In the latest quarterly update from Tata Motors (NS:TAMO), the numbers are consistent with expectations. Their revenue and EBITDA saw a slight dip of -1% and -2% respectively compared to Bloomberg's consensus. Specifically, their EBITDA in the Jaguar Land Rover (JLR), Commercial Vehicles (CV), and Passenger Vehicles (PV) segments fell by -2%, -1%, and -6% respectively, compared to estimates.

Despite this, JLR's management has successfully turned the business around, achieving positive free cash flow over the past year and a half. Looking ahead to FY25, they anticipate maintaining a flat EBIT margin, with an expected increase in Variable Marketing Expenditure to drive demand now that post-COVID supply shortages have eased.

Offer: Unlock smart investing with InvestingPro! An advanced stock analysis tool that uses diverse financial models to reveal the true value of stocks, eliminating extremes. Limited-time offer: Click here and get 69% off, just INR 216/month!

Forecasts suggest a low single-digit volume growth for JLR in FY25 as the order backlog stabilizes. While April showed promise, Tata Motors foresees a relatively softer first half of FY25 for domestic cars and CVs due to factors like the ongoing heatwave and delayed commercial vehicle demand caused by elections.

However, management remains optimistic about future prospects. They anticipate a shift towards higher tonnage vehicles and improved pricing strategies in the CV business, although substantial growth may only materialize post-election results in June. Despite increasing investment in JLR, Tata Motors is expected to achieve a net positive cash position at a consolidated level by FY25.

Goldman Sachs (NYSE:GS), who previously rated Tata Motors as a Buy, has now shifted their stance to Neutral. Since April 2023, Tata Motors' stock has surged by +140%, outperforming the NIFTY 50 by a significant margin. Factors such as the successful turnaround of JLR, improved cash flow, and strategic expansions in the PV sector seem to be adequately priced into the stock.

In terms of valuation, Tata Motors currently trades at an FY25E P/E of 14.7x, notably higher than its historical median of 10.4x. However, Goldman Sachs has revised down their FY25-FY26 EPS estimates by up to -4% due to concerns over JLR's margin trajectory and a slower-than-expected start to FY25 in the CV business.

Potential risks moving forward include uncertainty surrounding JLR's transition to electric vehicles compared to competitors like Mercedes, BMW, and Audi, as well as the impact of commodity cost inflation and increased competition in the Indian electric car market from companies like Mahindra and Maruti (NS:MRTI).

Image Source: InvestingPro+

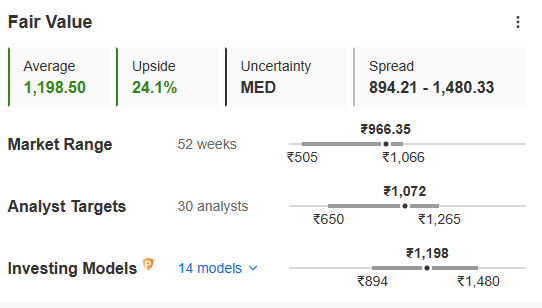

Goldman Sachs now sets Tata Motors' 12-month target price at INR 1,040, down from INR 1,080, reflecting their revised earnings estimates. However, investors can also wait for a higher target of INR 1,198 which is the actual fair value of the stock, depicting an upside of 24.1%. This is the average intrinsic value of the stock after taking 14 financial models into consideration.

But what’s more important is Goldman Sachs and InvestingPro’s fair value is showing some upside potential in the counter. In fact, an average of 30 analysts covering this counter are also bullish, giving an average target of INR 1,072 per share, as seen in the image above.

Discover the real value of stocks with InvestingPro! An industry-grade tool that employs sophisticated financial models to provide accurate insights. Act now by clicking here and enjoy a special discount: 69% off, only INR 216/month!

Also Read: Here’s How to Hunt for “Undervalued Stocks” in This Correction

X (formerly, Twitter) - Aayush Khanna