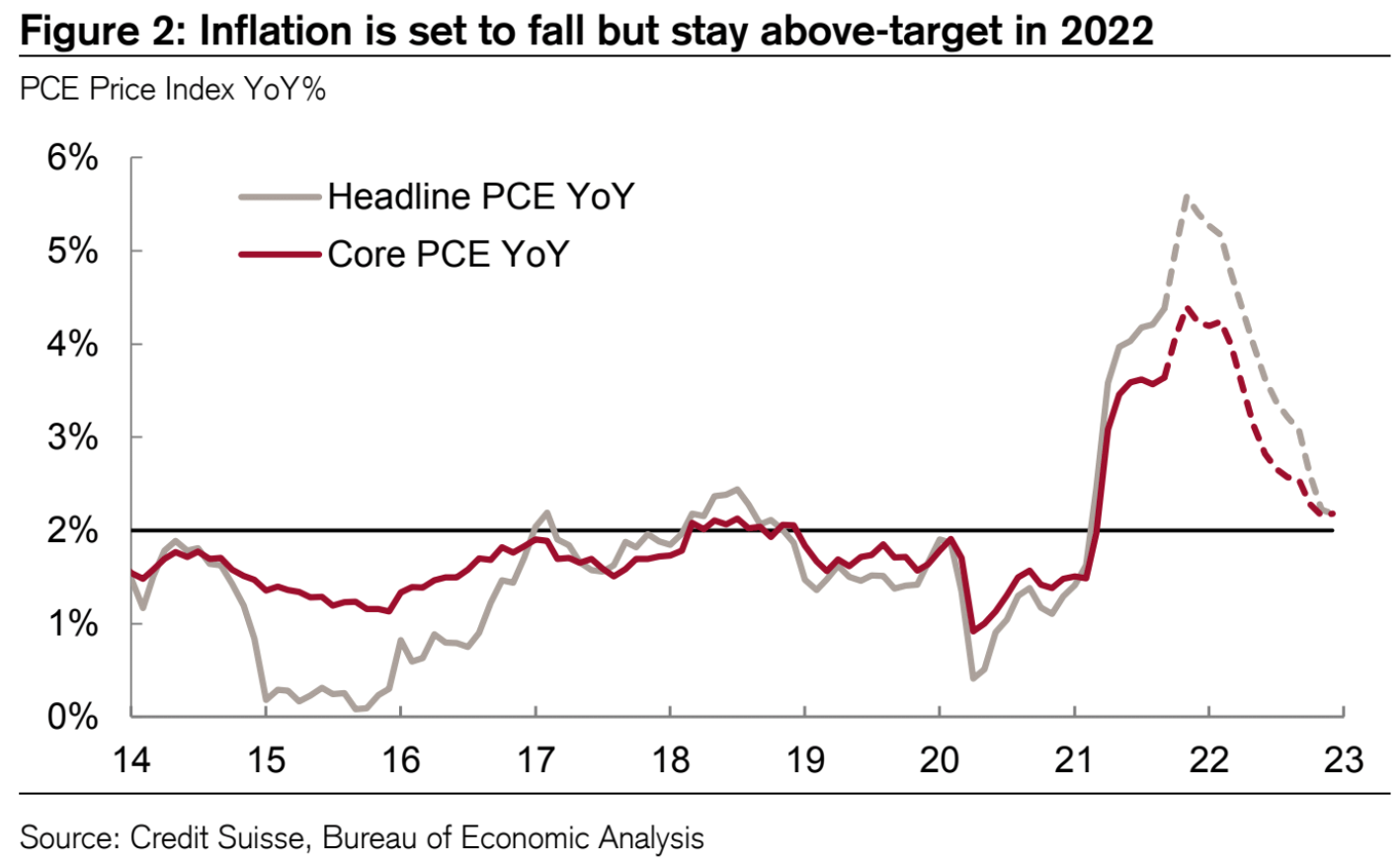

We now expect the Fed tightening cycle to begin with a 25bp rate increase in Q4 2022. Beyond that, we expect a steep path of hikes, and now see 125bps cumulatively by the end of 2023, and an eventual normalization to 2.75-3.0%. Our inflation forecasts have risen moderately, our expectations for strong jobs growth have been supported by new data, and financial markets have priced in more 2022 tightening than we expect, pressuring the Fed at a time when US politicians are increasingly being forced to address voters’ inflation concerns. These are the reasons for our view shift. We had been reluctant to embrace 2022 hikes because we foresee sharply falling US inflation, slowing global industrial production growth, and weak US real retail sales in the second half of 2022. Those things are typically sufficient to stay the tightening hand of a central bank. But inflation is likely to remain clearly above 2% in headline and core terms in late 2022. In our view, the market is pricing hikes to occur too soon, but is also pricing too few hikes once the tightening cycle begins. Underlying inflation pressures, including a structurally tight labor market, strong housing inflation, and a more tolerant attitude toward inflation by the Fed leadership, is likely to allow above-2% core inflation to persist in the coming years. US core inflation will prove stubbornly elevated even through short term slowdowns, in our view, leading to more hikes than most expect. Recent price data have shown a broadening of inflation pressures.

As global growth slows over the next few quarters and inflation calms down, I still also expect a large commodities complex bust across 2022 so that can stay the Fed’s hand for a while.

But, readers will know that I have long forecast US exceptionalism for this cycle with stronger growth, inflation, and yields than elsewhere, especially China which will lag as it addresses structural problems. I have therefore also expected a DXY bull market and it appears to have arrived in earnest.

With a tearaway greenback and bulk commodities bust lining up in 2022, AUD is in trouble.

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed. Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website. Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.